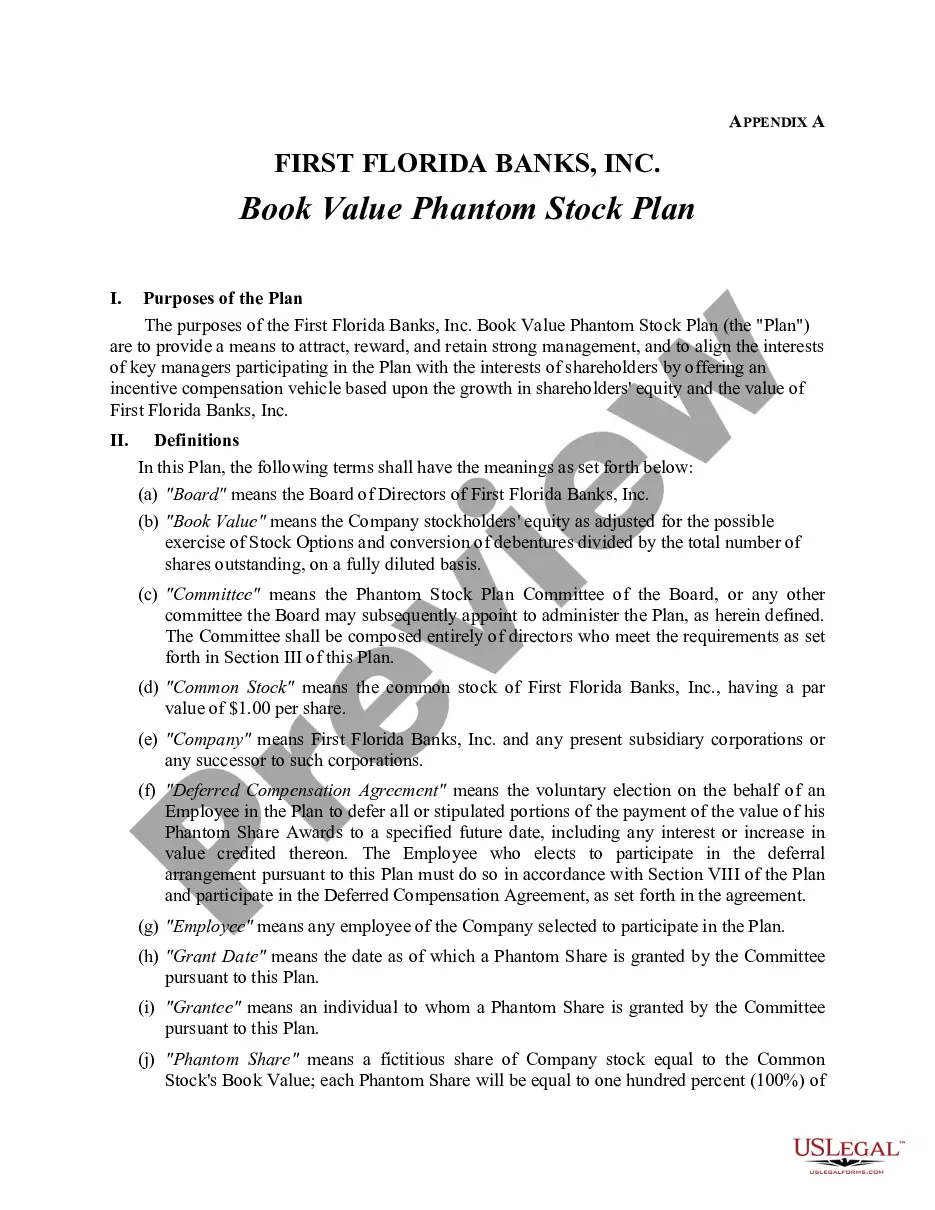

Minnesota Proposed book value phantom stock plan with appendices for First Florida Bank, Inc.

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Proposed Book Value Phantom Stock Plan With Appendices For First Florida Bank, Inc.?

Finding the right authorized record web template can be a have difficulties. Of course, there are plenty of themes available on the Internet, but how can you discover the authorized kind you will need? Utilize the US Legal Forms web site. The support offers thousands of themes, such as the Minnesota Proposed book value phantom stock plan with appendices for First Florida Bank, Inc., which you can use for enterprise and private requires. All the forms are inspected by specialists and meet state and federal demands.

Should you be presently authorized, log in for your bank account and click on the Obtain key to find the Minnesota Proposed book value phantom stock plan with appendices for First Florida Bank, Inc.. Utilize your bank account to check with the authorized forms you have bought earlier. Proceed to the My Forms tab of your respective bank account and have yet another copy of the record you will need.

Should you be a whole new customer of US Legal Forms, here are straightforward recommendations so that you can follow:

- Initially, ensure you have chosen the correct kind to your metropolis/county. You may look over the form while using Review key and look at the form description to guarantee it is the best for you.

- When the kind fails to meet your needs, take advantage of the Seach area to find the appropriate kind.

- Once you are positive that the form would work, select the Acquire now key to find the kind.

- Choose the pricing strategy you would like and enter in the essential info. Make your bank account and pay money for an order utilizing your PayPal bank account or charge card.

- Choose the submit format and down load the authorized record web template for your product.

- Comprehensive, edit and printing and indicator the attained Minnesota Proposed book value phantom stock plan with appendices for First Florida Bank, Inc..

US Legal Forms will be the largest library of authorized forms for which you can see a variety of record themes. Utilize the company to down load professionally-made files that follow express demands.

Form popularity

FAQ

If a business is sold, employees that own phantom stock receive money that is equal to the amount they would have received had they owned actual stock in the company. For that reason, it's financially beneficial to employees to own phantom stock, as they don't need to worry about dilution.

Phantom stock plans are considered ?liability awards? for accounting purposes (assuming they will be settled in cash rather than stock). As such, the sponsoring company must recognize the plan expense ratably over the vesting period. Varying accrual schedules can be found in the market.

For example, suppose an employee received 10 phantom shares with a starting value of $7, and assume the shares are valued on the payment date at $15. At the date of payment the employee would receive $150 under a ?full value? plan and $80 under an ?appreciation only? plan.

The answer involves two variables: (a) the presumed value of the company, and (b) the number of shares to be used in the plan. Once these two answers are known, the phantom share price is calculated as the former (the value) divided by the latter (the number of shares).

It is possible to create a phantom stock plan that avoids the application of 409A rules. The key requirement would be to (a) use cliff vesting (any incremental vesting must trigger immediate payment), and (b) pay benefits within 2½ months of the end of the year in which the awards vest.

A cash payment from Company A as the difference between the current common share price and phantom stock issue price: ($70 ? $50) x 500 = $10,000; or. A cash payment from Company A equal to the current common share price: $50 x 500 = $25,000.

As a default, this form plan provides for forfeiture of all unvested phantom stock units upon a participant's termination of employment (subject to the terms of the award agreement).

Phantom stock plans are considered ?liability awards? for accounting purposes (assuming they will be settled in cash rather than stock).