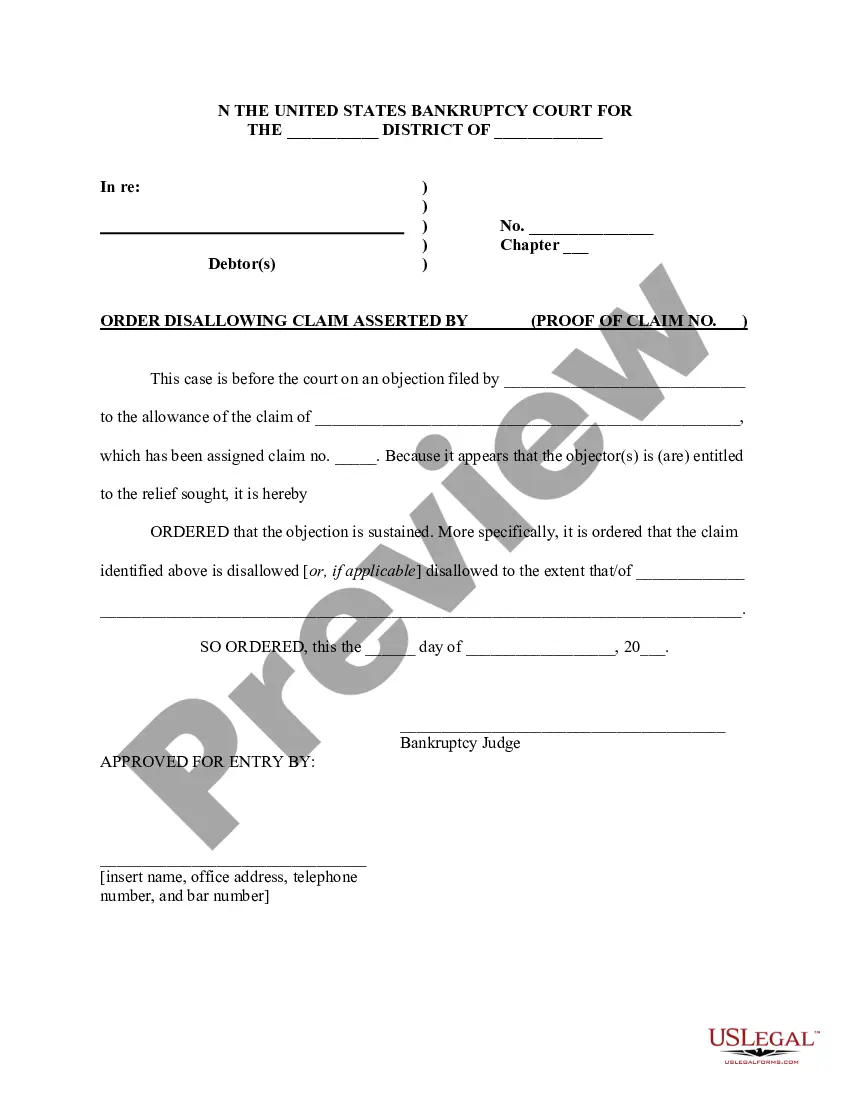

If you have to comprehensive, obtain, or print authorized papers themes, use US Legal Forms, the biggest selection of authorized forms, which can be found online. Utilize the site`s basic and handy search to discover the documents you need. A variety of themes for organization and specific purposes are categorized by categories and claims, or key phrases. Use US Legal Forms to discover the Nebraska Objection to Allowed Claim in Accounting within a couple of clicks.

In case you are presently a US Legal Forms consumer, log in in your accounts and then click the Download switch to find the Nebraska Objection to Allowed Claim in Accounting. You can also accessibility forms you formerly downloaded from the My Forms tab of your own accounts.

If you work with US Legal Forms the first time, refer to the instructions beneath:

- Step 1. Be sure you have chosen the form for your appropriate metropolis/land.

- Step 2. Utilize the Preview method to examine the form`s content. Don`t overlook to read through the description.

- Step 3. In case you are unhappy together with the develop, make use of the Research field near the top of the monitor to locate other models from the authorized develop template.

- Step 4. Once you have identified the form you need, click on the Buy now switch. Select the pricing program you choose and add your qualifications to register for an accounts.

- Step 5. Approach the financial transaction. You can use your Мisa or Ьastercard or PayPal accounts to perform the financial transaction.

- Step 6. Choose the format from the authorized develop and obtain it on your gadget.

- Step 7. Total, edit and print or indicator the Nebraska Objection to Allowed Claim in Accounting.

Every single authorized papers template you get is the one you have permanently. You have acces to each develop you downloaded within your acccount. Go through the My Forms section and pick a develop to print or obtain again.

Remain competitive and obtain, and print the Nebraska Objection to Allowed Claim in Accounting with US Legal Forms. There are millions of professional and condition-certain forms you may use for the organization or specific requirements.