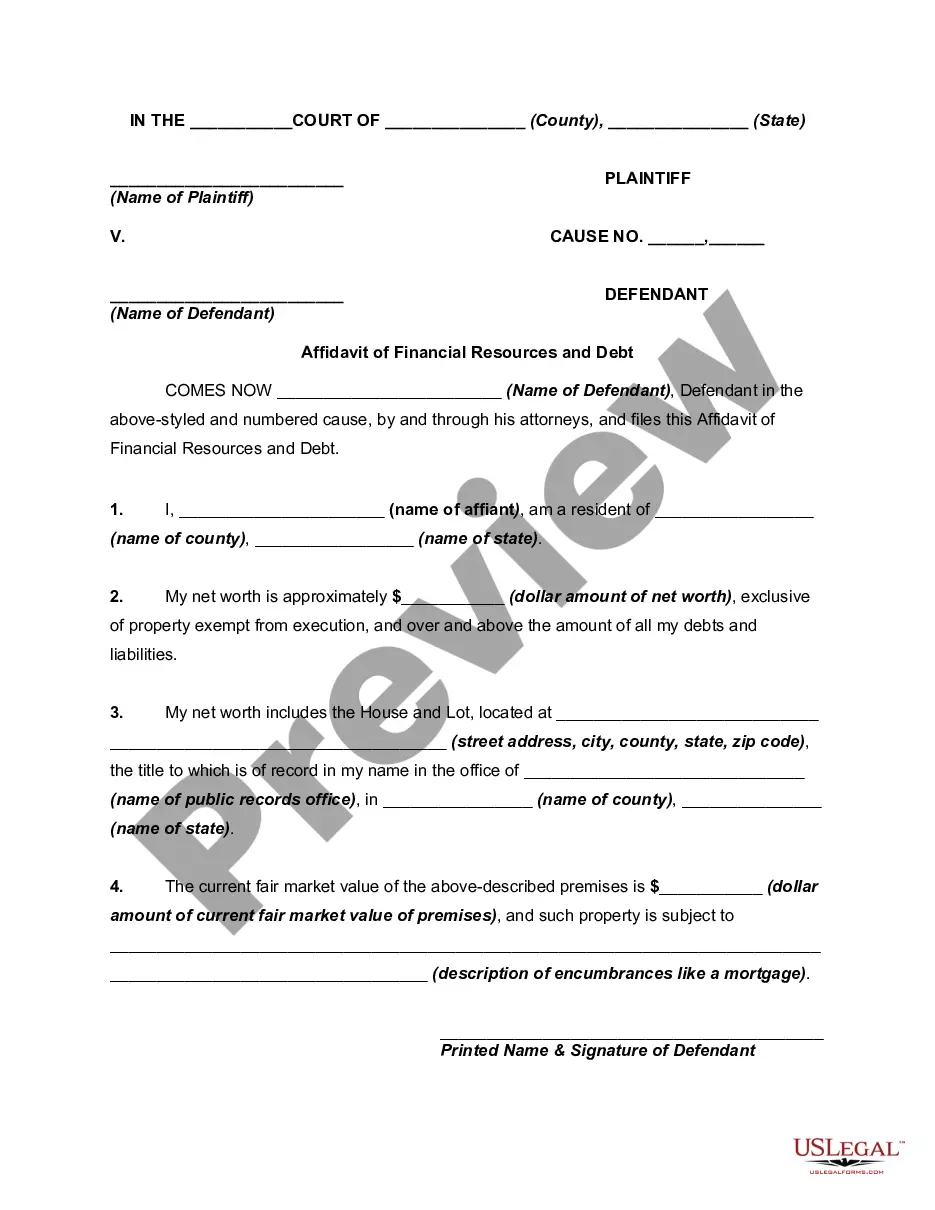

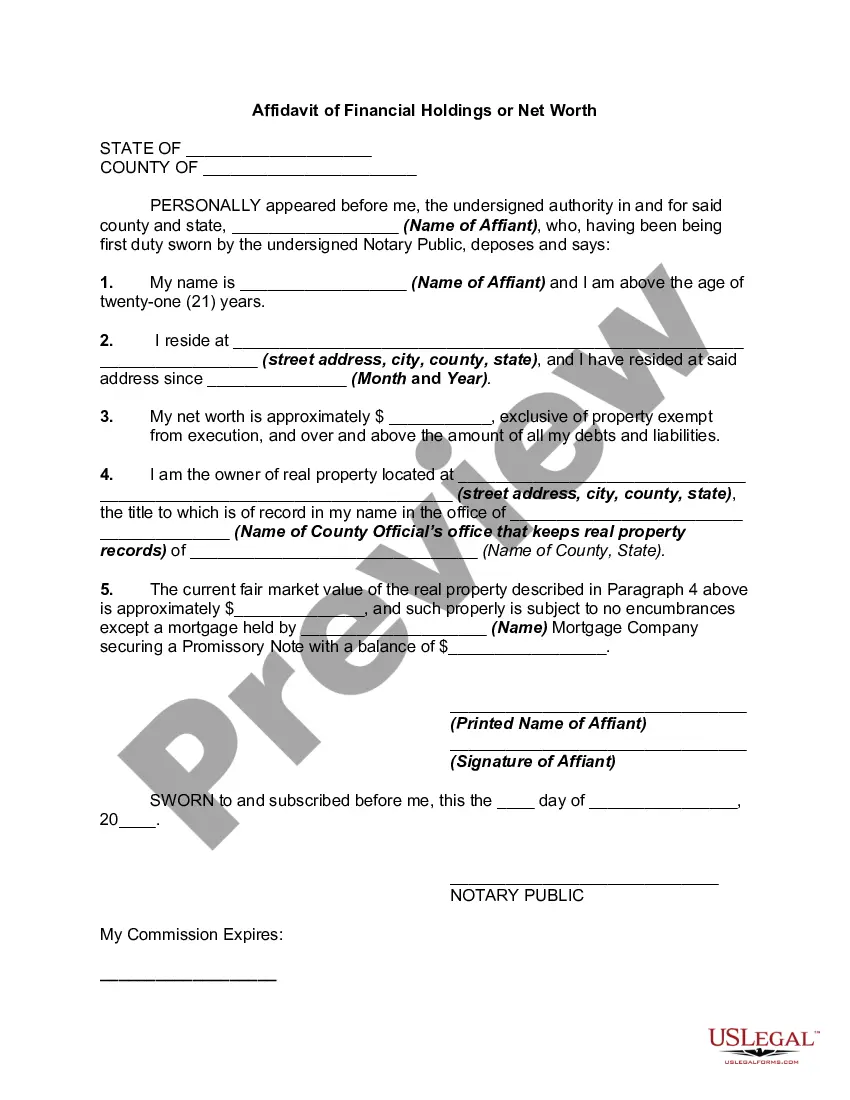

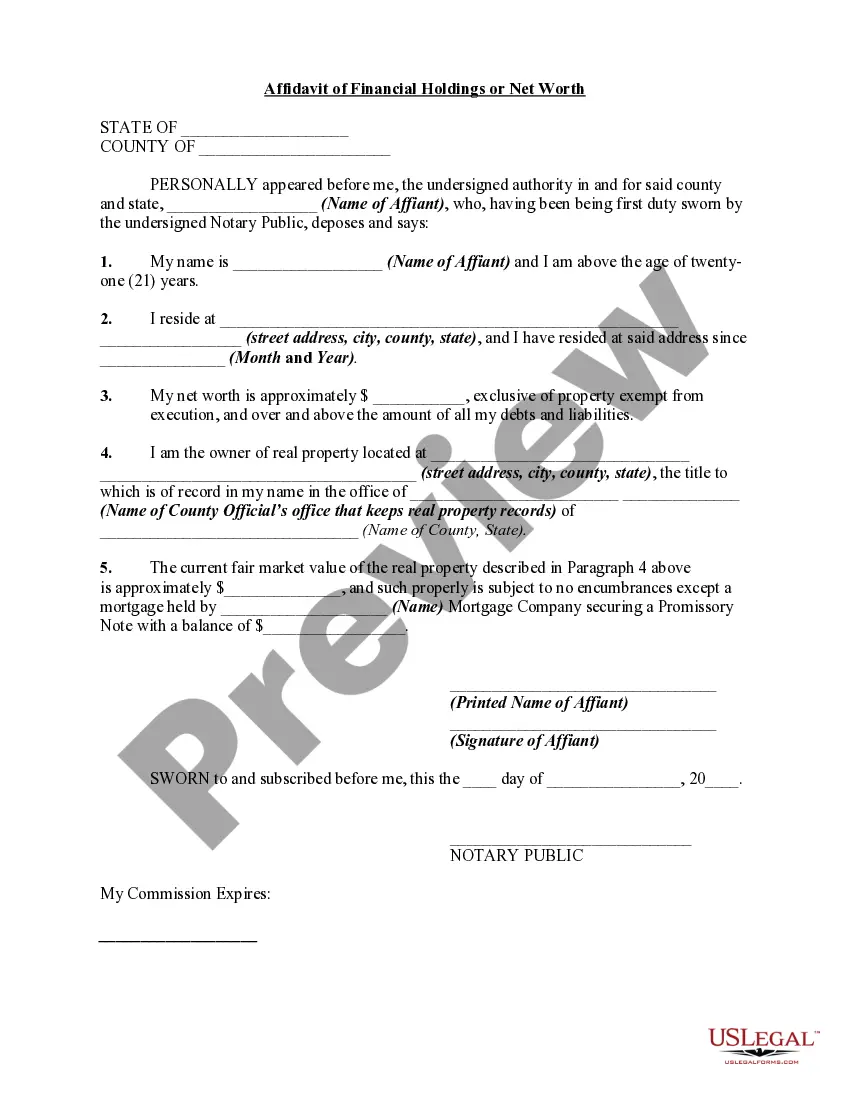

The purpose of this form is to show creditors the dire financial situation that the debtor is in so as to induce the creditors to compromise or write off the debt due.

Nebraska Debtor's Affidavit of Financial Status to Induce Creditor to Compromise or Write off the Debt which is Past Due - Assets and Liabilities

Instant download

Description

Free preview

How to fill out Debtor's Affidavit Of Financial Status To Induce Creditor To Compromise Or Write Off The Debt Which Is Past Due - Assets And Liabilities?

Are you presently in a situation where you occasionally require documentation for either professional or personal reasons nearly every day.

There are numerous authentic form templates available online, but finding templates that you can depend on is challenging.

US Legal Forms offers a vast array of document templates, such as the Nebraska Debtor's Affidavit of Financial Status to Induce Creditor to Compromise or Write off the Debt that is Overdue - Assets and Liabilities, designed to comply with federal and state regulations.

Choose a suitable document format and download your copy.

Access all the document templates you have purchased in the My documents section. You can acquire another copy of the Nebraska Debtor's Affidavit of Financial Status to Induce Creditor to Compromise or Write off the Debt that is Overdue - Assets and Liabilities at any time if needed. Click the desired form to download or print the document template.

- If you are already familiar with the US Legal Forms website and possess an account, just Log In.

- After logging in, you can download the Nebraska Debtor's Affidavit of Financial Status to Induce Creditor to Compromise or Write off the Debt that is Overdue - Assets and Liabilities template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Find the form you need and ensure it pertains to your specific city/county.

- Utilize the Preview button to examine the form.

- Check the summary to confirm you have selected the appropriate form.

- If the form is not what you seek, employ the Look for field to locate the form that matches your needs and specifications.

- Once you find the correct form, click Purchase now.

- Select the pricing plan you prefer, provide the required information to create your account, and complete your order using your PayPal or Credit Card.

Form popularity

FAQ

A creditor will usually object to the discharge of its particular debt when fraud or an intentional wrongful act occurs before the bankruptcy case. For instance, examples of nondischargeable debts, if proven, could include: The costs and damages caused by intentional and spiteful conduct.

If a creditor chooses to object to bankruptcy, it must file an official objection in court, called an adversary proceeding. In order to halt the discharge, the creditor objects to specific discharges on a limited set of legal grounds. If the court grants the objection, you'll remain responsible for paying the debt.

A Chapter 13 Plan may modify an automobile lien and if the plan completes and you receive a discharge the debt will be gone and the car lienholder is obligated to release its lien upon discharge. In certain circumstances a Chapter 13 Plan and subsequent discharge may avoid a second or third mortgage lien.

This chapter of the Bankruptcy Code generally provides for reorganization, usually involving a corporation or partnership. A chapter 11 debtor usually proposes a plan of reorganization to keep its business alive and pay creditors over time.

The word bankrupt comes from the Latin banca rupta, which literally means broken bench, after the practice of moneylenders breaking the table they used when they were no longer in business.

Chapter 11 bankruptcy is the formal process that allows debtors and creditors to resolve the problem of the debtor's financial shortcomings through a reorganization plan. Accordingly, the central goal of chapter 11 is to create a viable economic entity by reorganizing the debtor's debt structure.

Although it doesn't happen in most consumer cases, creditors have the ability to object to having their debt discharged. Some debts are not dischargeable by default. Others become non-dischargeable once a creditor objects and the court finds that cause exists to exclude a certain debt from being discharged.

Discharge Time Frame Getting a discharge in a Chapter 13 case generally takes between six and eight weeks after making your plan's final payment. This time frame depends upon the court's caseload the busier the court, the longer you may have to wait for your discharge letter.

In a Chapter 7 bankruptcy, a creditor or trustee can either object to the discharge of a particular debt or they can object to the discharge of all of your debts. If a creditor objects to a specific debt, it will not affect any of the other debts in your case.

Getting a discharge means that your personal liability on qualifying debt is wiped out, and the creditor can no longer do anything to collect the debt from you. Creditors aren't allowed to call you, sue you, garnish your wages, or continue any other collection efforts on the discharged debt.