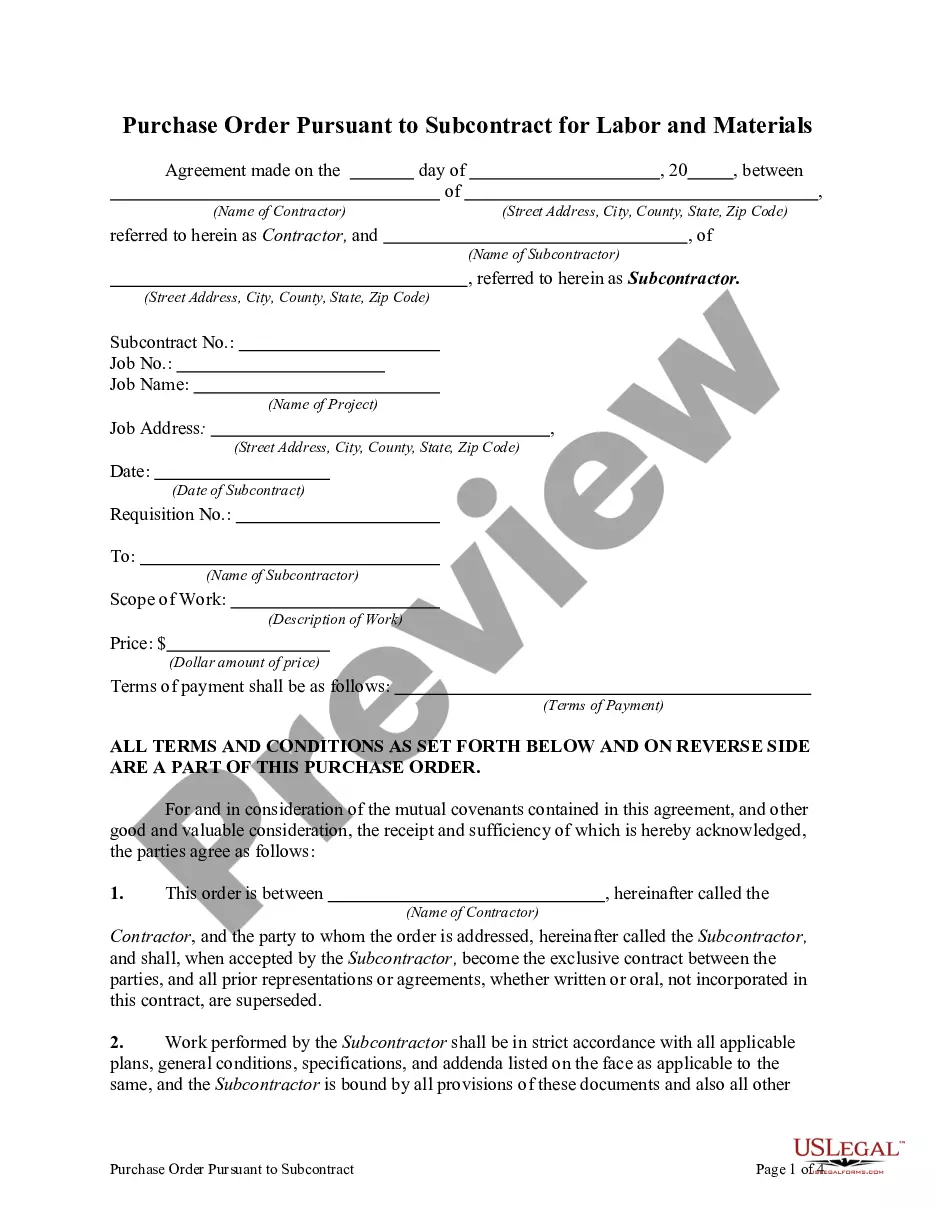

Nebraska Subcontract Purchase Order for Labor and Materials

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Subcontract Purchase Order For Labor And Materials?

You can spend time online attempting to discover the legal document format that adheres to the federal and state requirements you will need.

US Legal Forms provides a vast array of legal documents that can be reviewed by experts.

You can actually download or print the Nebraska Subcontract Purchase Order for Labor and Materials from the offered services.

If available, take advantage of the Preview button to examine the format as well.

- If you possess a US Legal Forms account, you can Log In and click on the Acquire button.

- Subsequently, you can complete, edit, print, or sign the Nebraska Subcontract Purchase Order for Labor and Materials.

- Every legal document format you obtain is yours permanently.

- To obtain another copy of the downloaded form, visit the My documents tab and click on the appropriate button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have selected the correct format for your desired region/area.

- Review the form description to ensure you have chosen the correct form.

Form popularity

FAQ

Yes, Nebraska requires a contractor's license for most construction-related activities. If you plan to use a Nebraska Subcontract Purchase Order for Labor and Materials, having the proper licensing is crucial. This ensures that you comply with state regulations and protects you from potential legal issues. For assistance in obtaining a contractor's license and navigating related processes, consider using the resources on the US Legal Forms platform.

In Nebraska, the taxation of labor depends on the type of work being performed. Generally, most labor services related to tangible personal property are taxable. It is essential to determine the specific application of tax laws, especially when issuing a Nebraska Subcontract Purchase Order for Labor and Materials, to ensure adherence to state tax regulations.

In Nebraska, sales tax is levied on most goods and some services, including construction materials. Understanding what is taxed is key for contractors, as it will directly influence the financial aspects of your project. Your Nebraska Subcontract Purchase Order for Labor and Materials should accurately reflect these tax obligations to avoid compliance issues.

An Option 2 contractor in Nebraska refers to a contractor who qualifies under specific criteria outlined by the state regulations. These criteria often pertain to experience levels and the types of projects being undertaken. Understanding this classification can help in aligning your Nebraska Subcontract Purchase Order for Labor and Materials with the correct contractor capabilities.

The Contractor Registration Act in Nebraska mandates all contractors to register with the state. This act ensures that contractors meet certain qualifications and adhere to legal standards for construction projects. By understanding this act, you can better navigate your Nebraska Subcontract Purchase Order for Labor and Materials, aligning your operations with state requirements.

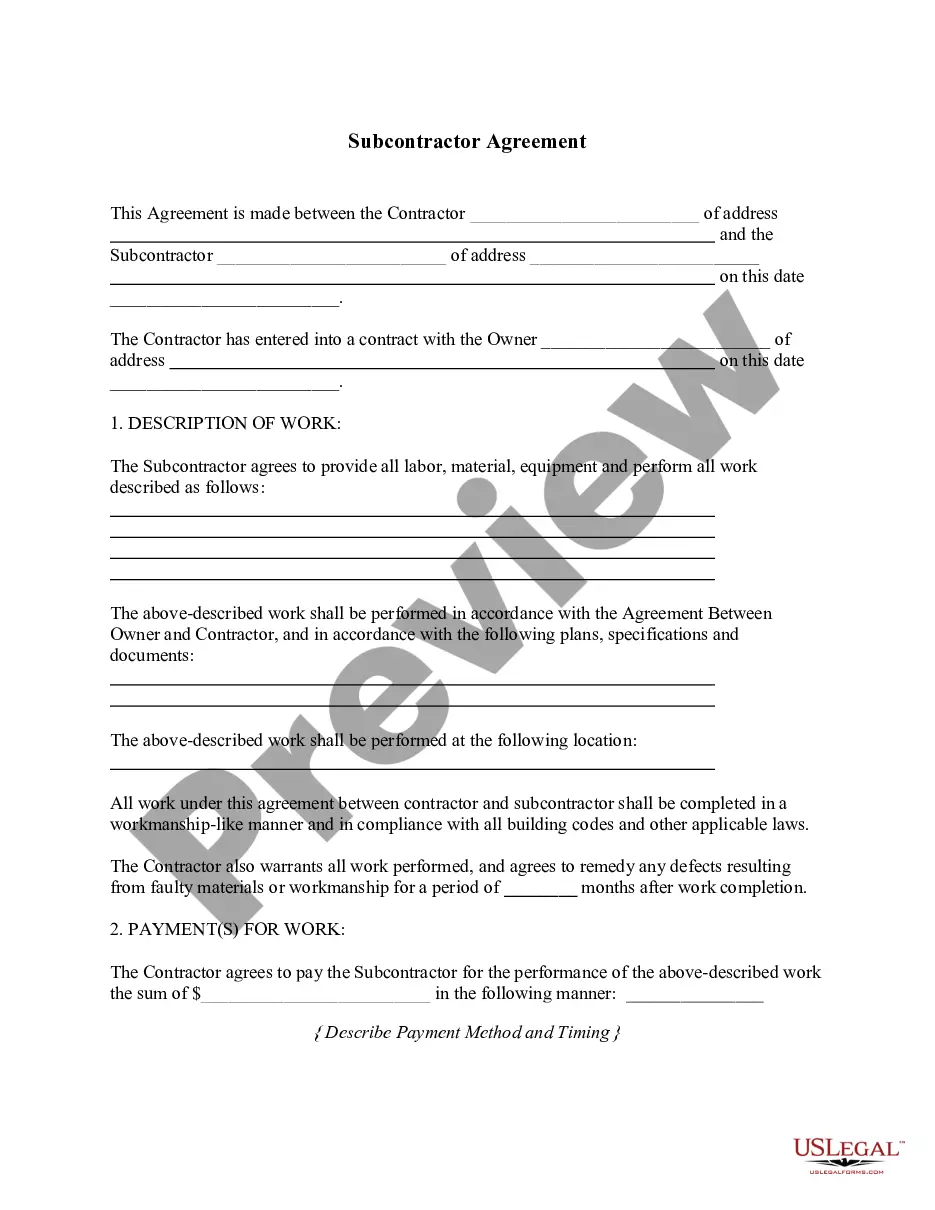

To draft a subcontract effectively, begin by clearly outlining the scope of work and specific duties required. Include essential terms such as payment details, timelines, and dispute resolution processes. Utilize a Nebraska Subcontract Purchase Order for Labor and Materials to ensure compliance with state regulations and to protect both parties involved.

The seven steps of the procurement process include need recognition, specification development, supplier search, proposal evaluation, negotiation, order placement, and contract management. Utilizing a Nebraska Subcontract Purchase Order for Labor and Materials ensures that all essential procedures are documented. This structured approach enhances collaboration and communication among all parties involved.

The five steps of the procurement process usually consist of identifying needs, creating specifications, sourcing suppliers, evaluating bids, and selecting the supplier. Involving a Nebraska Subcontract Purchase Order for Labor and Materials in this process helps clarify responsibilities and expectations. Following these steps systematically can lead to successful project completion.

Yes, construction labor is generally taxable in Nebraska. However, specific exemptions may apply based on the nature of the contract or project type. For accurate understanding and guidance regarding tax obligations related to a Nebraska Subcontract Purchase Order for Labor and Materials, consulting legal experts or tax professionals is advisable.

The four steps of the procurement process typically include identifying needs, choosing suppliers, placing orders, and receiving the goods or services. When applying this to a Nebraska Subcontract Purchase Order for Labor and Materials, each step is crucial to ensure quality and efficiency. Following these stages helps in managing resources effectively and meeting project requirements.