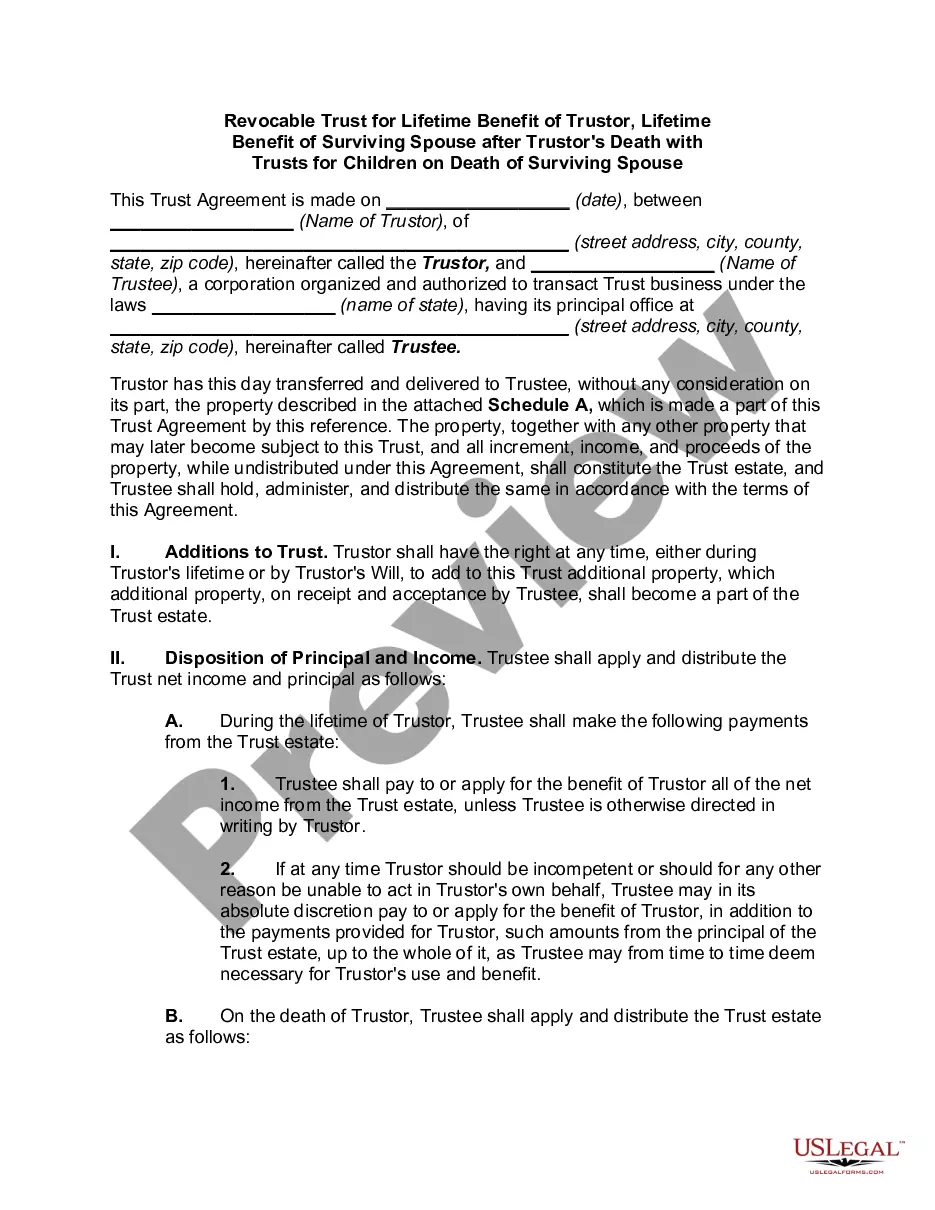

Minnesota Marital-deduction Residuary Trust with a Single Trustor and Lifetime Income and Power of Appointment in Beneficiary Spouse

Description

How to fill out Marital-deduction Residuary Trust With A Single Trustor And Lifetime Income And Power Of Appointment In Beneficiary Spouse?

Discovering the right authorized record template might be a have a problem. Naturally, there are tons of themes accessible on the Internet, but how can you discover the authorized form you want? Utilize the US Legal Forms site. The service delivers a huge number of themes, such as the Minnesota Marital-deduction Residuary Trust with a Single Trustor and Lifetime Income and Power of Appointment in Beneficiary Spouse, which you can use for enterprise and personal requirements. All the types are inspected by professionals and satisfy state and federal demands.

In case you are already listed, log in to the accounts and click the Down load button to have the Minnesota Marital-deduction Residuary Trust with a Single Trustor and Lifetime Income and Power of Appointment in Beneficiary Spouse. Make use of your accounts to search with the authorized types you might have bought in the past. Go to the My Forms tab of your respective accounts and get an additional backup from the record you want.

In case you are a new user of US Legal Forms, allow me to share basic directions so that you can comply with:

- Initially, make certain you have chosen the appropriate form for your area/region. It is possible to examine the shape making use of the Review button and study the shape information to make sure it is the right one for you.

- When the form does not satisfy your needs, take advantage of the Seach industry to obtain the proper form.

- When you are sure that the shape is acceptable, click on the Get now button to have the form.

- Opt for the pricing program you need and enter in the needed info. Build your accounts and buy the transaction with your PayPal accounts or charge card.

- Pick the file format and down load the authorized record template to the product.

- Total, change and print and indication the acquired Minnesota Marital-deduction Residuary Trust with a Single Trustor and Lifetime Income and Power of Appointment in Beneficiary Spouse.

US Legal Forms is the greatest catalogue of authorized types that you can discover various record themes. Utilize the company to down load skillfully-created paperwork that comply with condition demands.

Form popularity

FAQ

The grantor can opt to have the beneficiaries receive trust property directly without any restrictions. The trustee can write the beneficiary a check, give them cash, and transfer real estate by drawing up a new deed or selling the house and giving them the proceeds.

Beneficiaries of a trust typically pay taxes on distributions they receive from the trust's income. However, they are not subject to taxes on distributions from the trust's principal.

The marital deduction is determinable from the overall gross estate. The total value of the assets passed on to the spouse is subtracted from that amount, giving us the marital deduction. This interspousal transfer can occur during the couple's lifetime or after one spouse's death, ing to a will.

The trustee can transfer real estate to the beneficiary by having a new deed written up or selling the property and giving them the money, writing them a check or giving them cash.

The fiduciary must be under a duty to distribute the income currently even if, as a matter of practical necessity, the income is not distributed until after the close of the trust's taxable year.

The first trust (the ?marital? trust) is for the surviving spouse, and the second trust (the ?bypass? or ?residual? trust) is typically for the couple's heirs. The surviving spouse can access the residual trust or receive income from it during their lifetime, but it does not belong to them.

Outright Trust Distributions They consist of the trustee releasing each beneficiary's inheritance without any restrictions. Outright distributions can either be made as a single lump sum, or periodically. Prior to making outright trust distributions, the trustee will need to pay the trust's debts and taxes.

An example of when a marital trust might be used is when a couple has children from a previous marriage and wants to pass all property to the surviving spouse upon death, but also provide for their individual children.