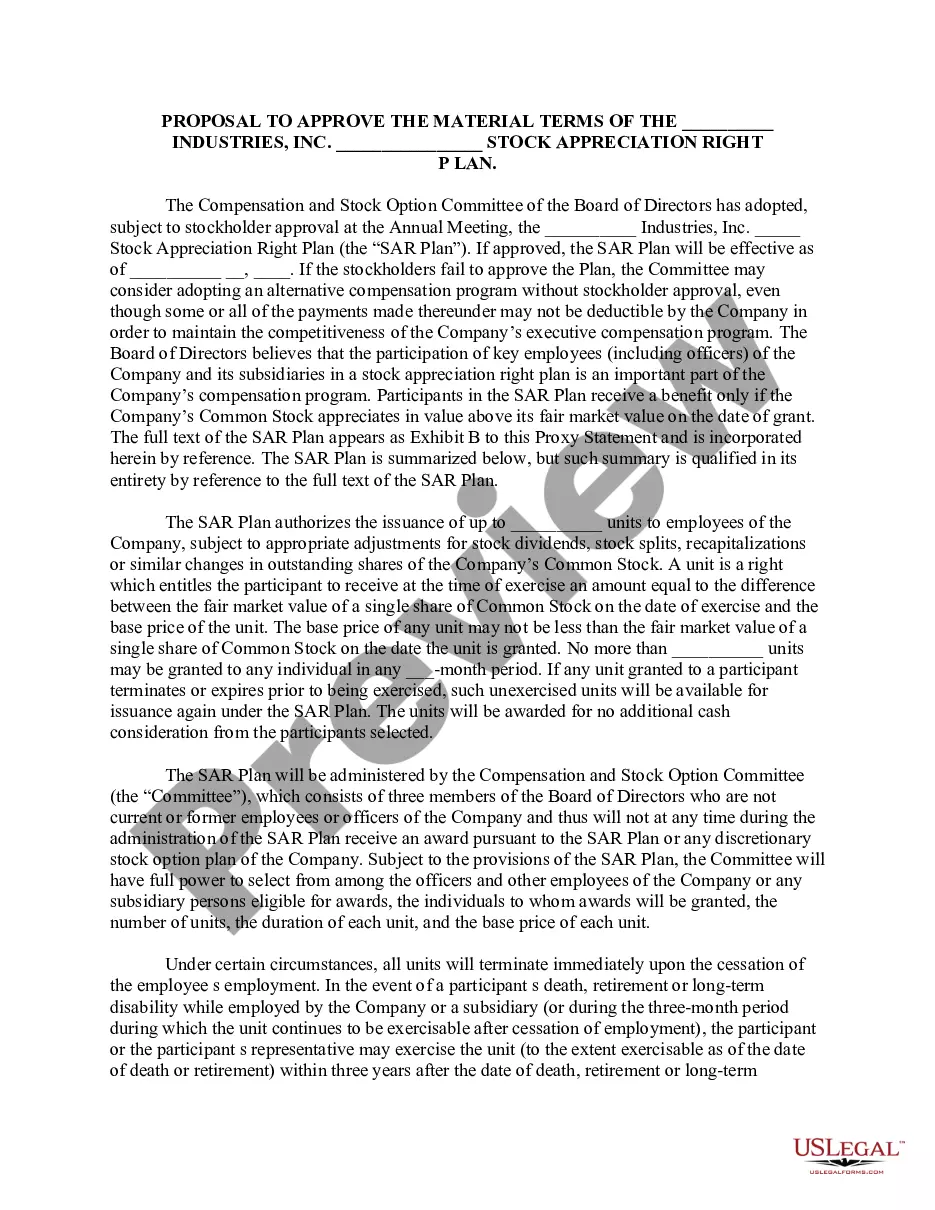

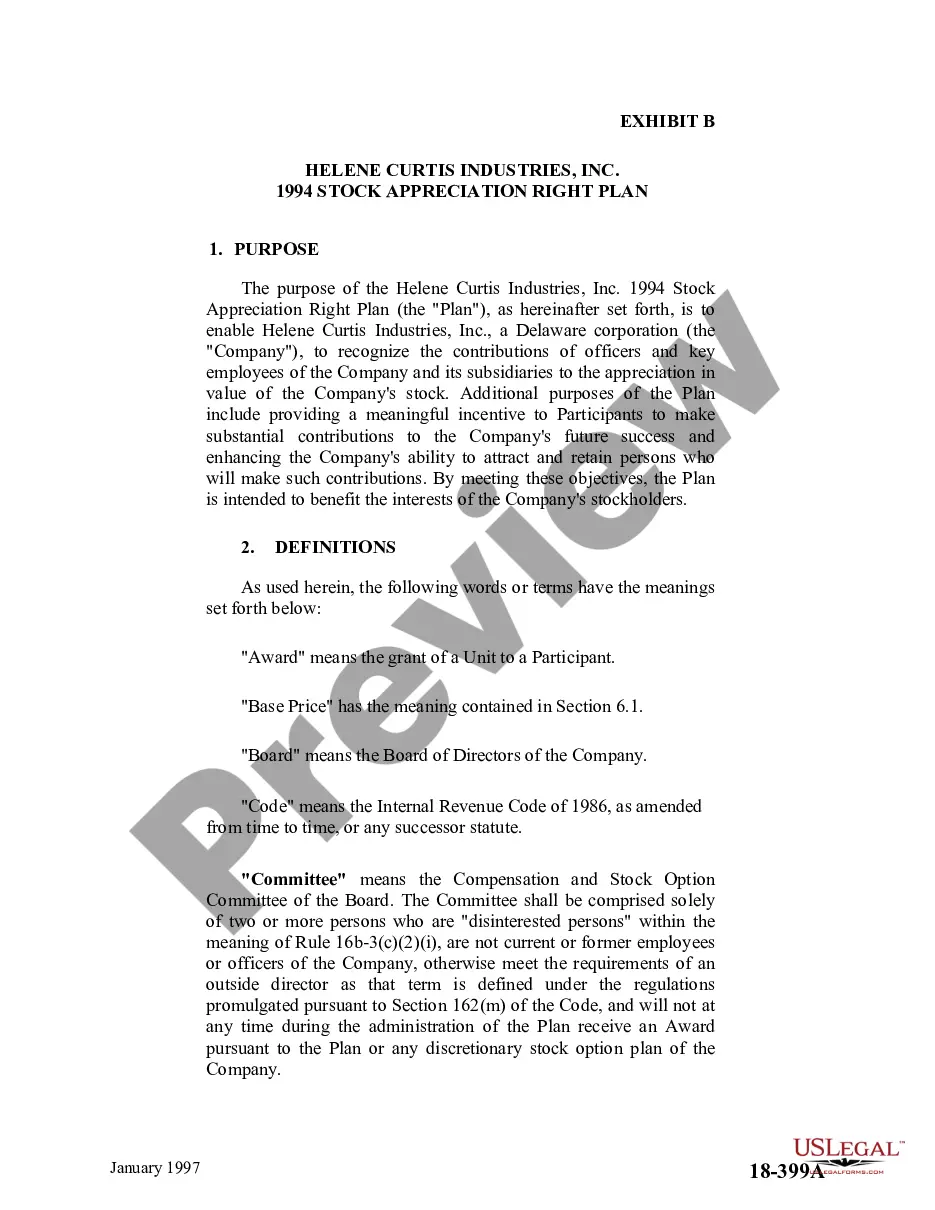

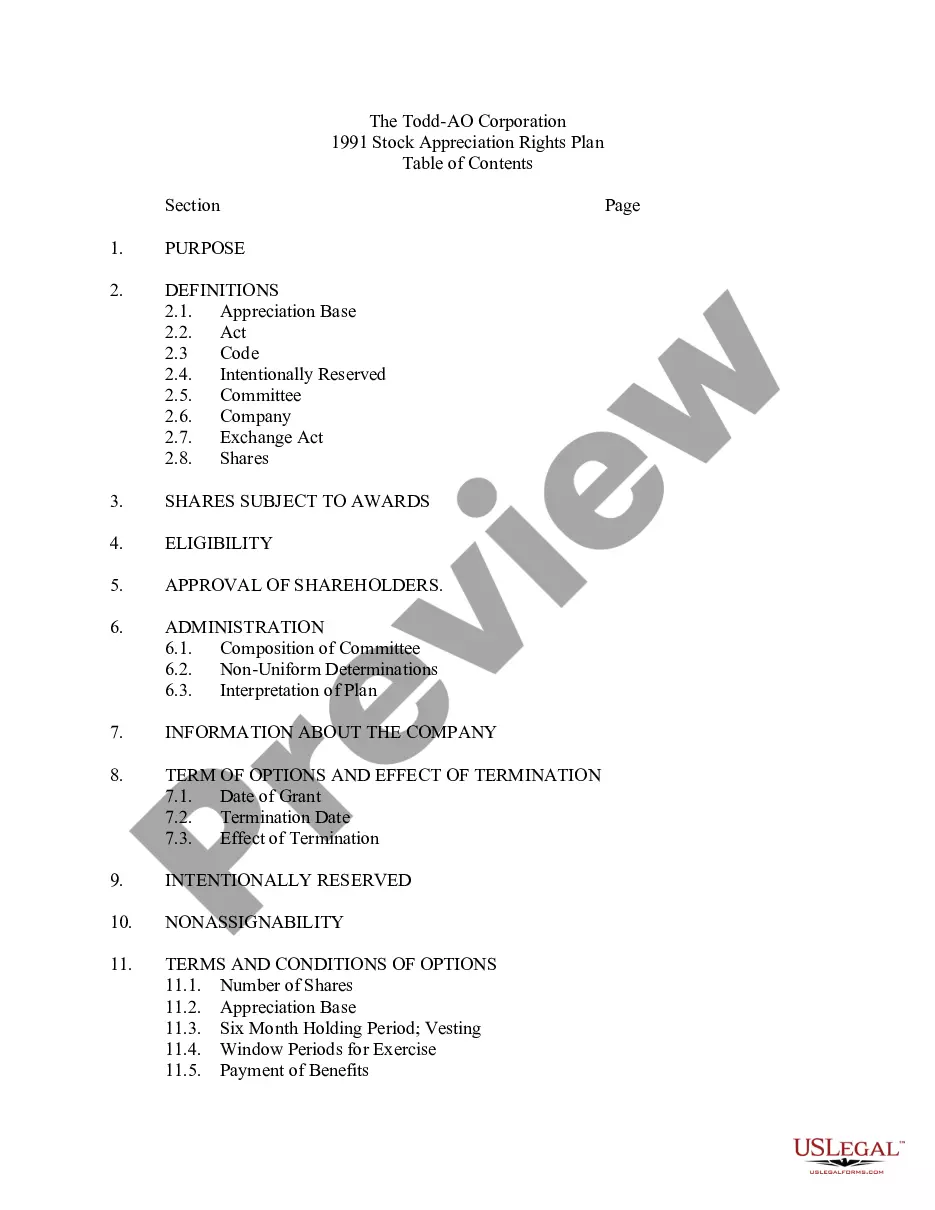

18-400D 18-400D . . . Share Appreciation Rights Plan under which stock option committee determines to whom units are awarded, number of units to be awarded and terms of such units. On grant date, committee assigns each unit a base value which cannot be less than market value of share of common stock on that date. Each award becomes exercisable with respect to 25% of units awarded on each of first four anniversaries of grant date, provided grantee has been continually employed full-time by corporation or subsidiary. Units may be exercised, to extent vested, at any time until five years after grant date. Upon exercise of vested units, grantee is entitled to receive net appreciation of such units in cash or in shares of common stock, as determined by committee

New Hampshire Share Appreciation Rights Plan with amendment

Category:

State:

Multi-State

Control #:

US-CC-18-400D

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Share Appreciation Rights Plan With Amendment?

Choosing the best legitimate file template can be a have a problem. Naturally, there are plenty of themes accessible on the Internet, but how do you get the legitimate type you need? Take advantage of the US Legal Forms internet site. The services delivers thousands of themes, like the New Hampshire Share Appreciation Rights Plan with amendment, that can be used for organization and private requirements. Each of the kinds are examined by specialists and meet federal and state requirements.

In case you are currently registered, log in to the bank account and then click the Down load key to get the New Hampshire Share Appreciation Rights Plan with amendment. Use your bank account to check with the legitimate kinds you may have purchased earlier. Proceed to the My Forms tab of the bank account and obtain an additional backup of the file you need.

In case you are a brand new customer of US Legal Forms, allow me to share easy recommendations so that you can adhere to:

- First, be sure you have selected the appropriate type for the metropolis/county. It is possible to examine the form utilizing the Preview key and read the form description to ensure it will be the best for you.

- In the event the type fails to meet your requirements, take advantage of the Seach field to find the correct type.

- Once you are sure that the form is acceptable, select the Purchase now key to get the type.

- Choose the costs plan you want and enter the required details. Design your bank account and purchase an order using your PayPal bank account or Visa or Mastercard.

- Select the submit structure and obtain the legitimate file template to the gadget.

- Complete, edit and print out and sign the attained New Hampshire Share Appreciation Rights Plan with amendment.

US Legal Forms may be the most significant local library of legitimate kinds where you can find a variety of file themes. Take advantage of the company to obtain appropriately-manufactured papers that adhere to state requirements.

Form popularity

FAQ

Stock Appreciation Right (SAR) entitles an employee, who is a shareholder in a company, to a cash payment proportionate to the appreciation of stock traded on a public exchange market. SAR programs provide companies with the flexibility to structure the compensation scheme in a way that suits their beneficiaries.

SARs are not explicitly defined in Canada's Income Tax Act, but they are commonly known as phantom plans that entitle the participant to receive an amount equal to the appreciation in the value of the underlying shares from the date that the SAR is granted until the date that it is exercised.

Stock appreciation rights (SARs) are a type of employee compensation linked to the company's stock price during a preset period. Unlike stock options, SARs are often paid in cash and do not require the employee to own any asset or contract.

However, when a stock appreciation right is exercised, the employee does not have to pay to acquire the underlying security. Instead, the employee receives the appreciation in value of the underlying security, which would equal the current market value less the grant price.

How do I value it? For purposes of financial disclosure, you may value a stock appreciation right based on the difference between the current market value and the grant price. This formula is: (current market value ? grant price) x number of shares = value.

A ?Stock Appreciation Right? is the right to receive a payment from the Company in an amount equal to the ?Spread,? which is defined as the excess of the Fair Market Value (as defined in Plan) of one share of common stock, $1.00 par value (the ?Stock?) of the Company at the Exercise Date (as defined below) over a ...

A SAR is very similar to a stock option, but with a key difference. When a stock option is exercised, an employee has to pay the grant price and acquire the underlying security. However, when a SAR is exercised, the employee does not have to pay to acquire the underlying security.

Grant: Like stock options, there are no federal income tax consequences when you are granted SARs. Vesting: Again, no tax consequences at the time of vesting like options.