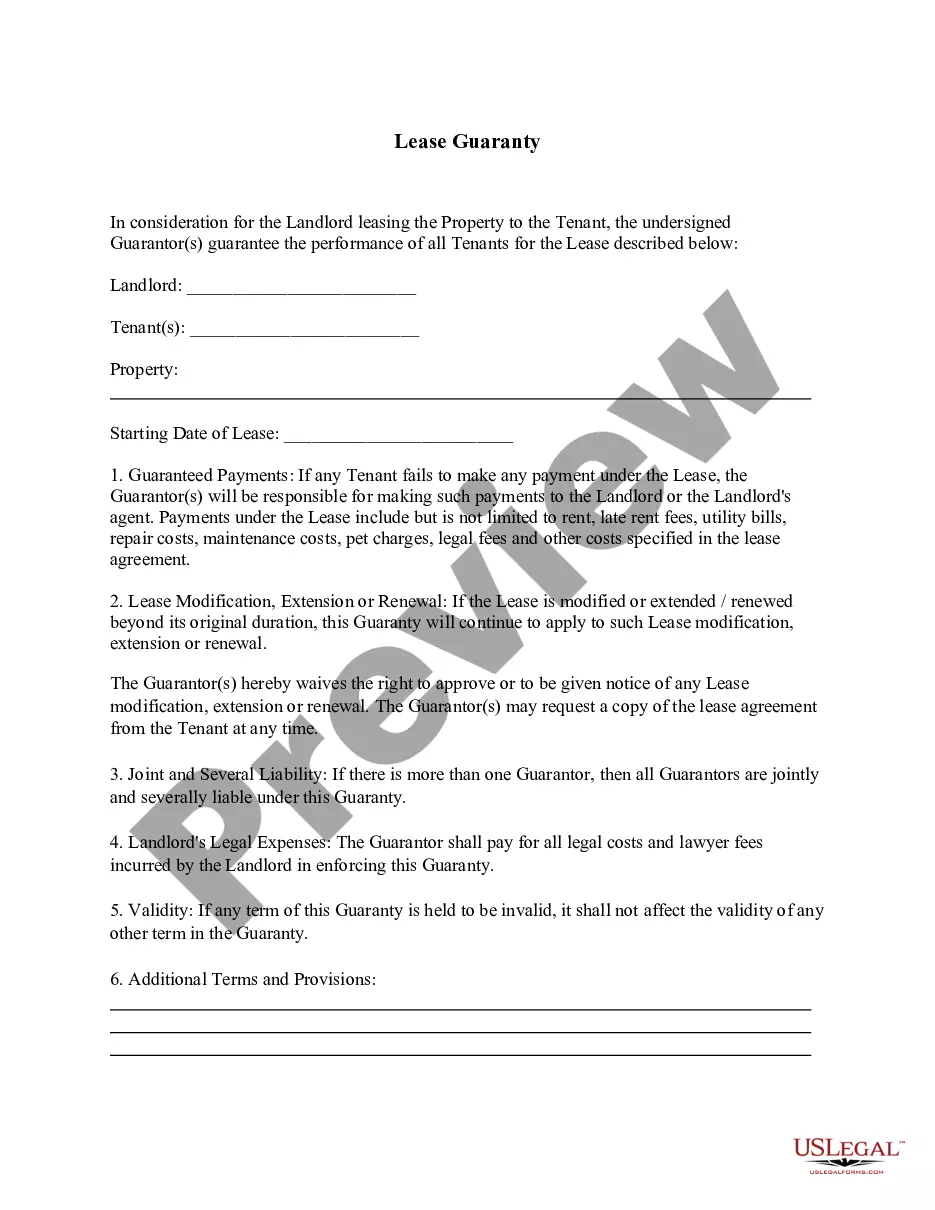

Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate

Description

How to fill out Personal Guaranty - Guarantee Of Contract For The Lease And Purchase Of Real Estate?

Selecting the most suitable authorized document template can be challenging. It goes without saying that there are numerous web templates accessible online, but how do you find the authorized form you need.

Utilize the US Legal Forms website. The service offers thousands of templates, such as the Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate, that you can use for both business and personal purposes.

All the forms are reviewed by experts and comply with federal and state regulations.

US Legal Forms is indeed the largest repository of authorized forms where you can access a variety of document templates. Use this service to obtain professionally crafted paperwork that conforms to state requirements.

- If you are already registered, Log In to your account and click the Obtain button to access the Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate.

- Use your account to search through the authorized forms you have purchased previously.

- Visit the My documents tab in your account to download another copy of the document you need.

- If you are a new user of US Legal Forms, here are straightforward instructions to follow.

- First, ensure you have selected the correct form for your jurisdiction.

- You can review the form using the Review option and check the form description to confirm it is the appropriate one for your needs.

- If the form does not meet your requirements, utilize the Search feature to find the correct form.

- Once you are confident that the form is suitable, click the Buy now option to purchase the form.

- Select the payment plan you desire and enter the necessary details.

- Create your account and pay for the order using your PayPal account or credit card.

- Choose the file format and download the authorized document template to your device.

- Complete, modify, print, and sign the obtained Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate.

Form popularity

FAQ

A guarantee agreement for a mortgage provides a safety net for lenders. It assures them that if the borrower defaults, the guarantor will cover the missed payments. In the context of a Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate, this agreement is particularly important for securing real estate transactions. By using a platform like uslegalforms, you can easily draft a personalized agreement tailored to your specific needs.

Whether a personal guarantee needs to be notarized can vary by state and specific contractual requirements. In many cases, having it notarized adds a layer of validity and protection. For peace of mind regarding a Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate, checking local laws or using a service like USLegalForms can provide clarity on this requirement.

Filling out a personal guarantee involves entering your contact details, the amount being guaranteed, and any terms related to the agreement. It’s essential to communicate openly with the parties involved, ensuring clarity in obligations under the Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate. Double-check for any specific requirements the form may have, and consider using USLegalForms for guidance.

A personal guarantor agreement is a document where an individual agrees to take responsibility for another party’s debt or obligation. This agreement is essential in various financial transactions, particularly in real estate. In a Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate, it helps landlords or lenders secure their investments.

To fill out a personal guaranty, first, provide your personal details, including your name, address, and relationship to the entity involved. Then, outline the specific obligations you are accepting under the Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate. Make sure to read the document thoroughly before signing to understand your responsibilities.

A personal guarantee form is a legal document that an individual signs to confirm they will be personally responsible for paying a debt or fulfilling an obligation if the primary entity fails to do so. In the context of a Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate, this form ensures that personal assets can be claimed if a lease or purchase agreement is not honored. It is crucial for protecting the interests of landlords and lenders.

An example of a personal guarantee is when a parent agrees to be a guarantor for their child's apartment lease. In the Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate, this scenario often occurs when young adults lack a solid credit history. The parent’s commitment provides reassurance to the landlord that rent will be covered, promoting smoother leasing arrangements.

A personal guarantee agreement is similar to a personal guaranty agreement, in that it involves an individual agreeing to assume responsibility for another's debts. It specifically outlines the obligations the guarantor will cover in case of default. For individuals engaging with Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate, understanding this concept is vital for securing rental or property purchase arrangements.

The purpose of a guaranty agreement is to provide additional security for a lease or purchase contract. In the Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate, the guaranty reassures landlords and sellers that they will receive payment even if the primary party fails to meet their obligations. This added layer of assurance can facilitate smoother negotiations and transactions.

A personal guaranty agreement is a contract in which an individual agrees to take personal responsibility for another party's debt or obligations. Specifically, in the context of Minnesota Personal Guaranty - Guarantee of Contract for the Lease and Purchase of Real Estate, this agreement ensures that if the tenant or buyer defaults, the guarantor will fulfill the financial obligations. This type of agreement often helps landlords or sellers mitigate risk.