New Hampshire Waiver of Qualified Joint and Survivor Annuity - QJSA

Description

How to fill out Waiver Of Qualified Joint And Survivor Annuity - QJSA?

Have you found yourself in the scenario where you need documents for either business or personal purposes nearly every day.

There are numerous legal document templates accessible online, but discovering ones you can rely on isn't simple.

US Legal Forms provides a vast array of template formats, including the New Hampshire Waiver of Qualified Joint and Survivor Annuity - QJSA, which can be tailored to meet state and federal requirements.

Once you have the correct template, click on Buy now.

Choose the pricing plan you desire, provide the necessary details to create your account, and pay for the order using your PayPal or credit card. Select a convenient file format and download your copy. Access all the document templates you have purchased in the My documents menu. You can obtain an additional copy of the New Hampshire Waiver of Qualified Joint and Survivor Annuity - QJSA at any time, if needed. Click the desired template to download or print the document format. Leverage US Legal Forms, one of the most extensive collections of legal templates, to save time and prevent errors. The service provides properly crafted legal document templates that you can use for various purposes. Create an account on US Legal Forms and start simplifying your life.

- If you are already acquainted with the US Legal Forms website and possess an account, simply Log In.

- Then, you can download the New Hampshire Waiver of Qualified Joint and Survivor Annuity - QJSA template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Obtain the template you require and ensure it is for the correct municipality/region.

- Utilize the Preview feature to review the document.

- Examine the outline to confirm that you have selected the correct template.

- If the template isn't what you're seeking, use the Lookup field to find the template that fits your needs.

Form popularity

FAQ

The New Hampshire Waiver of Qualified Joint and Survivor Annuity - QJSA offers several advantages. First, it provides financial security for you and your spouse, ensuring that income continues after one partner's death. Additionally, waiving a QJSA may allow greater flexibility in how you manage your retirement funds, potentially leading to higher returns. Overall, this approach can enhance your retirement planning.

A joint and survivor annuity is an insurance product designed for couples that continues to make regular payments as long as one spouse lives. A joint and survivor annuity has the advantage of providing income if one or both people live longer than expected. This is not a good choice for a younger couple.

QJSA rules apply to money-purchase pension plans, defined benefit plans, and target benefits. They can also apply to profit-sharing and 401(k) and 403(b) plans, but only if so elected under the plan.

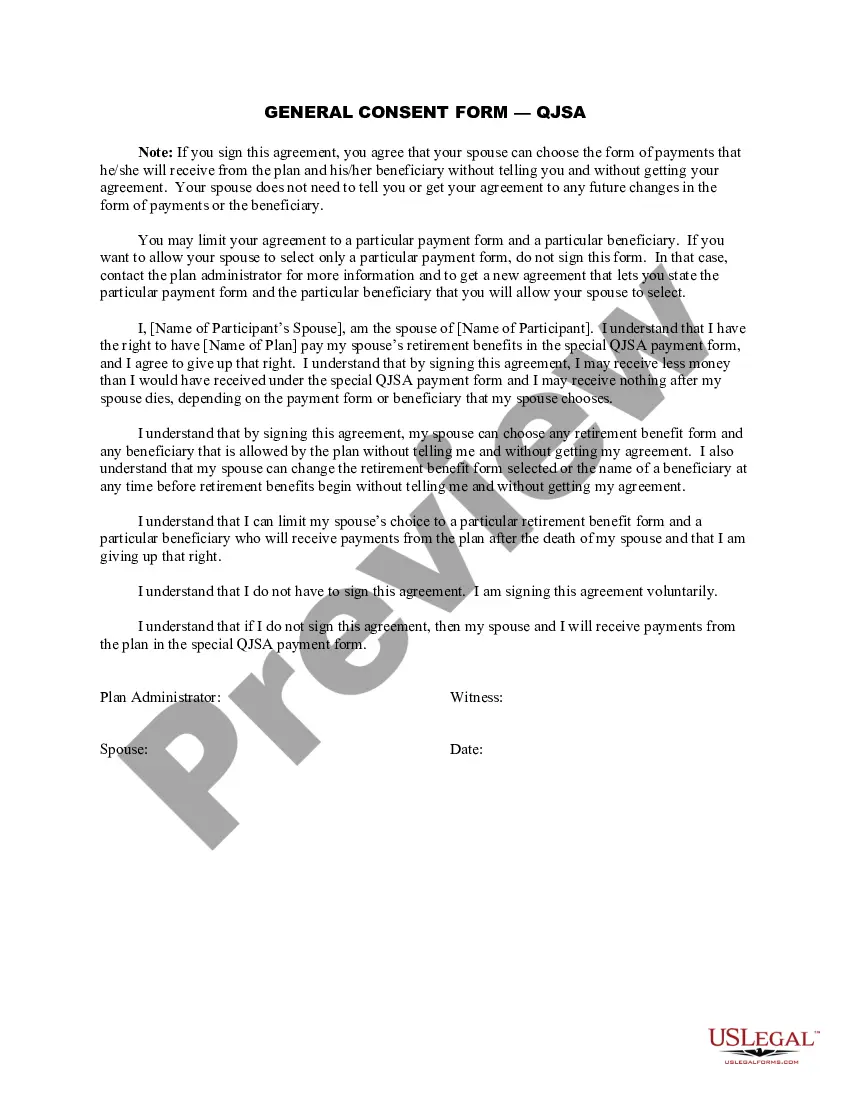

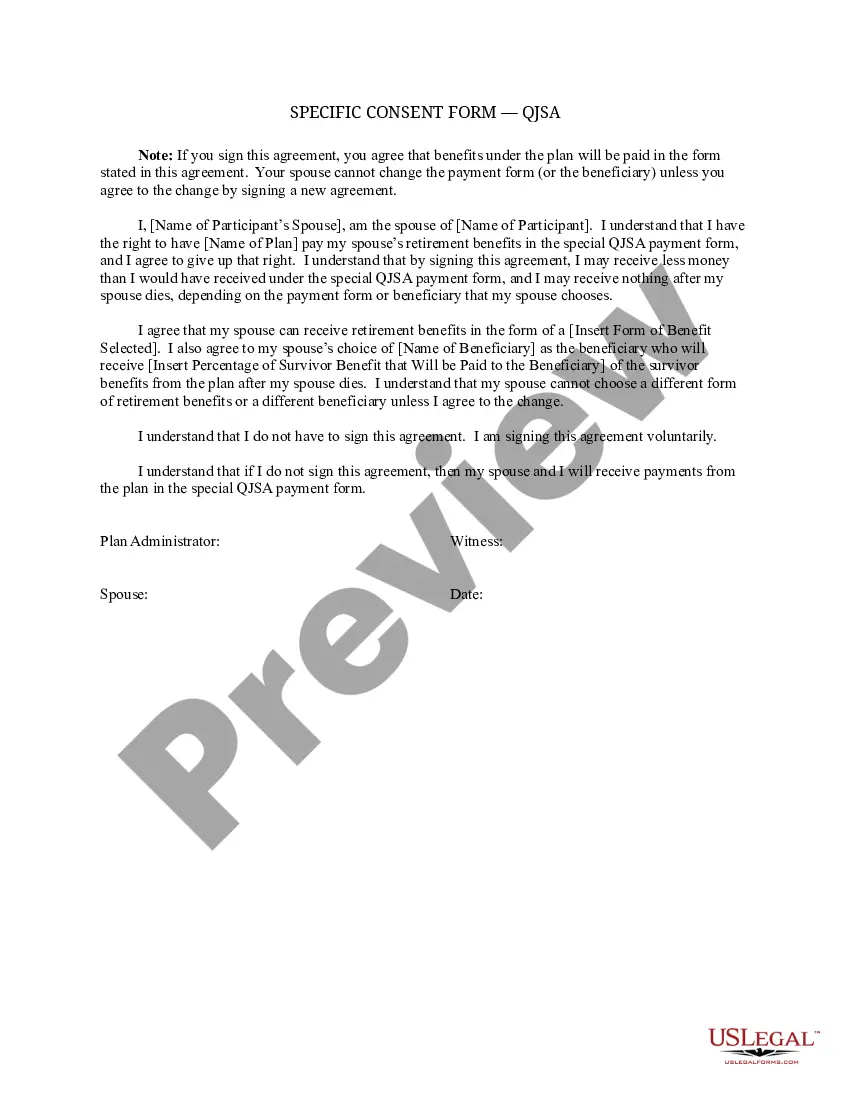

When the participant dies, the spouse will receive lifetime payments in the same or reduced amount. The participant may waive the Qualified Joint and Survivor Annuity with spousal consent and elect to receive another form of payment.

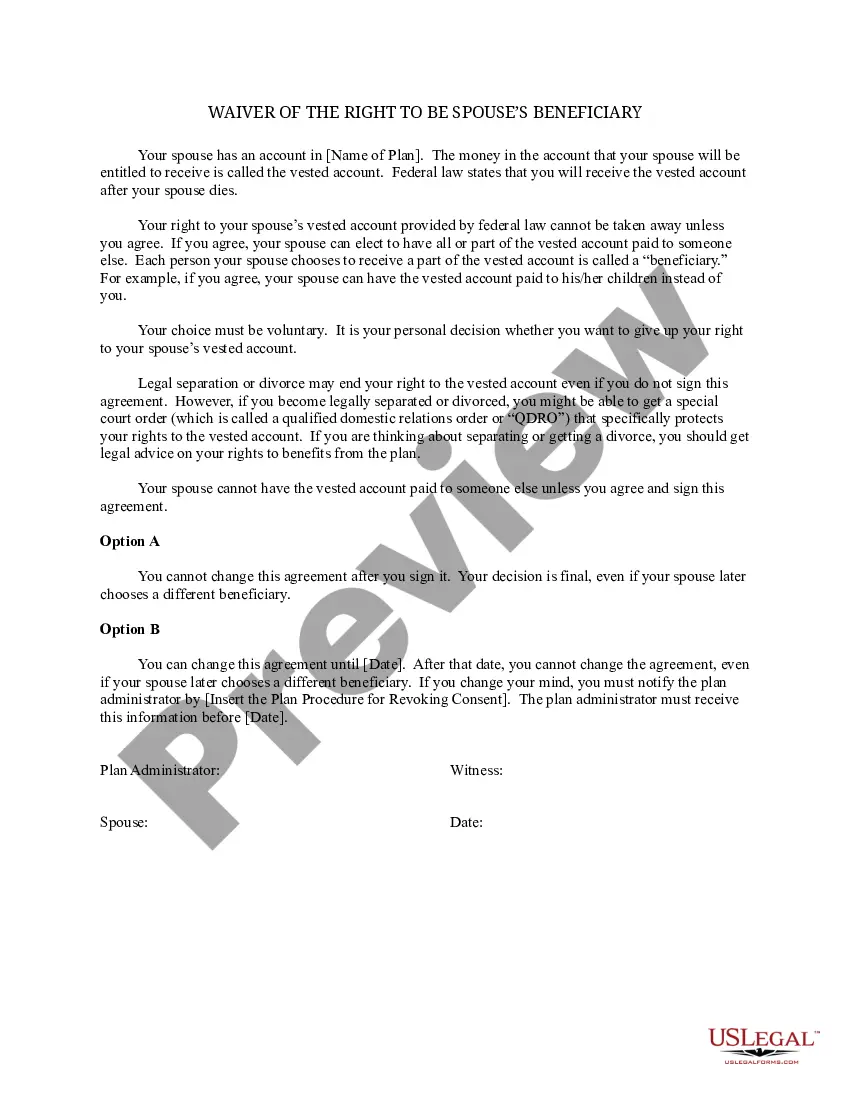

If you do not waive the QPSA, after your death the Plan will pay your spouse the QPSA unless your spouse elects another benefit form. The QPSA will not pay benefits to other beneficiaries after your spouse dies. If you waive the QPSA, the Plan will pay your account to your designated beneficiary.

This special payment form is often called a qualified joint and survivor annuity or QJSA payment form. This benefit is paid to the participant each year and, on the participant's death, a survivor annuity is paid to the surviving spouse.

This benefit provides payments to the participant's spouse for his or her lifetime equal to a percentage (as specified in the Pension Plan) not less than one-half of the annuity that would have been payable during their joint lives. The participant may waive the Qualified Preretirement Survivor Annuity.

This benefit provides payments to the participant's spouse for his or her lifetime equal to a percentage (as specified in the Pension Plan) not less than one-half of the annuity that would have been payable during their joint lives. The participant may waive the Qualified Preretirement Survivor Annuity.

Qualified Joint and Survivor AnnuityIf your spouse consents to change the way the Plan's retirement benefits are paid, your spouse gives up his or her right to the QJSA payments. This is referred to as a waiver of the QJSA payment form.

life annuity provides the largest monthly payment but pays only during your lifetime. It's a poor choice if your spouse will need income from your pension to pay routine expenses. A jointandsurvivor annuity pays you during your lifetime and then continues to pay your spouse or other named beneficiary.