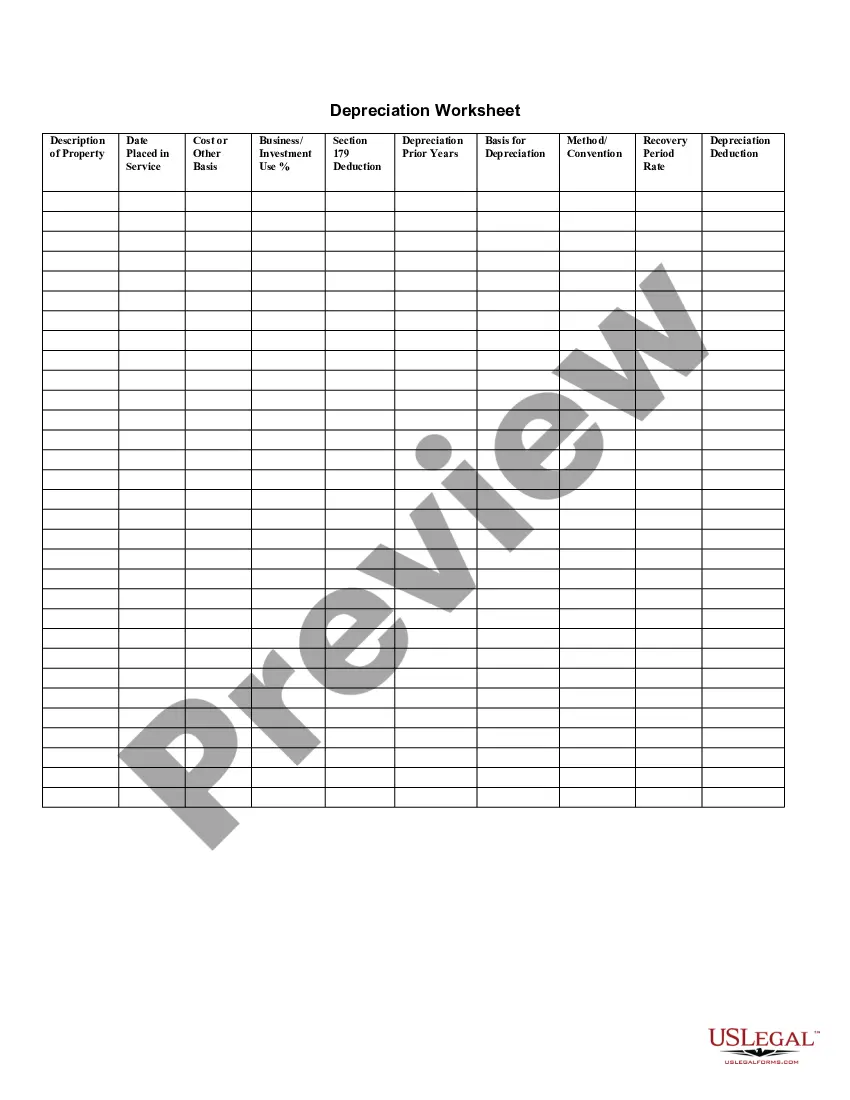

Maryland Depreciation Schedule

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Depreciation Schedule?

If you need to total, obtain, or print authentic legal document templates, utilize US Legal Forms, the foremost collection of legal forms accessible online.

Utilize the site’s user-friendly search feature to find the documents you need.

An array of templates for commercial and personal applications are organized by categories and regions, or keywords. Use US Legal Forms to acquire the Maryland Depreciation Schedule in just a few clicks.

Every legal document template you purchase is yours indefinitely. You have access to every form you acquired in your account. Visit the My documents section and select a form to print or download again.

Stay competitive and obtain and print the Maryland Depreciation Schedule with US Legal Forms. There are thousands of professional and state-specific forms available for your commercial or personal needs.

- If you are already a US Legal Forms user, Log In to your account and click the Download button to access the Maryland Depreciation Schedule.

- You can also access forms you previously acquired from the My documents section of your account.

- If you are utilizing US Legal Forms for the first time, follow the outlined steps below.

- Step 1. Ensure you have selected the form for the correct city/state.

- Step 2. Utilize the Preview option to examine the article of the form. Don’t forget to review the summary.

- Step 3. If you are dissatisfied with the form, use the Search field at the top of the screen to find other variations of the legal document template.

- Step 4. Once you have located the form you require, click the Buy now button. Choose the pricing plan you prefer and input your information to register for an account.

- Step 5. Process the transaction. You can use your Мisa or Ьastercard or PayPal account to complete the payment.

- Step 6. Choose the format of the legal document and download it onto your device.

- Step 7. Complete, modify, and print or sign the Maryland Depreciation Schedule.

Form popularity

FAQ

Because Maryland has legislatively decoupled from federal bonus depreciation, non-manufacturers may not take bonus depreciation on QIP at the Maryland level, even though the property qualifies for federal bonus depreciation.

Maryland requires that Maryland taxable or modified income be computed in accordance with federal income tax laws as if the taxpayer elected not to use the special first year additional depreciation deductions.

For Maryland tax purposes, a taxpayer only is allowed to expense up to $25,000, reduced dollar-for-dollar by the amount over $200,000, of the cost of Section 179 property that is purchased and put in service for a trade or business for the tax year.

The personal property tax bill is calculated by dividing the assessed value, as determined by the State Department of Assessment and Taxation, by $100 and then multiplying by the Cecil County personal property tax rate. Tax rates are set by the County Council each fiscal year.

Under the new TG ? 10-210.1 and 10-310, Maryland has decoupled from both of these JCWAA provisions.

The states that do not conform simply do not allow bonus depreciation and no additional deduction for bonus depreciation is allowed....States that do not conform to the new rules:Arizona.Arkansas.California.Connecticut.District of Columbia.Florida.Georgia.Hawaii.More items...

Maryland has decoupled from certain federal provisions, as listed at the top of Form 500DM, by enacting addition and subtraction modifications which eliminate the effect of the changes on Maryland and local taxes. This form is used to determine the amount of the required modification.

For Maryland tax purposes, a taxpayer only is allowed to expense up to $25,000, reduced dollar-for-dollar by the amount over $200,000, of the cost of Section 179 property that is purchased and put in service for a trade or business for the tax year.

The tax rate is applied to the assessed value of your property. The Maryland State Department of Assessments and Taxation re-evaluates your property once every three years. If the assessed value of your property goes up, then your property tax bill will increase.

Maryland generally conforms to the Internal Revenue Code (IRC) on a rolling conformity basis. In other words, Maryland conforms to amendments to the IRC as they occur. However, Maryland law does require the state's income tax statute to automatically decouple from the IRC under certain circumstances.