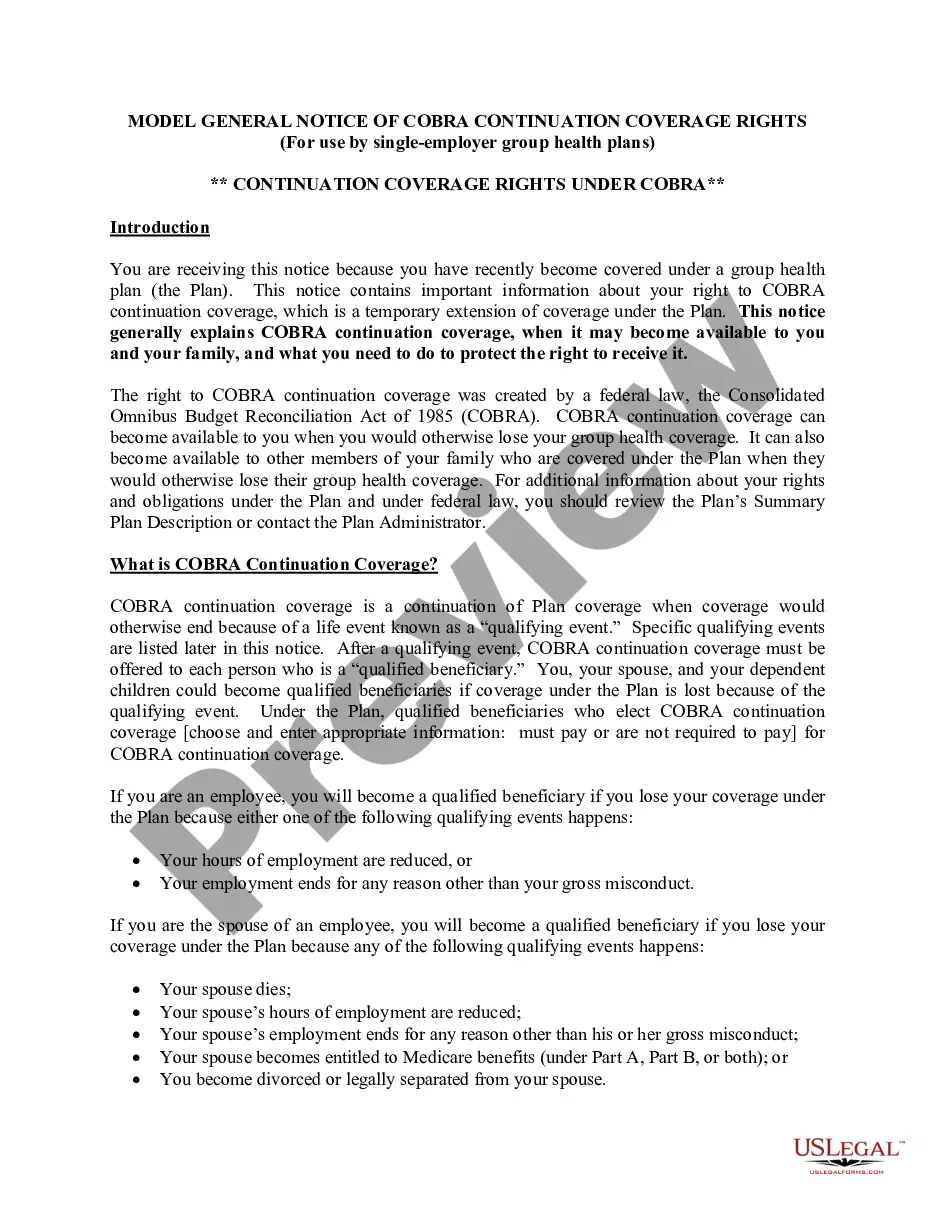

Massachusetts Introductory COBRA Letter

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Introductory COBRA Letter?

US Legal Forms - one of the largest collections of legal documents in the United States - provides an extensive selection of legal form templates that you can purchase or print.

By utilizing the website, you can access thousands of forms for both business and personal use, organized by categories, states, or keywords. You can find the latest versions of forms such as the Massachusetts Introductory COBRA Letter in just a few minutes.

If you already have a subscription, Log In to acquire the Massachusetts Introductory COBRA Letter from the US Legal Forms library. The Download button will appear on each form you view. You have access to all previously saved forms in the My documents section of your account.

Complete the transaction. Use your credit card or PayPal account to finalize the transaction.

Select the format and download the form onto your device. Edit. Fill out, modify, print, and sign the saved Massachusetts Introductory COBRA Letter. Each template you add to your account never expires and is yours indefinitely. Therefore, if you wish to download or print another copy, simply visit the My documents section and click on the form you need.

Access the Massachusetts Introductory COBRA Letter with US Legal Forms, one of the most extensive libraries of legal document templates. Utilize a wide range of professional and state-specific templates that meet your personal or business needs and requirements.

- If you are using US Legal Forms for the first time, here are some straightforward instructions to get you started.

- Ensure you have selected the appropriate form for your city/state.

- Click the Preview button to review the details of the form.

- Examine the form summary to confirm you’ve selected the right form.

- If the form does not meet your needs, use the Search field at the top of the screen to find one that does.

- Once you are satisfied with the form, confirm your choice by clicking the Get now button.

- Then, select the pricing plan you prefer and enter your information to register for an account.

Form popularity

FAQ

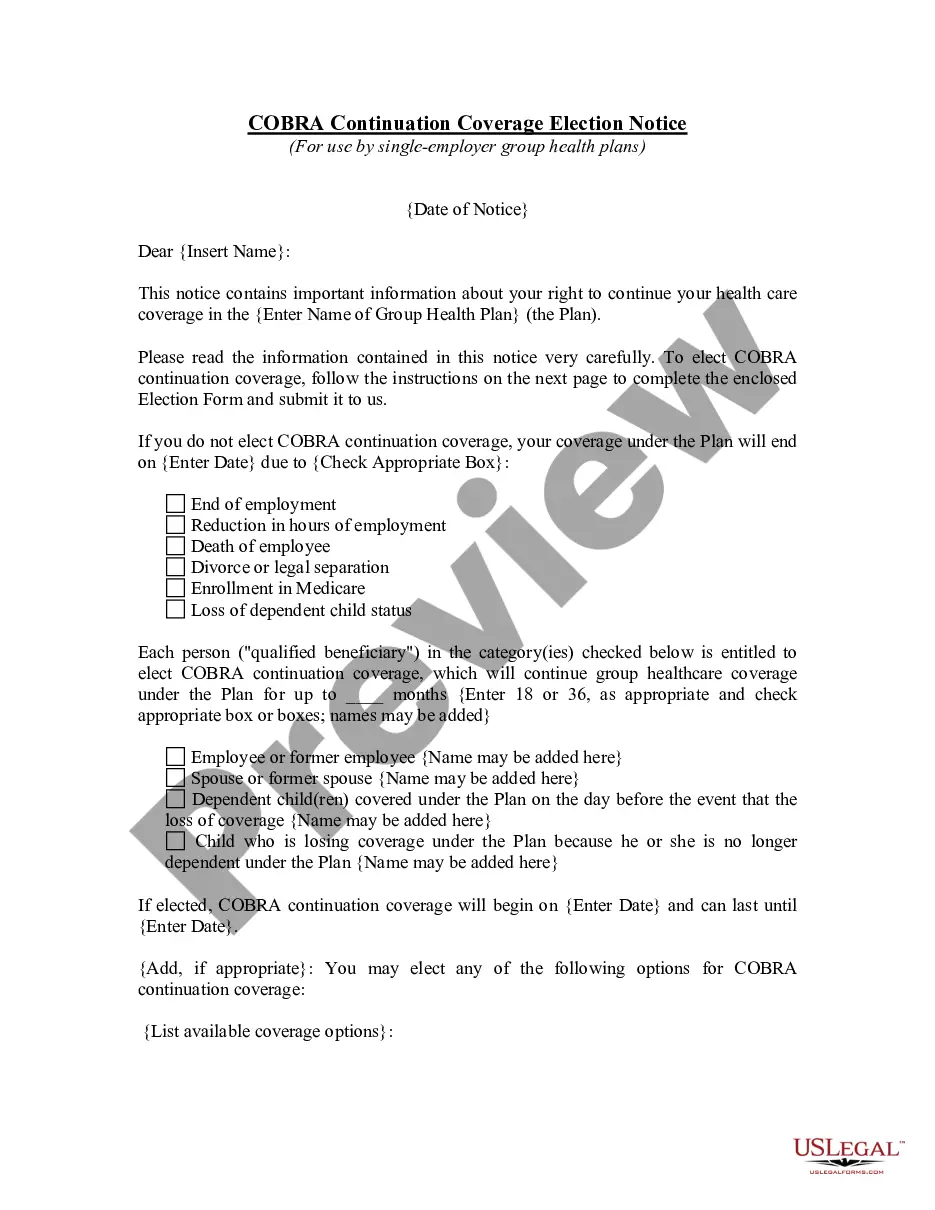

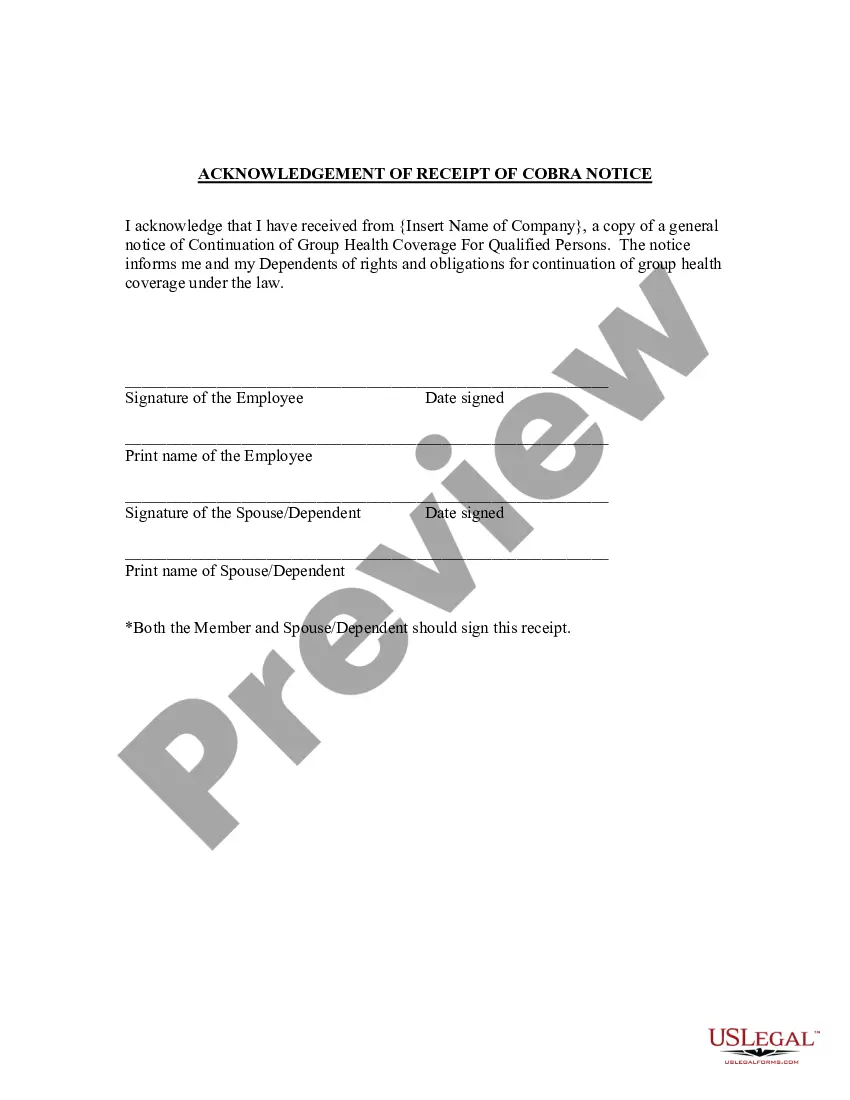

The initial notice, also referred to as the general notice, communicates general COBRA rights and obligations to each covered employee (and his or her spouse) who becomes covered under the group health plan.

When does COBRA continuation coverage startCOBRA is always effective the day after your active coverage ends. For most, active coverage terminates at the end of a month and COBRA is effective on the first day of the next month.

In addition, employers can provide COBRA notices electronically (via email, text message, or through a website) during the Outbreak Period, if they reasonably believe that plan participants and beneficiaries have access to these electronic mediums.

There are several other scenarios that may explain why you received a COBRA continuation notice even if you've been in your current position for a long time: You may be enrolled in a new plan annually and, therefore, receive a notice each year. Your employer may have just begun offering a health insurance plan.

Employers should send notices by first-class mail, obtain a certificate of mailing from the post office, and keep a log of letters sent. Certified mailing should be avoided, as a returned receipt with no delivery acceptance signature proves the participant did not receive the required notice.

COBRA coverage follows a "qualifying event". An example of a qualifying event would be if your hours were reduced or you lost your job (as long as there was no gross misconduct). Your employer must mail you the COBRA information and forms within 14 days after receiving notification of the qualifying event.

If You Do Not Receive Your COBRA PaperworkReach out to the Human Resources Department and ask for the COBRA Administrator. They may use a third-party administrator to handle your enrollment. If the employer still does not comply you can call the Department of Labor at 1-866-487-2365.

Although the earlier rules only covered summary plan descriptions (SPDs) and summary annual reports, the final rules provide that all ERISA-required disclosure documents can be sent electronically -- this includes COBRA notices as well as certificates of creditable coverage under the Health Insurance Portability and

COBRA is a federal law about health insurance. If you lose or leave your job, COBRA lets you keep your existing employer-based coverage for at least the next 18 months. Your existing healthcare plan will now cost you more. Under COBRA, you pay the whole premium including the share your former employer used to pay.

COBRA is a federal law under which certain former employees, retirees, spouses, former spouses and dependent children have the right to temporarily continue their existing group health coverage at group rates when group coverage otherwise would end due to certain life events, called 'Qualifying Events.