Maine 4.26.7203 Failure to File a Tax Return, 26 U.S.C. Sec. 7203, is a criminal offense under the United States federal law. The offense is defined as the willful failure to file a tax return required by law within the required time frame. This offense is punishable by a fine or imprisonment for up to one year. There are two types of Maine 4.26.7203 Failure to File a Tax Return, 26 U.S.C. Sec. 7203: 1. Willful Failure to File: This offense occurs when a taxpayer willfully fails to file a tax return or other required document within the required time frame. This offense is punishable by a fine or imprisonment for up to one year. 2. Negligent Failure to File: This offense occurs when a taxpayer negligently fails to file a tax return or other required document within the required time frame. This offense is punishable by a fine or imprisonment for up to six months.

Maine 4.26.7203 Failure to File a Tax Return, 26 U.S.C. Sec. 7203

Description

How to fill out Maine 4.26.7203 Failure To File A Tax Return, 26 U.S.C. Sec. 7203?

If you’re seeking a method to effectively prepare the Maine 4.26.7203 Failure to File a Tax Return, 26 U.S.C. Sec. 7203 without engaging a legal expert, then you’re in the perfect place.

US Legal Forms has demonstrated itself as the most comprehensive and trustworthy collection of official templates for all personal and business circumstances. Every document you locate on our online platform is created in accordance with federal and state regulations, ensuring that your paperwork is accurate.

Another significant benefit of US Legal Forms is that you never lose the documents you acquired - you can access any of your downloaded forms in the My documents tab of your profile whenever you require it.

- Confirm that the document you view on the page aligns with your legal circumstances and state regulations by reviewing its text description or checking the Preview mode.

- Type the form title in the Search tab at the top of the page and choose your state from the list to discover another template in case of any discrepancies.

- Repeat the content verification and click Buy now when you are assured of the paperwork's compliance with all necessary requirements.

- Log in to your account and click Download. If you don’t have one yet, sign up for the service and select the subscription plan.

- Use your credit card or the PayPal option to purchase your US Legal Forms subscription. The blank will be ready for download immediately afterward.

- Select the format in which you wish to save your Maine 4.26.7203 Failure to File a Tax Return, 26 U.S.C. Sec. 7203 and download it by clicking the appropriate button.

- Add your template to an online editor to complete and sign it quickly or print it out to prepare your hard copy manually.

Form popularity

FAQ

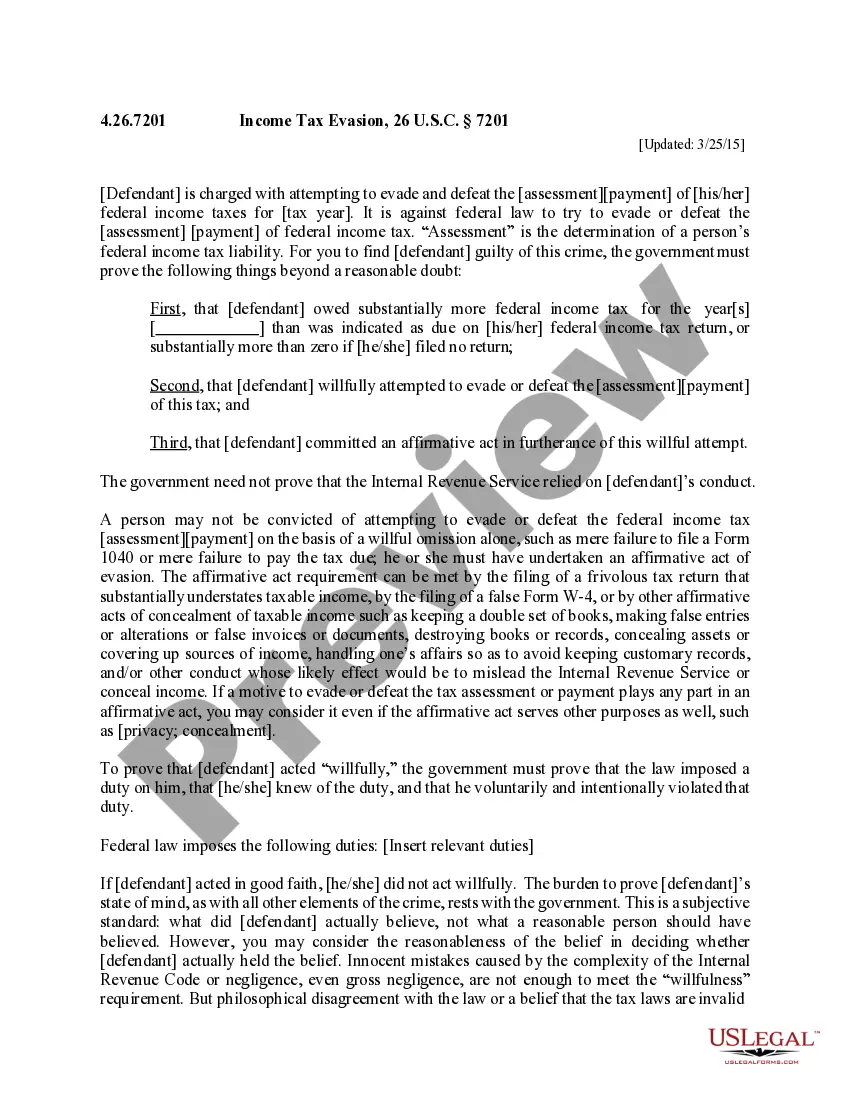

7203 the willful failure to file a return, supply information, or pay tax at the time or times required by law, are felonies and carry a penalty of imprisonment for up to 3 years, a $250,000 fine for individuals or a $500,000 fine for corporations, or both, and reimbursement to the federal government to cover the costs

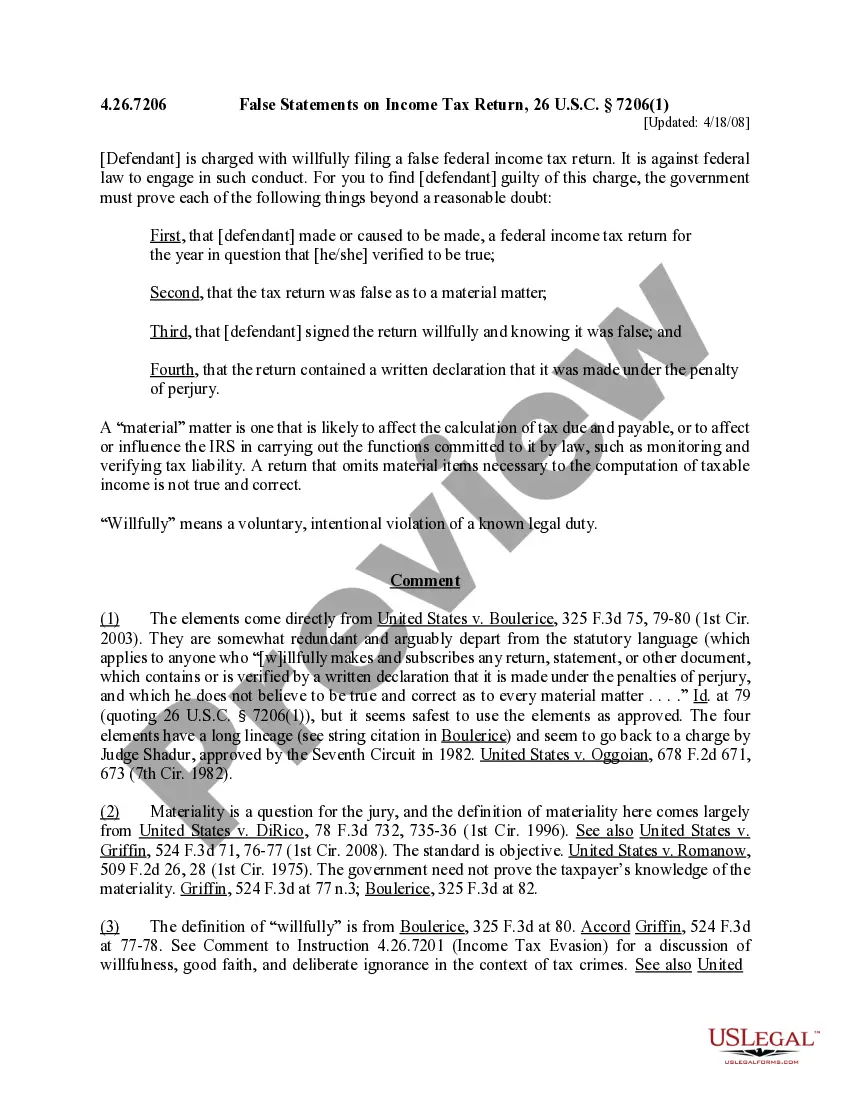

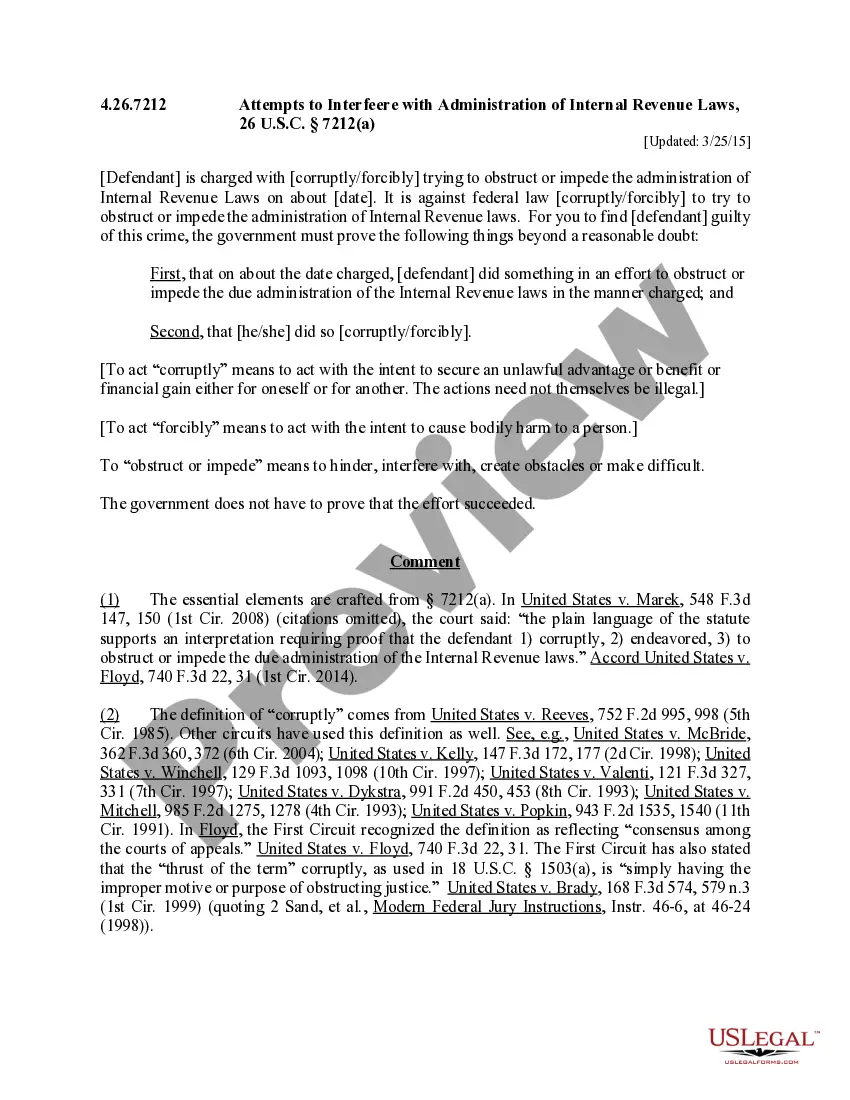

Willful failure to file a tax return is a misdemeanor pursuant to IRC 7203. In cases where an overt act of evasion occurred, willful failure to file may be elevated to a felony under IRC 7201. If you are charged with a criminal tax violation, the punishment can be severe and may include fines and jail time.

Section 7203 makes illegal four entirely different acts of failure to timely complete a requirement of the IRS: (1) failure to pay an estimated tax or tax, (2) failure to make (file) a return, (3) failure to keep records, and (4) failure to supply information.

Failure to file penalty The penalty is $25,000 for each year you failed to file. You can face criminal tax evasion charges for failing to file a tax return if it was due no more than six years ago. If convicted, you could be sent to jail for up to one year.

Tax evasion is an illegal activity in which a person or entity deliberately avoids paying a true tax liability. Those caught evading taxes are generally subject to criminal charges and substantial penalties. To willfully fail to pay taxes is a federal offense under the Internal Revenue Service (IRS) tax code.

Most Common Charge under 7203 is Failure to File a Return The charge most often brought under Section 7203 is the failure to make (file) a return. A number of cases are also brought under Section 7203 for failure to pay a tax. Note that the attempt to evade or defeat the payment of a tax is a felony under Section 7201.

Section 7203 makes illegal four entirely different acts of failure to timely complete a requirement of the IRS: (1) failure to pay an estimated tax or tax, (2) failure to make (file) a return, (3) failure to keep records, and (4) failure to supply information.