Missouri The FACTA Red Flags Rule: A Primer

Description

How to fill out The FACTA Red Flags Rule: A Primer?

It is possible to devote several hours on-line searching for the authorized record design that meets the state and federal needs you need. US Legal Forms provides 1000s of authorized varieties that are evaluated by professionals. You can easily down load or printing the Missouri The FACTA Red Flags Rule: A Primer from the services.

If you have a US Legal Forms accounts, you can log in and then click the Obtain switch. Following that, you can total, revise, printing, or indication the Missouri The FACTA Red Flags Rule: A Primer. Every authorized record design you buy is your own for a long time. To acquire an additional backup of the acquired develop, go to the My Forms tab and then click the corresponding switch.

If you are using the US Legal Forms internet site for the first time, stick to the simple directions below:

- First, make certain you have selected the proper record design to the county/city of your choice. Look at the develop explanation to ensure you have chosen the correct develop. If accessible, use the Review switch to look from the record design as well.

- If you want to discover an additional model of your develop, use the Look for area to discover the design that meets your needs and needs.

- Once you have located the design you would like, click Get now to proceed.

- Select the prices prepare you would like, type your qualifications, and register for your account on US Legal Forms.

- Comprehensive the purchase. You can use your credit card or PayPal accounts to purchase the authorized develop.

- Select the file format of your record and down load it for your gadget.

- Make adjustments for your record if needed. It is possible to total, revise and indication and printing Missouri The FACTA Red Flags Rule: A Primer.

Obtain and printing 1000s of record themes while using US Legal Forms website, that provides the greatest selection of authorized varieties. Use skilled and status-distinct themes to tackle your company or person needs.

Form popularity

FAQ

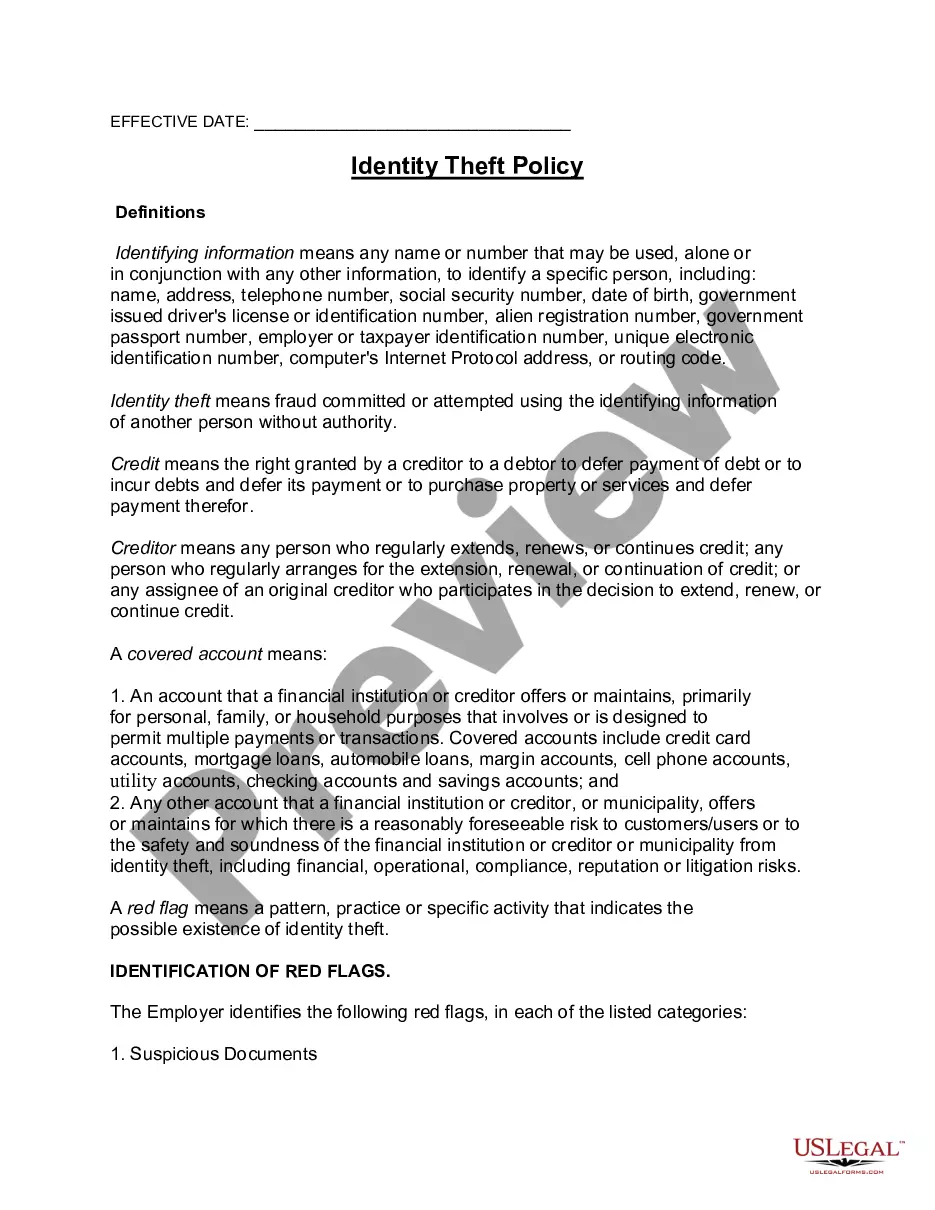

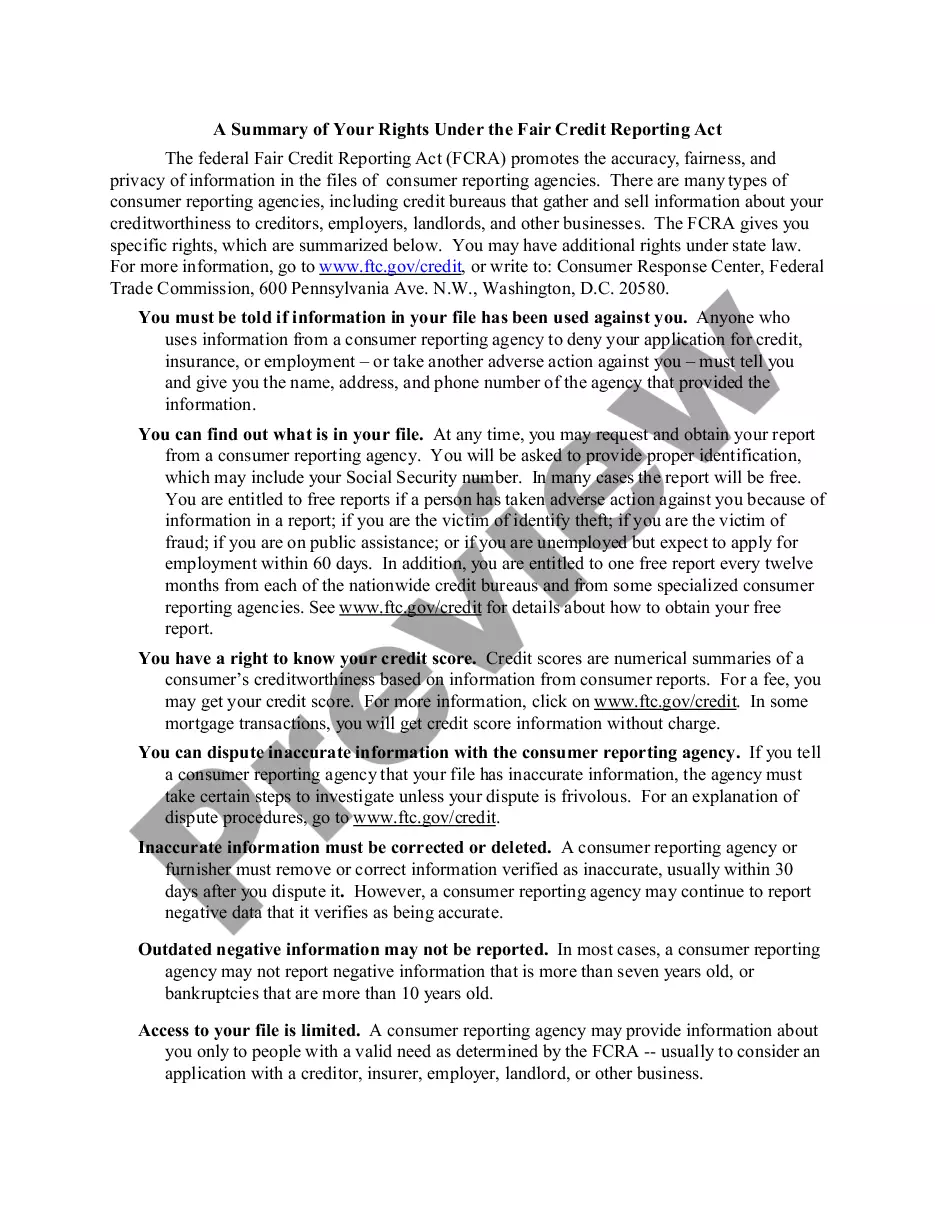

The Red Flags Rule requires that each "financial institution" or "creditor"?which includes most securities firms?implement a written program to detect, prevent and mitigate identity theft in connection with the opening or maintenance of "covered accounts." These include consumer accounts that permit multiple payments ...

The Red Flags Rule requires that each "financial institution" or "creditor"?which includes most securities firms?implement a written program to detect, prevent and mitigate identity theft in connection with the opening or maintenance of "covered accounts." These include consumer accounts that permit multiple payments ...

Banks, credit unions, brokers, mutual funds, financial institutions, and similar businesses are generally covered by the rule and must have identity theft prevention programs in place.

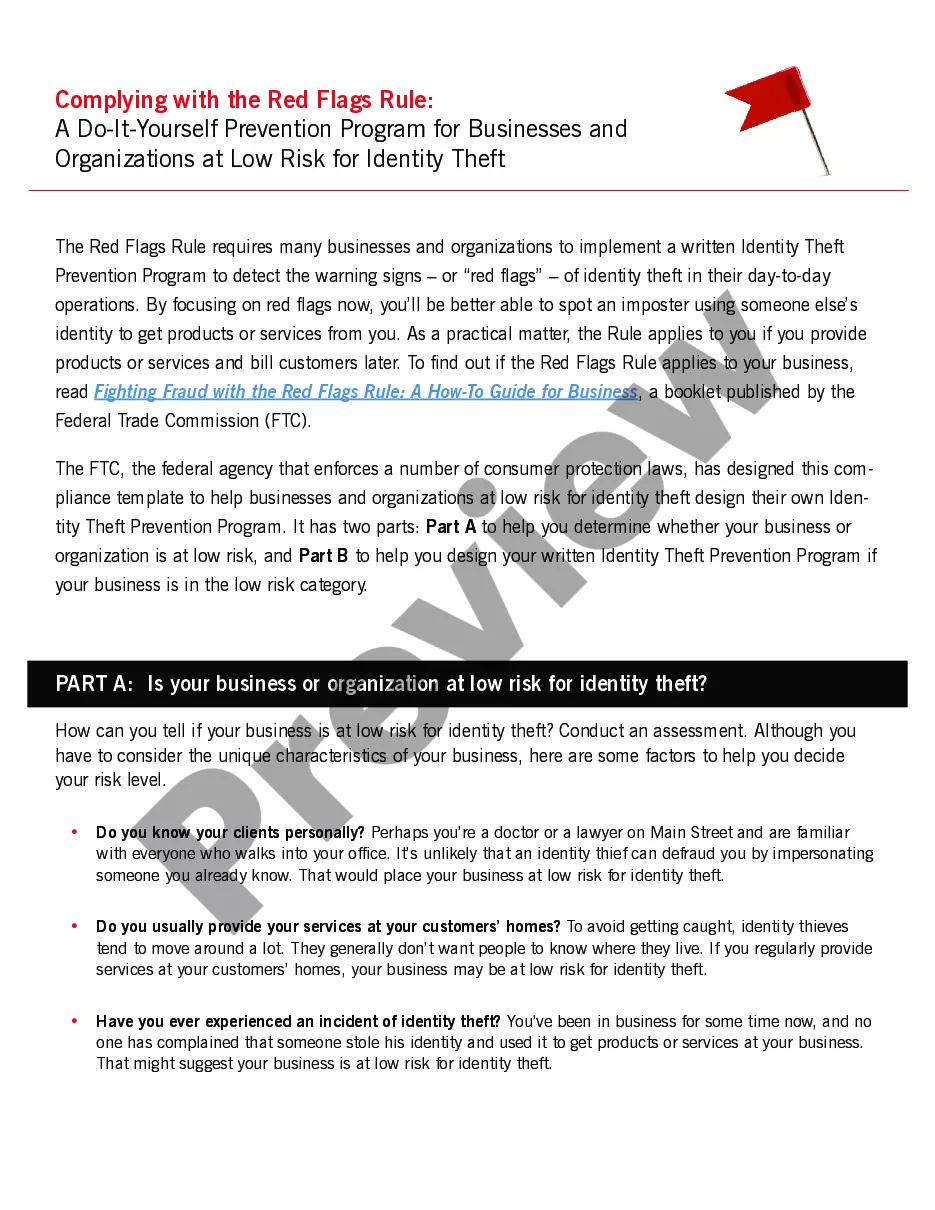

The Red Flags Rule requires organizations to implement a written identity theft prevention program to help them identify any of the relevant ?red flags? that indicate identity theft in daily operations. The Rule also offers steps to help prevent the crime and to mitigate its damage.

In Anti-Money Laundering (AML) compliance, a red flag describes a warning sign that indicates the possibility of money laundering or other criminal activity. Red flags can include transactions involving companies in sanctioned jurisdictions, large volumes, or funds being transmitted from unknown or opaque sources.

The Red Flags Rule requires specified firms to create a written Identity Theft Prevention Program (ITPP) designed to identify, detect and respond to ?red flags??patterns, practices or specific activities?that could indicate identity theft.

The Federal Trade Commission (FTC) has issued regulations (the Red Flags Rules) requiring institutions having covered accounts to develop and implement written identity theft prevention programs, as part of the Fair and Accurate Credit Transactions (FACT) Act of 2003.

Red Flags Rule | Federal Trade Commission.