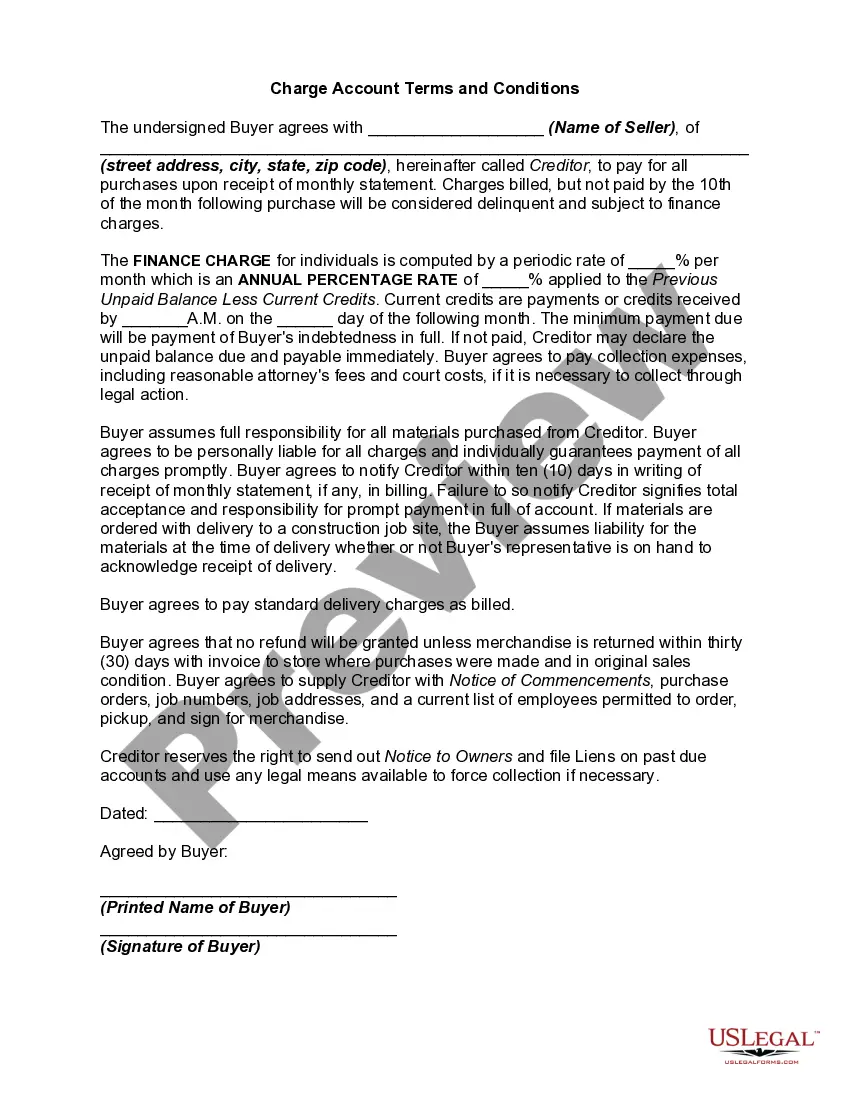

Missouri Retail Charge Account Agreement Initial Disclosure Statement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Retail Charge Account Agreement Initial Disclosure Statement?

Choosing the right authorized papers web template can be quite a struggle. Obviously, there are a variety of web templates available online, but how would you obtain the authorized form you need? Utilize the US Legal Forms web site. The services gives 1000s of web templates, for example the Missouri Retail Charge Account Agreement Initial Disclosure Statement, which can be used for business and personal requirements. All the types are inspected by professionals and meet up with state and federal needs.

When you are presently registered, log in to the profile and then click the Down load option to get the Missouri Retail Charge Account Agreement Initial Disclosure Statement. Use your profile to look from the authorized types you possess acquired formerly. Proceed to the My Forms tab of your respective profile and have an additional backup from the papers you need.

When you are a whole new user of US Legal Forms, listed below are simple recommendations for you to follow:

- Very first, ensure you have chosen the proper form for the town/state. It is possible to check out the form making use of the Review option and read the form information to guarantee it will be the best for you.

- In case the form will not meet up with your preferences, take advantage of the Seach area to get the right form.

- When you are certain that the form is acceptable, click on the Buy now option to get the form.

- Select the pricing plan you desire and enter the required information. Make your profile and pay money for the order using your PayPal profile or charge card.

- Opt for the data file formatting and download the authorized papers web template to the product.

- Comprehensive, edit and produce and signal the attained Missouri Retail Charge Account Agreement Initial Disclosure Statement.

US Legal Forms is definitely the largest collection of authorized types that you can discover numerous papers web templates. Utilize the service to download appropriately-made papers that follow state needs.

Form popularity

FAQ

Total of payments, Payment schedule, Prepayment/late payment penalties, If applicable to the transaction: (1) Total sales cost, (2) Demand feature, (3) Security interest, (4) Insurance, (5) Required deposit, and (6) Reference to contract.

The annual percentage rate (APR), finance charges (including application fees, late fees, and prepayment penalties), finance charge information, a payment schedule, and the total repayment amount consumers the loan's lifetime must all be included in the lender's Truth in Lending (TIL) disclosure statement.

Credit card disclosure must include a list of fees associated with your card. Some common credit card fees include annual fees, cash advance fees, foreign transaction fees, often called a "currency conversion" fee. Other fees include late payment fees, over-the-limit fees, and returned payment fees.

TILA disclosures include the number of payments, the monthly payment, late fees, whether a borrower can prepay the loan without penalty and other important terms.

Created to protect people from predatory lending practices, Regulation Z, also known as the Truth in Lending Act, requires that lenders disclose borrowing costs, interest rates and fees upfront and in clear language so consumers can understand all the terms and make informed decisions.

The Truth in Lending Act (and Regulation Z) explains which transactions are exempt from the disclosure requirements, including: loans primarily for business, commercial, agricultural, or organizational purposes. federal student loans.

Regulation Z restricts how rates can be included in advertisements for closed-end credit. The APR must always be listed (and must state that the APR is subject to increase after consummation, if applicable). The interest rate may also be listed but not more conspicuously than the APR.