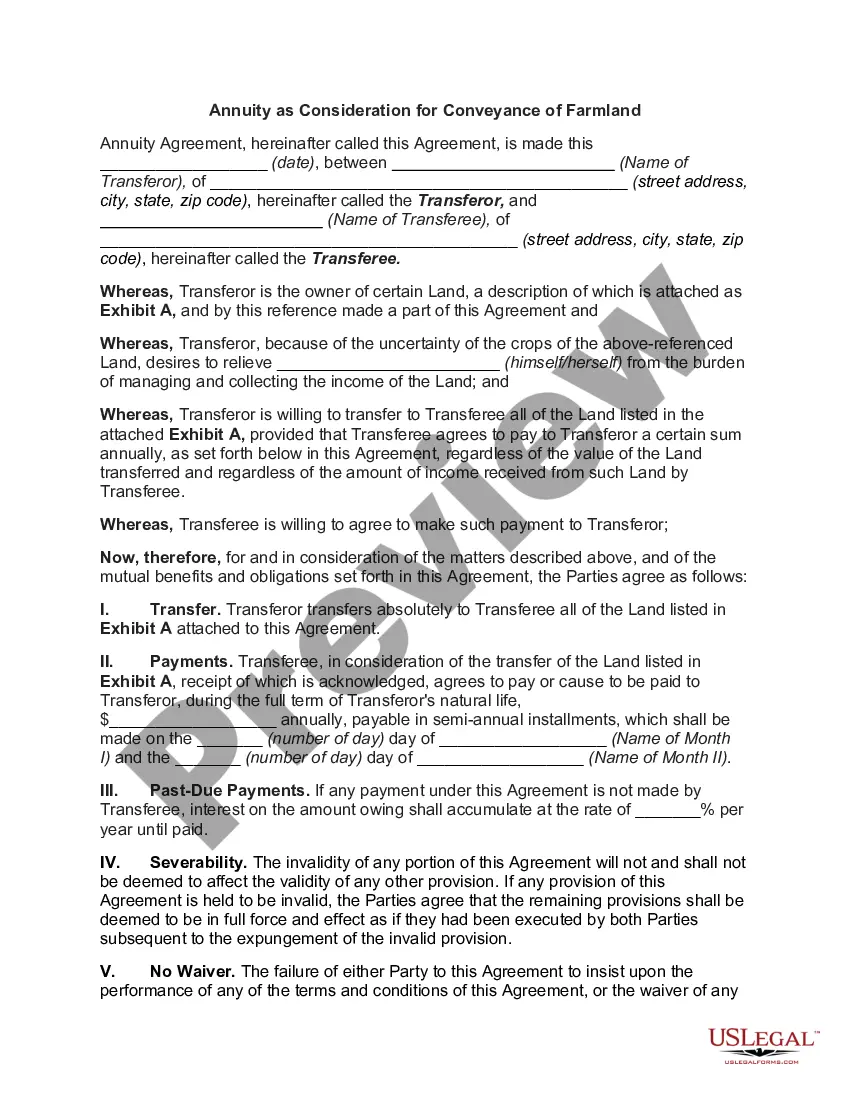

Montana Private Annuity Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Private Annuity Agreement?

US Legal Forms - one of the most important collections of legal documents in the United States - offers a wide selection of legal document templates available for download or creation.

By using the website, you can find numerous forms for both business and personal purposes, organized by categories, states, or keywords. You can access the latest versions of documents like the Montana Private Annuity Agreement within moments.

If you already have an account, Log In to download the Montana Private Annuity Agreement from the US Legal Forms library. The Download button will appear on every document you view. You can access all previously saved forms in the My documents section of your account.

Complete the transaction. Use your credit card or PayPal account to finalize the purchase.

Select the format and download the document to your device. Edit. Fill in, modify, print, and sign the downloaded Montana Private Annuity Agreement. Every template you add to your account has no expiration date and is yours indefinitely. Therefore, to download or create an additional copy, simply return to the My documents section and click on the form you desire. Access the Montana Private Annuity Agreement with US Legal Forms, one of the most extensive libraries of legal document templates. Utilize a multitude of professional and state-specific templates that cater to your business or personal requirements.

- Ensure you have chosen the correct form for your city/county.

- Click on the Review button to check the content of the form.

- Refer to the form description to confirm that you have selected the appropriate document.

- If the form does not meet your needs, utilize the Search feature at the top of the screen to find a suitable one.

- If you are satisfied with the form, confirm your choice by clicking the Get now button.

- Choose your preferred payment plan and provide your details to register for an account.

Form popularity

FAQ

You can roll-over your annuity IRA to a self-directed IRA. You'll need to cash-out the IRA, pay any applicable surrender charges, and then instruct the annuity company to process a direct roll-over of the funds to your self-directed IRA custodian as a direct rollover.

An annuity is a long-term investment that is issued by an insurance company and is designed to help protect you from the risk of outliving your income. Through annuitization, your purchase payments (what you contribute) are converted into periodic payments that can last for life.

There are four basic types of annuities to meet your needs: immediate fixed, immediate variable, deferred fixed, and deferred variable annuities. These four types are based on two primary factors: when you want to start receiving payments and how you would like your annuity to grow.

What's an annuity contract? In the simplest terms, an annuity is a financial contract between a person and an insurance company that provides retirement income or death benefits.

There are three parties to every annuity contract the owner, the annuitant, and the beneficiary. The owner controls the contract. The owner can add and withdraw money, change parties to the annuity, and terminate the contract. The annuitant is similar to the insured in a life insurance policy.

There are four parties to an annuity contract: the annuity issuer, the owner, the annuitant, and the beneficiary. The annuity issuer is the company (e.g., an insurance company) that issues the annuity.

In the simplest terms, an annuity is a financial contract between a person and an insurance company that provides retirement income or death benefits.

An annuity is a contract between you and an insurance company that requires the insurer to make payments to you, either immediately or in the future. You buy an annuity by making either a single payment or a series of payments.

Annuitants pay taxes as they receive payments from their annuity. The tax rate depends on a variety of factors, including the type of annuity, payout option, and type of funds used for the premium. Some people use pre-tax dollars, such as funds from a 401(k) or IRA, to buy an annuity.

There are three parties to an annuity contract: the owner, annuitant and the beneficiary. The owner makes the initial investment, decides when to begin taking income and can change the beneficiary designation at will. The annuitant's life is used to determine the benefits to be paid out under the contract.