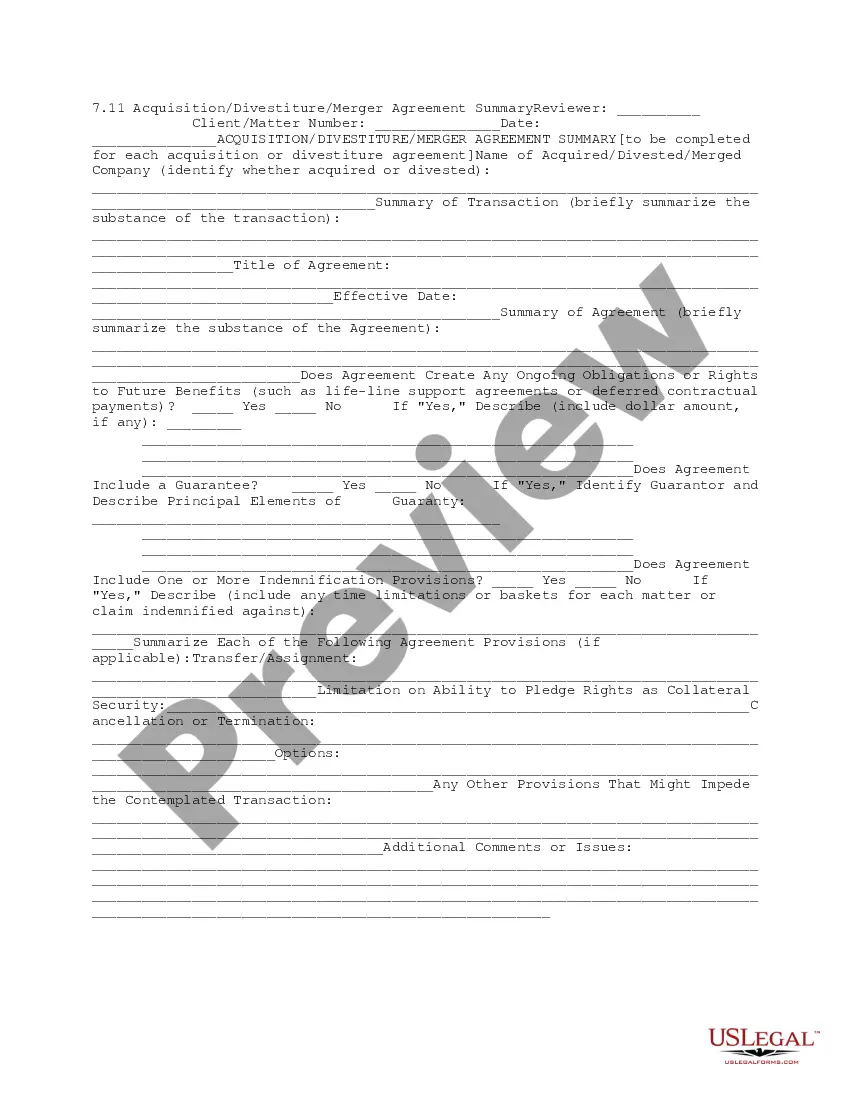

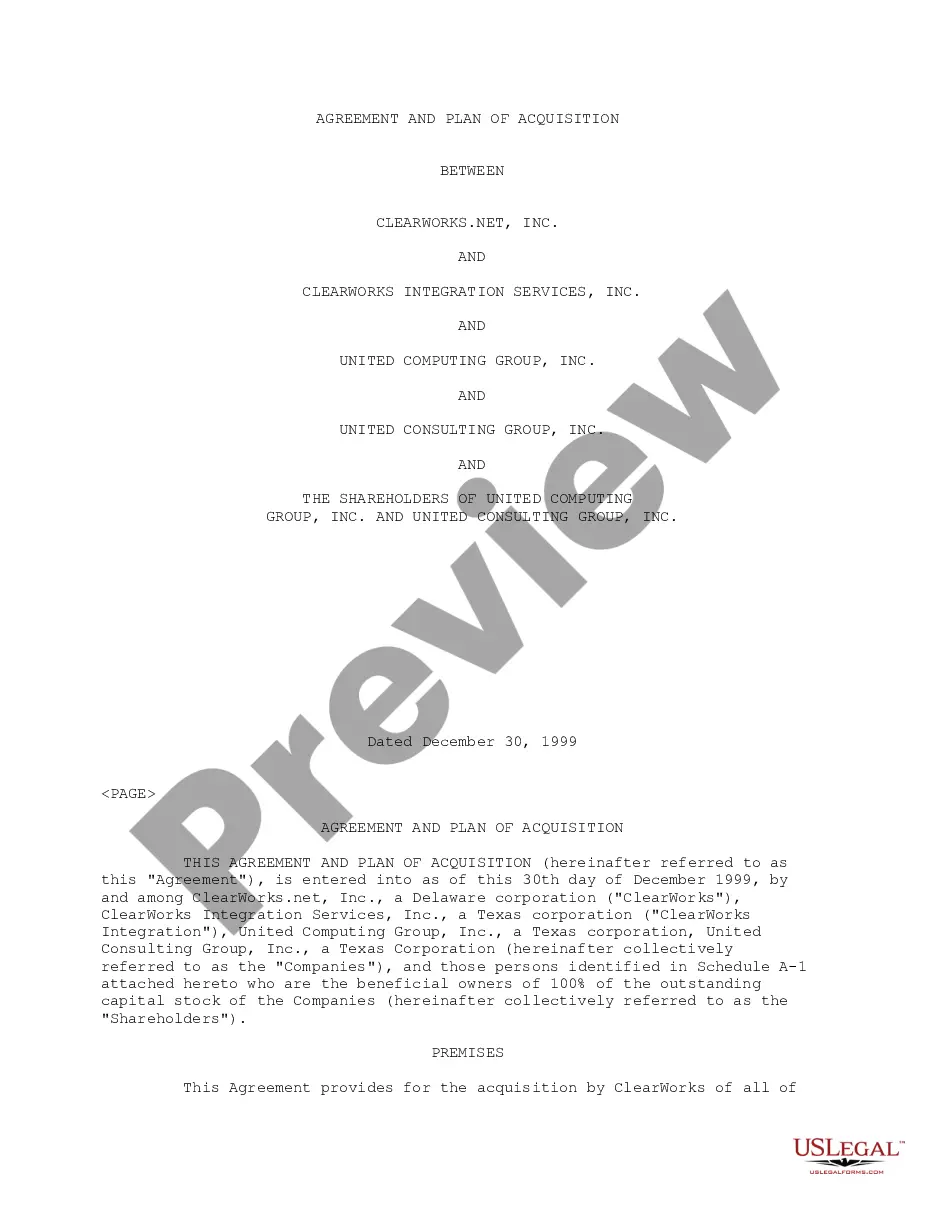

Maryland Acquisition, Merger, or Liquidation

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Acquisition, Merger, Or Liquidation?

US Legal Forms - one of many greatest libraries of lawful types in America - provides a variety of lawful document templates you may down load or printing. Making use of the site, you may get a large number of types for organization and person uses, categorized by groups, states, or search phrases.You will find the newest types of types just like the Maryland Acquisition, Merger, or Liquidation in seconds.

If you currently have a membership, log in and down load Maryland Acquisition, Merger, or Liquidation from the US Legal Forms catalogue. The Download button will appear on every single develop you see. You get access to all previously acquired types from the My Forms tab of your own profile.

If you want to use US Legal Forms the very first time, allow me to share simple recommendations to obtain started off:

- Make sure you have picked the proper develop for your area/region. Click on the Review button to review the form`s articles. Look at the develop description to actually have selected the right develop.

- In case the develop doesn`t fit your demands, take advantage of the Look for industry at the top of the display screen to get the one that does.

- Should you be content with the form, verify your choice by clicking the Buy now button. Then, select the prices plan you prefer and give your accreditations to sign up on an profile.

- Method the financial transaction. Use your credit card or PayPal profile to finish the financial transaction.

- Select the format and down load the form on your own gadget.

- Make changes. Fill out, modify and printing and indicator the acquired Maryland Acquisition, Merger, or Liquidation.

Each web template you added to your bank account lacks an expiry particular date and it is the one you have forever. So, if you wish to down load or printing another copy, just proceed to the My Forms segment and then click on the develop you will need.

Gain access to the Maryland Acquisition, Merger, or Liquidation with US Legal Forms, by far the most substantial catalogue of lawful document templates. Use a large number of skilled and state-specific templates that fulfill your small business or person demands and demands.

Form popularity

FAQ

The acquiring business may experience a taxable gain from the transaction if the tax basis of the assets or shares acquired is lower than the fair market value. This gain is determined by subtracting the asset's or stock's tax base from fair market value. The purchasing firm must pay taxes on this gain.

Mergers and acquisitions can qualify as either taxable or non-taxable. Taxable mergers are mergers where both companies assume tax liability. When two companies merge, they pay taxes on gains from the capital, stock, or assets acquired during the merger.

When a company merges with another company, in some cases the first company needs to pay on acquired assets, so the second company need not to pay any taxes. But if the second company is not dissolved then they must pay tax on their assets. These are the tax consequence faced by the companies in the merger process.

§ 3-105. (6) A business trust party to a merger shall have the merger advised, authorized, and approved in the manner and by the vote required by its declaration of trust and the laws of the place where it is organized.

What should you do? Most organizations that merge into another organization or otherwise terminate will notify the IRS of the changes by filing a final Form 990, Form 990-EZ or the e- Postcard (Form 990-N). Which form your organization uses depends on its gross income and assets.

With a merger ?continuity? can be achieved since assets and liabilities are being transferred to the absorbing ? surviving company. Liquidation brings an end to the existence of the company. The merger requires approval by the Court. The voluntary liquidation does not.

When a business is acquired through a cash purchase, that is a taxable event for the shareholders of the target corporation. A gain or loss must be recognized. However, a stock purchase is generally tax-deferred.

Mergers can be tax free if enough of the payment to the target corporation is in stock rather than cash or property and if substantially all of the assets of the target corporation are acquired. Statutory guidelines are often general, and specific guidelines are often in regulations.