Courts vary in their approach to enforcing releases depending on the particular facts of each case, the effect of the release on other statutes and laws, and the view of the court of the benefits of releases as a matter of public policy. Many courts will invalidate documents signed on behalf of minors. Also, Courts do not permit persons to waive their responsibility when they have exercised gross negligence or misconduct that is intentional or criminal in nature. Such an agreement would be deemed to be against public policy because it would encourage dangerous and illegal behavior.

A lactation consultant is a healthcare provider recognized as having expertise in the fields of human lactation and breastfeeding

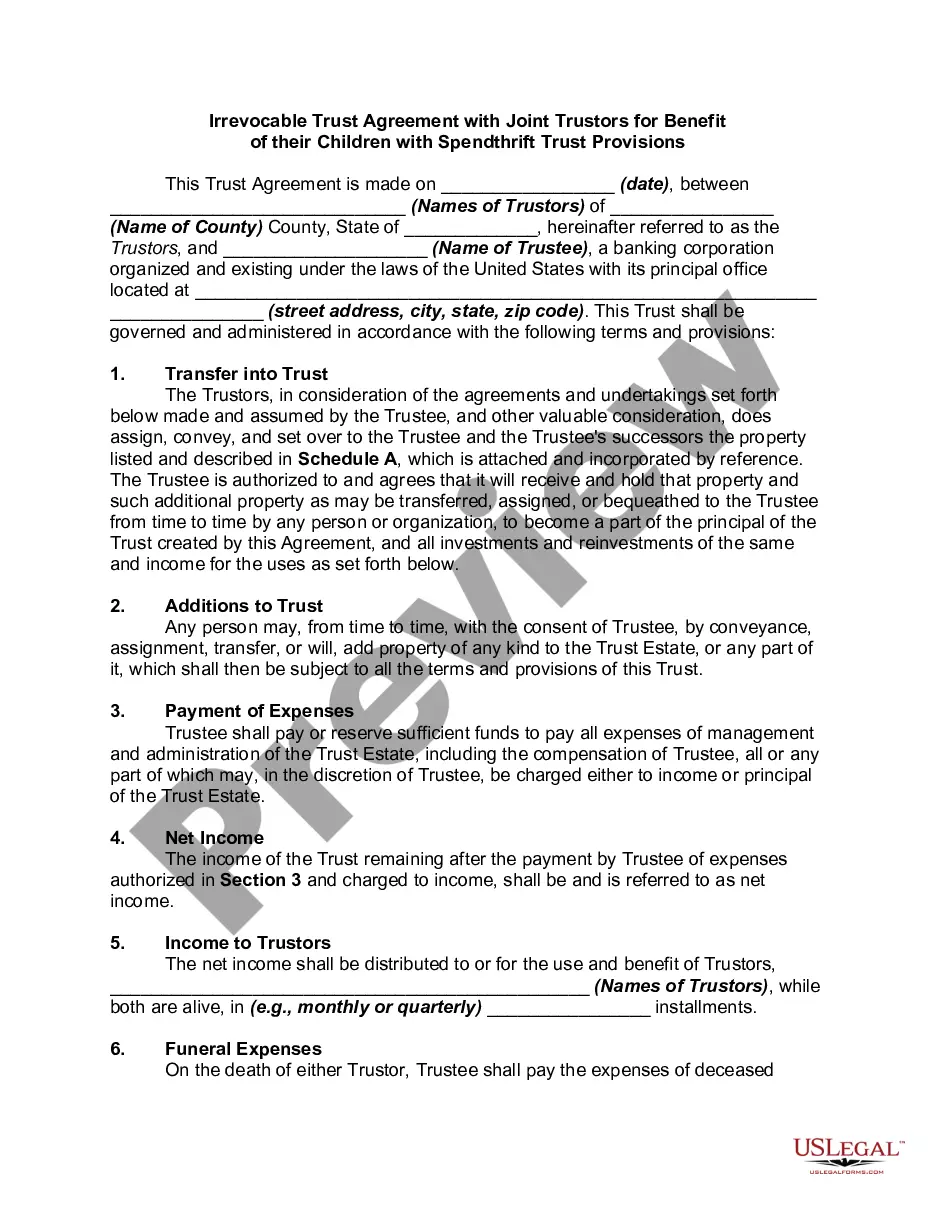

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Mississippi Irrevocable Trust Agreement for the Benefit of Spouse, Children and Grandchildren

Instant download

Description

Free preview

How to fill out Irrevocable Trust Agreement For The Benefit Of Spouse, Children And Grandchildren?

Selecting the correct legitimate document format can be challenging. Naturally, there are numerous templates accessible online, but how do you find the valid form you require? Use the US Legal Forms platform. The service offers thousands of templates, including the Mississippi Irrevocable Trust Agreement for the Benefit of Spouse, Children, and Grandchildren, which can be utilized for both business and personal purposes. All forms are reviewed by professionals and comply with state and federal regulations.

If you are already registered, Log In to your account and click on the Acquire button to obtain the Mississippi Irrevocable Trust Agreement for the Benefit of Spouse, Children, and Grandchildren. Use your account to browse through the legitimate forms you have acquired previously. Visit the My documents section of your account to obtain another copy of the document you require.

If you are a new user of US Legal Forms, here are simple steps you should follow: First, ensure you have selected the correct form for your city/state. You can view the form using the Preview button and read the form details to make sure it is suitable for you. If the form does not meet your requirements, use the Search field to find the appropriate form. Once you are confident that the form is right, click the Purchase now button to acquire the form. Choose the payment option you prefer and enter the necessary information. Create your account and pay for the order using your PayPal account or credit card. Select the file format and download the legitimate document design to your device. Complete, modify, and print and sign the received Mississippi Irrevocable Trust Agreement for the Benefit of Spouse, Children, and Grandchildren.

- Selecting the right valid document design can be tough.

- There are many templates online, but how do you find the genuine form you need.

- Utilize the US Legal Forms site to access a plethora of templates.

- Choose the pricing plan and input the required details for payment.

- US Legal Forms is the most comprehensive library of legal documents available.

Form popularity

FAQ

Trusts can have more than one beneficiary and they commonly do. In cases of multiple beneficiaries, the beneficiaries may hold concurrent interests or successive interests.

What are the Disadvantages of a Trust?Costs. When a decedent passes with only a will in place, the decedent's estate is subject to probate.Record Keeping. It is essential to maintain detailed records of property transferred into and out of a trust.No Protection from Creditors.

When one of the spouses dies, the trust will then split into two trusts automatically. Each trust will have half the assets of the trust along with the separate property of the spouse.

Disadvantages of a Family Trust You must prepare and submit legal documents, which the court charges a fee to process. The second financial disadvantage of a family trust is the lack of tax benefits, especially when it comes to filing income taxes. When the grantor dies, the trust must file a federal tax return.

An irrevocable trust is a trust that can't be amended or modified. However, like any other trust an irrevocable trust can have multiple beneficiaries. The Internal Revenue Service allows irrevocable trusts to be created as grantor, simple or complex trusts.

One of the most preferred ways to leave assets to grandchildren is by naming them as a beneficiary in your will or trust. As the grantor or trustor, you are able to specify a set amount of money or a percentage of your total accounts and property to each grandchild as you see fit.

Irrevocable trusts can also protect assets from being used in determining Medicare eligibility. Once an irrevocable trust is funded, the trust property cannot be taken back by the grantor without the consent of the beneficiary. It is legal to name a beneficiary as trustee, such as a spouse.

Income earned by the trust from amounts that you've deposited will not be taxed to you; the trust pays the taxes. Amounts deposited in trust, and the income earned from those funds, will be used for the benefit of your grandchildren. You can provide that the trust terminate at any age you specify.

While there's no limit to how many trustees one trust can have, it might be beneficial to keep the number low. Here are a few reasons why: Potential disagreements among trustees. The more trustees you name, the greater the chance they'll have different ideas about how your trust should be managed.

Individual trusts for each grandchild. Most grandparents choose to put equal amounts of money into each grandchild's individual trust. The trustee can then decide when and how much money to distribute to each grandchild from their individual trust based on the standards written into the trust.