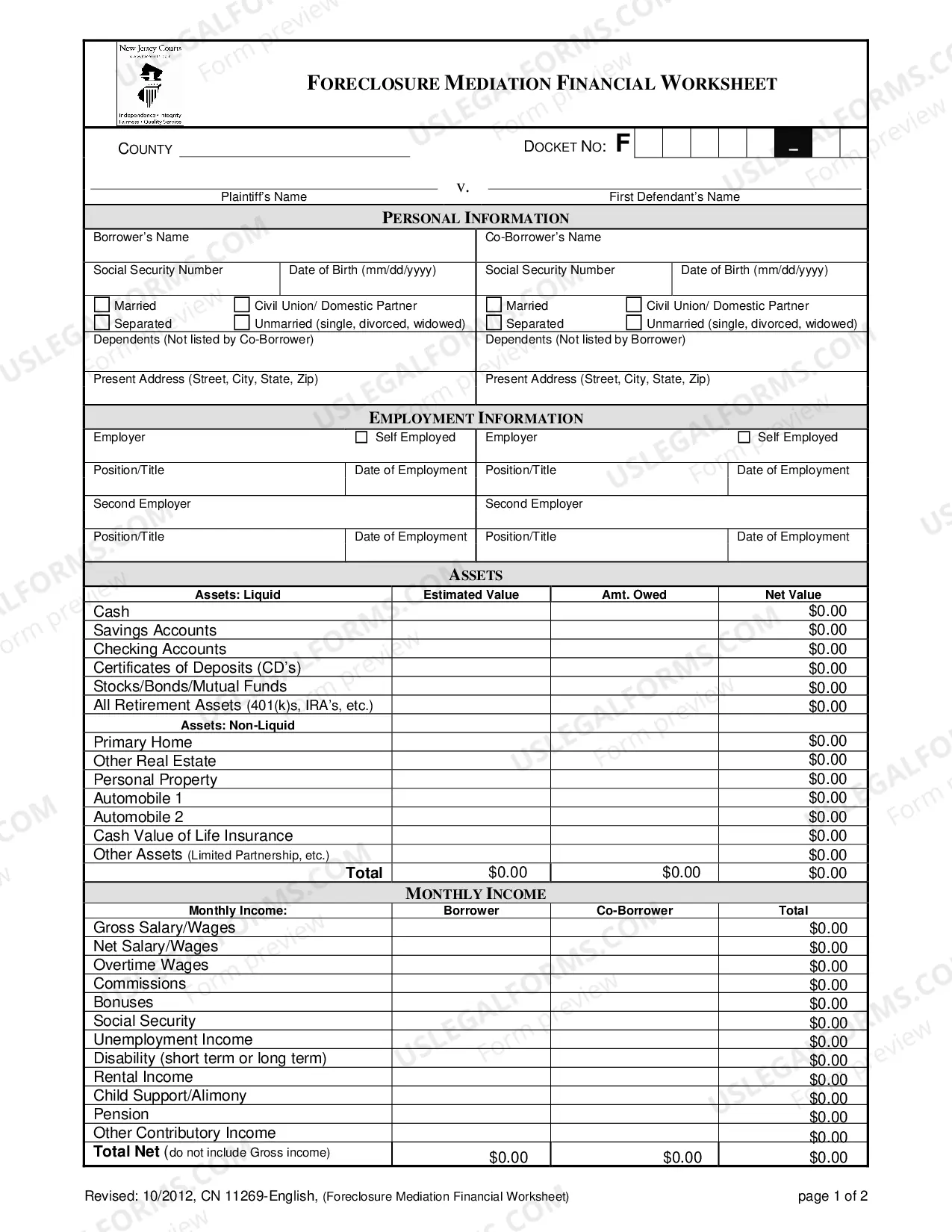

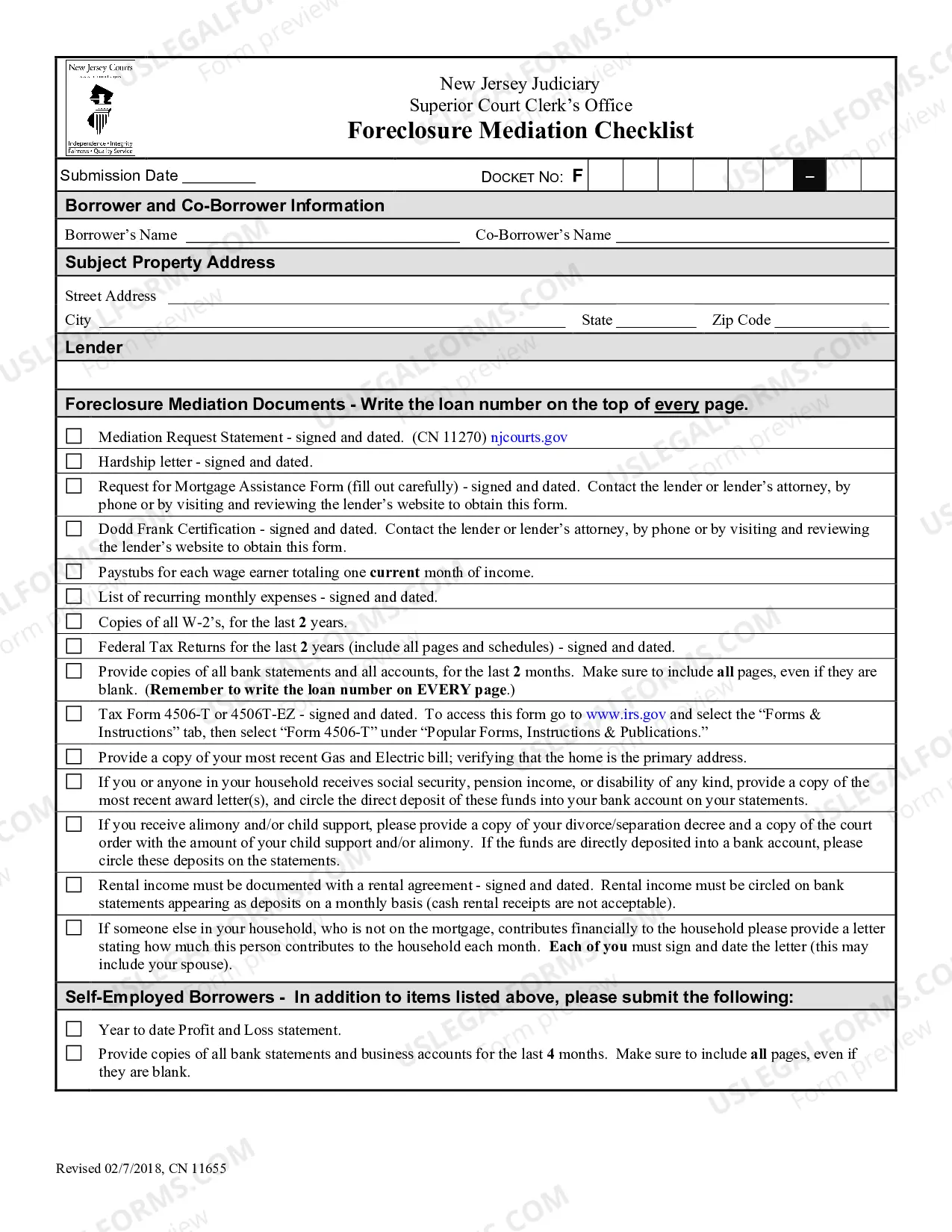

New Jersey Foreclosure Amount Due Schedule is a document that outlines the amount of money owed to a lender for a property in foreclosure in the state of New Jersey. It typically includes the total amount due, the date the payment is due, any late charges or fees associated with the payment, the amount of principal and interest due, and the breakdown of any additional fees. There are two types of New Jersey Foreclosure Amount Due Schedule: pre-foreclosure and post-foreclosure. Pre-foreclosure schedules list the amount due to the lender prior to the foreclosure sale, while post-foreclosure schedules list the amounts due to the lender after the foreclosure sale.

New Jersey Foreclosure Amount Due Schedule

Instant download

This website is not affiliated with any governmental entity

Public form

Description

Foreclosure Amount Due Schedule

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Key Concepts & Definitions

Foreclosure Amount Due Schedule:A detailed timeline that outlines the amounts due at various stages of foreclosure proceedings. This includes the payments needed to avoid foreclosure and the deadlines by which these amounts must be settled.

Mortgage Loan:A loan secured by real property through the use of a mortgage note which evidences the existence of the loan and the encumbrance of that realty through the granting of a mortgage which secures the loan.

Foreclosure Process:The legal procedure by which a lender attempts to recover the balance of a loan from a borrower who has stopped making payments by forcing the sale of the asset used as the collateral for the loan.

Step-by-Step Guide to Understanding the Foreclosure Amount Due Schedule

- Review Your Mortgage Agreement:Identify the terms regarding foreclosure and any specific conditions or timelines stipulated for repayment.

- Communicate with Your Lender:Reach out to your lender to obtain a detailed foreclosure amount due schedule. This often includes exact dates and amounts due to stave off foreclosure.

- Assess Insurance Coverage:Confirm with your homeowners insurance to ensure coverage aligns with requirements, potentially affecting foreclosure risks and costs.

- Consult a Financial Advisor:Consider professional help to plan finances including refinancing options, restructuring of mortgage loans, or personal loans for managing the credit balance effectively.

- Stay Informed About State Laws:Understanding local regulations and Fannie Mae guidelines that may influence the foreclosure process in your region.

Risk Analysis of Neglecting the Foreclosure Amount Due Schedule

- Elevated Legal Costs:Ignoring the schedule can lead to increased fees and legal costs as the foreclosure process progresses.

- Credit Score Impact:Late payments and foreclosure can significantly lower your credit score, influencing your ability to secure future lines of credit or any financial aid.

- Loss of Property:Ultimately, failing to keep up with the scheduled payments might result in losing your home and any equity built over time.

- Insurance Complications:A lapse in insurance payments during foreclosure can lead to breaches in insurance requirements, adding further to costs.

Common Mistakes & How to Avoid Them

Lack of Communication with Lenders:Borrowers often avoid contacting their lenders out of fear or confusion. It's crucial to communicate early to discuss potential payment arrangements or modifications.

Ignoring Legal Notices:Disregarding any legal communications can hasten the foreclosure process. Respond promptly to any notices received.

Underestimating Expenses:It's essential to consider all related property expenses including insurance, taxes, and maintenance when analyzing one's financial capacity to meet scheduled payments.

How to fill out New Jersey Foreclosure Amount Due Schedule?

US Legal Forms is the most straightforward and affordable way to locate suitable formal templates. It’s the most extensive online library of business and personal legal documentation drafted and checked by attorneys. Here, you can find printable and fillable templates that comply with national and local regulations - just like your New Jersey Foreclosure Amount Due Schedule.

Getting your template requires only a few simple steps. Users that already have an account with a valid subscription only need to log in to the website and download the form on their device. Afterwards, they can find it in their profile in the My Forms tab.

And here’s how you can obtain a properly drafted New Jersey Foreclosure Amount Due Schedule if you are using US Legal Forms for the first time:

- Read the form description or preview the document to make certain you’ve found the one meeting your requirements, or find another one using the search tab above.

- Click Buy now when you’re sure of its compatibility with all the requirements, and select the subscription plan you like most.

- Create an account with our service, log in, and purchase your subscription using PayPal or you credit card.

- Select the preferred file format for your New Jersey Foreclosure Amount Due Schedule and save it on your device with the appropriate button.

Once you save a template, you can reaccess it anytime - simply find it in your profile, re-download it for printing and manual completion or import it to an online editor to fill it out and sign more effectively.

Take full advantage of US Legal Forms, your reliable assistant in obtaining the corresponding formal documentation. Give it a try!

Form popularity

FAQ

New Jersey is a judicial foreclosure state which means that if you default on your mortgage, the lender must go to court in order to repossess your home. (Some states use nonjudicial foreclosures, which do not go through court.)

In a strict foreclosure, the foreclosing party (the "lender") goes to court to ask for an order declaring you in default on the mortgage and permitting it to foreclose. If the court agrees that you're in default, it will approve the foreclosure and give the title to your home directly to the lender.

After the sale of the property, the debtor has 10 days to redeem the property. This means they can buy the property back or sell it. If the debtor fails to redeem with 10 days, the proceeds of the sale pay off what is owed on the mortgage.

The Fair Foreclosure Act (FFA), N.J.S.A §§ 2A:50-53 to 2A:50-73, is a state law that protects residential mortgage debtors and establishes a uniform statutory framework under which courts can more clearly identify the rights and remedies of the parties involved in foreclosure proceedings throughout New Jersey.

State law requires that all residential mortgage lenders give residential mortgage debtors at least 30 days prior notice before commencing any foreclosure or other legal action to take possession of property (the ?Notice of Intention to Foreclose?).

The Fastest Possible Foreclosure Timeline is About 12 Months If you fail to Answer they must move for Default and have the case returned to the Office of Foreclosure. Then, they must wait 14 days to Move for Entry of Final Judgment. It takes at least 30 days for Final Judgment to be entered.