Maryland Construction Loan Financing Term Sheet

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Construction Loan Financing Term Sheet?

US Legal Forms - one of many most significant libraries of legal kinds in the USA - delivers an array of legal record themes you may download or printing. Making use of the site, you can get a huge number of kinds for company and specific uses, sorted by classes, suggests, or keywords and phrases.You can get the newest versions of kinds just like the Maryland Construction Loan Financing Term Sheet within minutes.

If you already have a membership, log in and download Maryland Construction Loan Financing Term Sheet from your US Legal Forms collection. The Down load option will appear on every kind you look at. You get access to all earlier acquired kinds within the My Forms tab of your own accounts.

If you wish to use US Legal Forms the first time, listed here are basic directions to help you get started out:

- Be sure you have picked the best kind for the metropolis/region. Click on the Preview option to check the form`s information. See the kind description to ensure that you have selected the appropriate kind.

- If the kind doesn`t match your needs, utilize the Lookup discipline towards the top of the screen to get the the one that does.

- When you are happy with the form, affirm your option by clicking on the Purchase now option. Then, select the prices program you like and supply your credentials to register for the accounts.

- Method the financial transaction. Make use of your Visa or Mastercard or PayPal accounts to accomplish the financial transaction.

- Choose the structure and download the form on the device.

- Make adjustments. Fill up, modify and printing and signal the acquired Maryland Construction Loan Financing Term Sheet.

Each format you added to your bank account lacks an expiry particular date and is your own eternally. So, if you want to download or printing one more copy, just go to the My Forms section and click on about the kind you need.

Gain access to the Maryland Construction Loan Financing Term Sheet with US Legal Forms, by far the most extensive collection of legal record themes. Use a huge number of expert and express-certain themes that meet up with your small business or specific requirements and needs.

Form popularity

FAQ

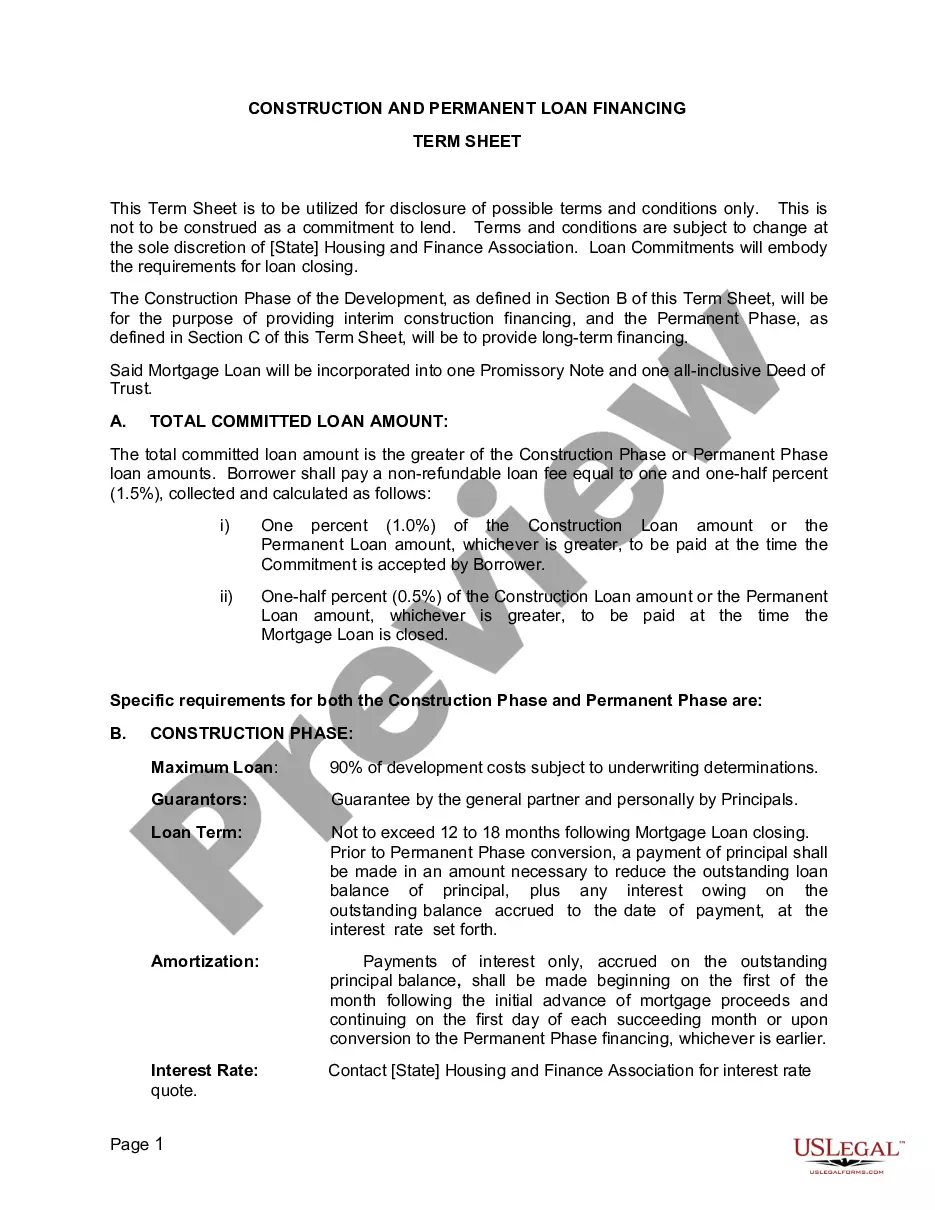

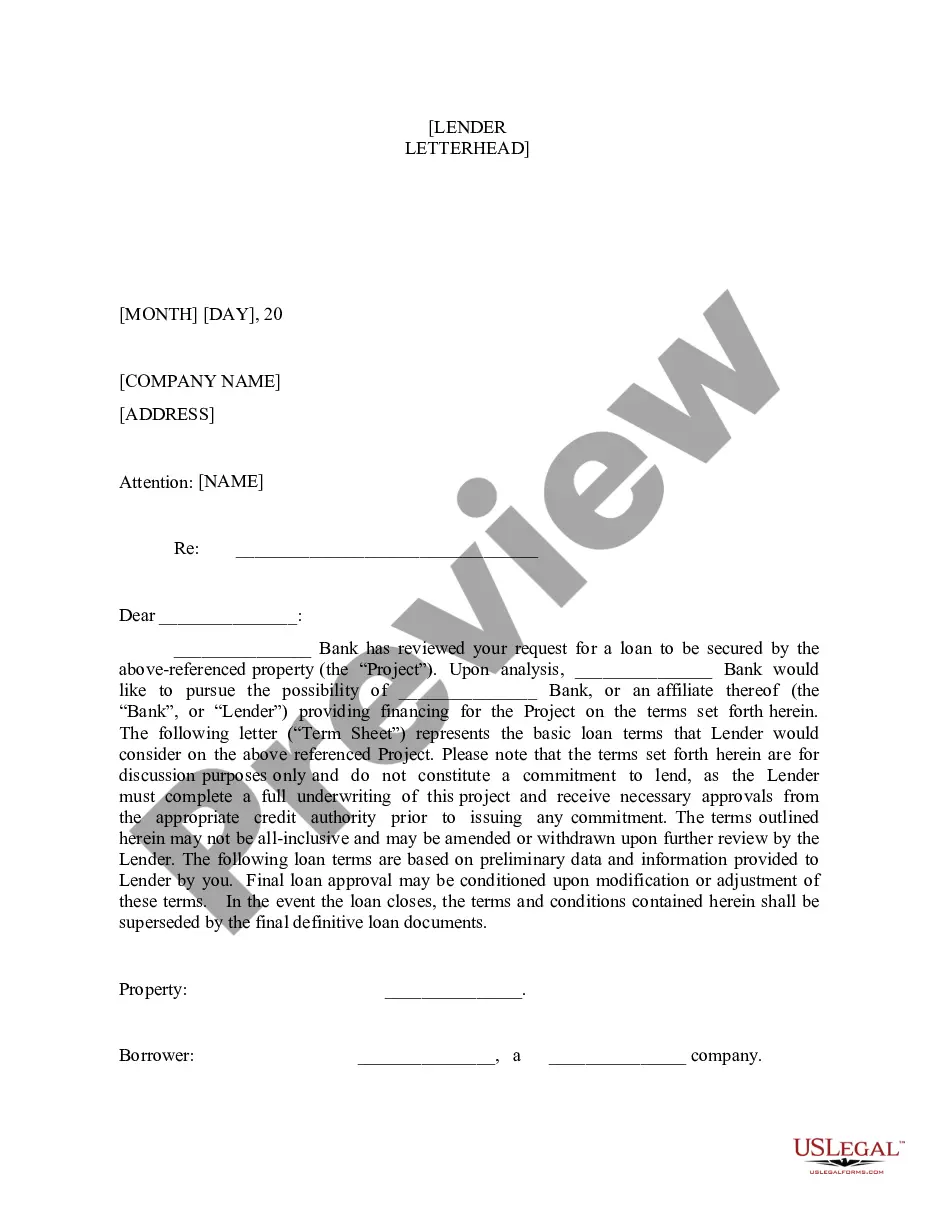

As mentioned, construction loans are short-term loans, usually no longer than a year in length. On the other hand, traditional mortgages are long-term loans, with terms typically ranging from 15 ? 30 years. With a mortgage, the borrower receives the money in one lump sum.

In a project finance transaction, a set of conditions a project company must satisfy once the project has achieved substantial completion or final completion to convert a construction loan to a term loan. Failure to satisfy these conditions may result in the immediate repayment of the construction loan.

With a construction loan, the lender typically agrees to loan a certain percentage (95%, for example) of the future home's appraised value. Then, they'll suggest a down payment equal to the difference between the approved loan amount and the construction costs.

This includes the term, loan size, interest rate, and other financial matters common to debt. Risk mitigation preferences. The lender will often require specific conditions be met or specific information be provided on a recurring, timely manner.

A major feature of a construction loan is that the total approved loan amount is not usually given to the borrower right away, in one lump sum. Instead, the construction loan operates more like a line of credit from which the borrower can access funds as needed at various stages of the construction project.

Here are a few potential outcomes: Personal Financial Responsibility: If you are responsible for covering the additional costs, you may need to contribute additional funds from your own pocket to cover the overage. This can strain your personal finances and potentially disrupt your financial plans.

Construction factoring is an increasingly popular financing option among subcontractors. It improves cash flow and provides a financial platform that can be used to grow the business. Most factoring companies finance your invoices by purchasing them rather than offering a loan.

Construction loans are short-term loans funded in increments over the project's construction. The borrower pays interest only on the outstanding balance, so interest charges grow as the project progresses.