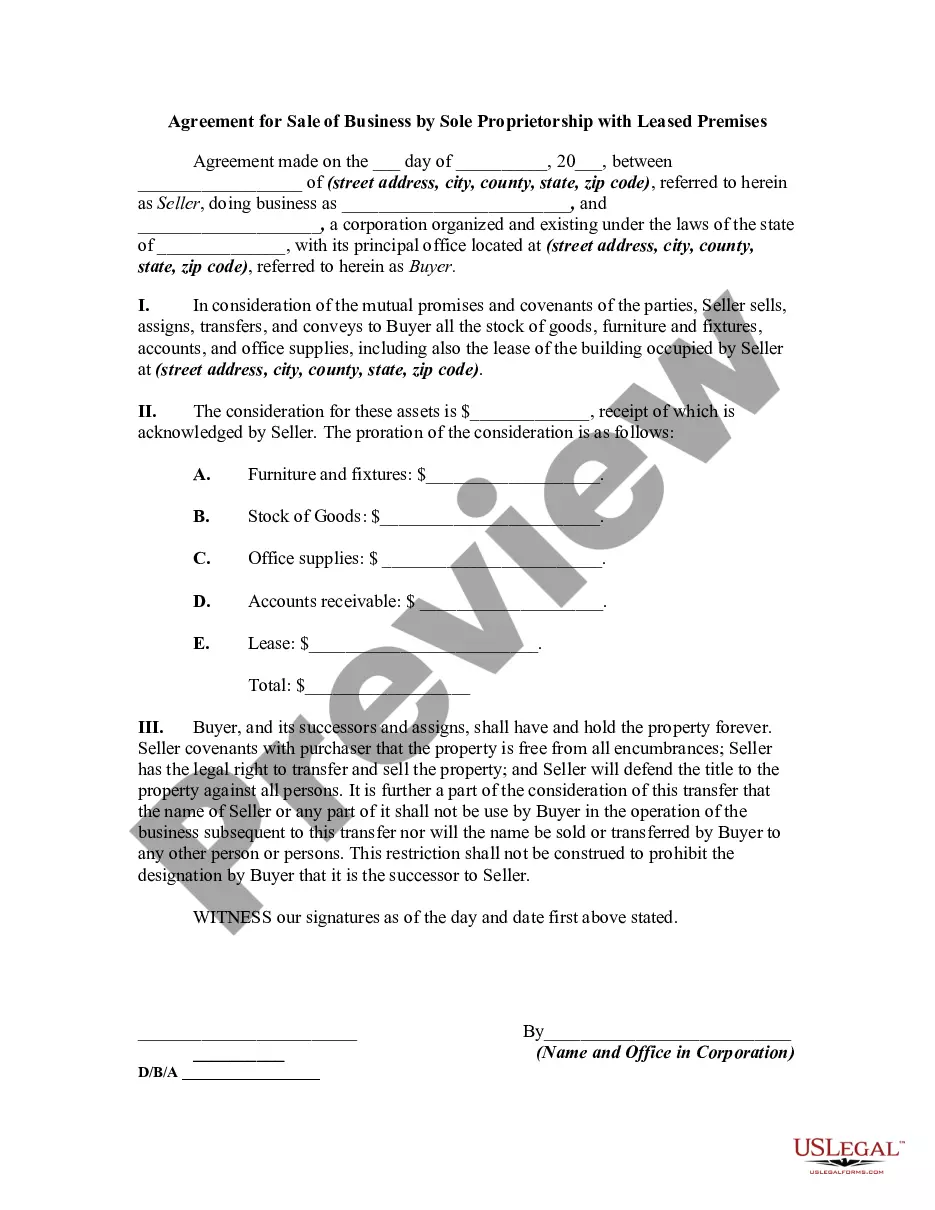

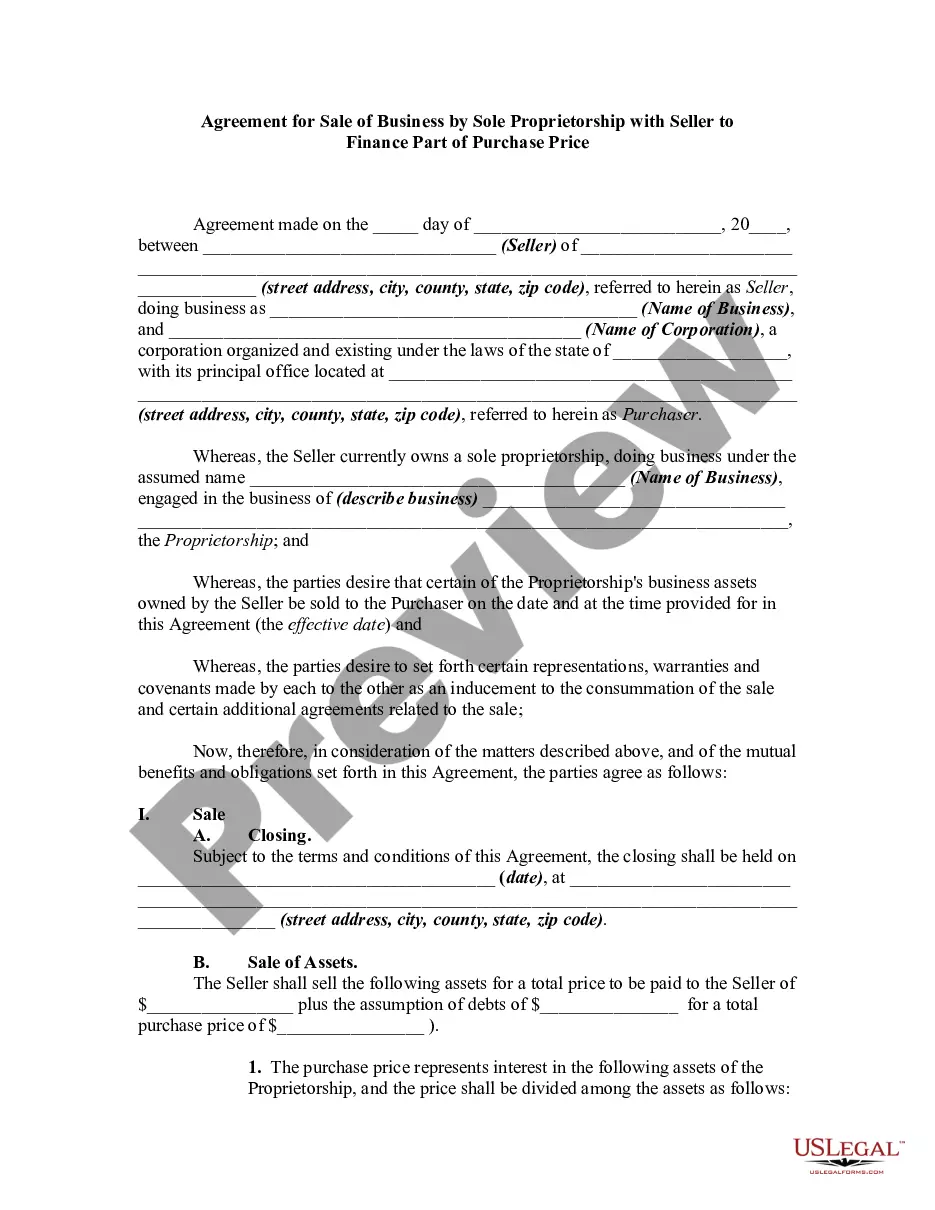

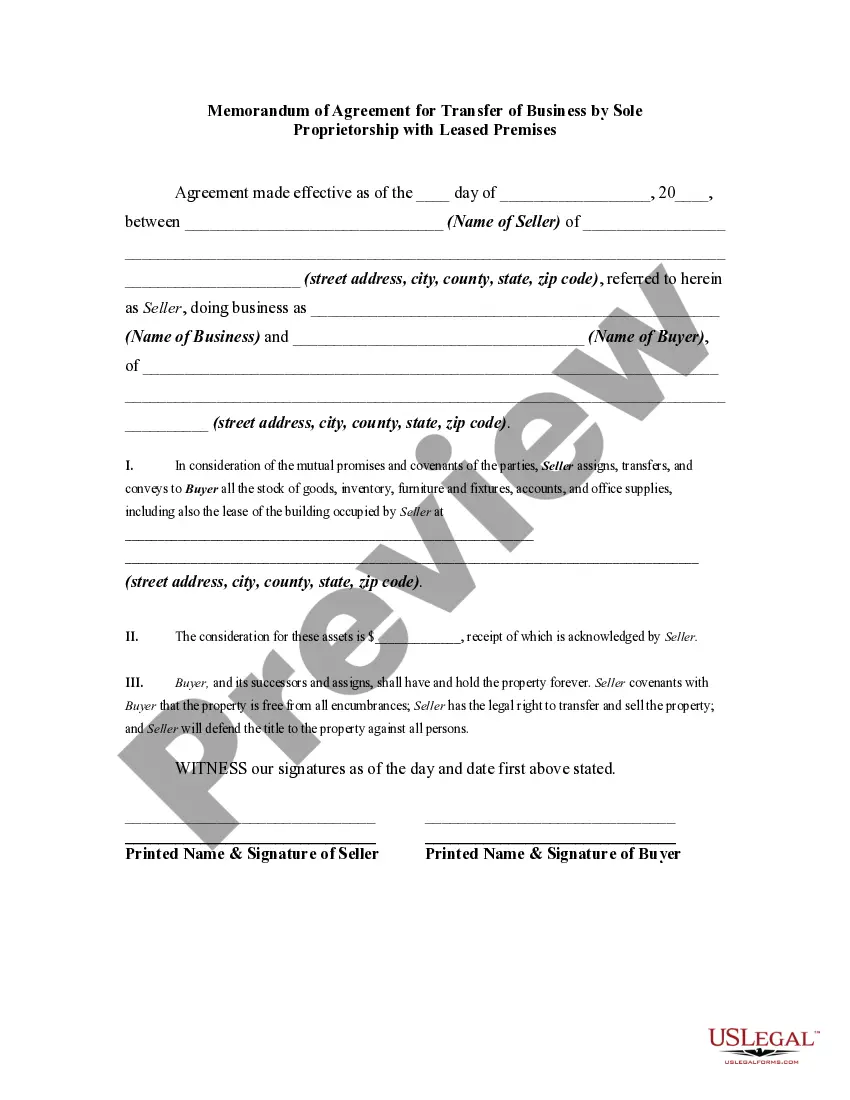

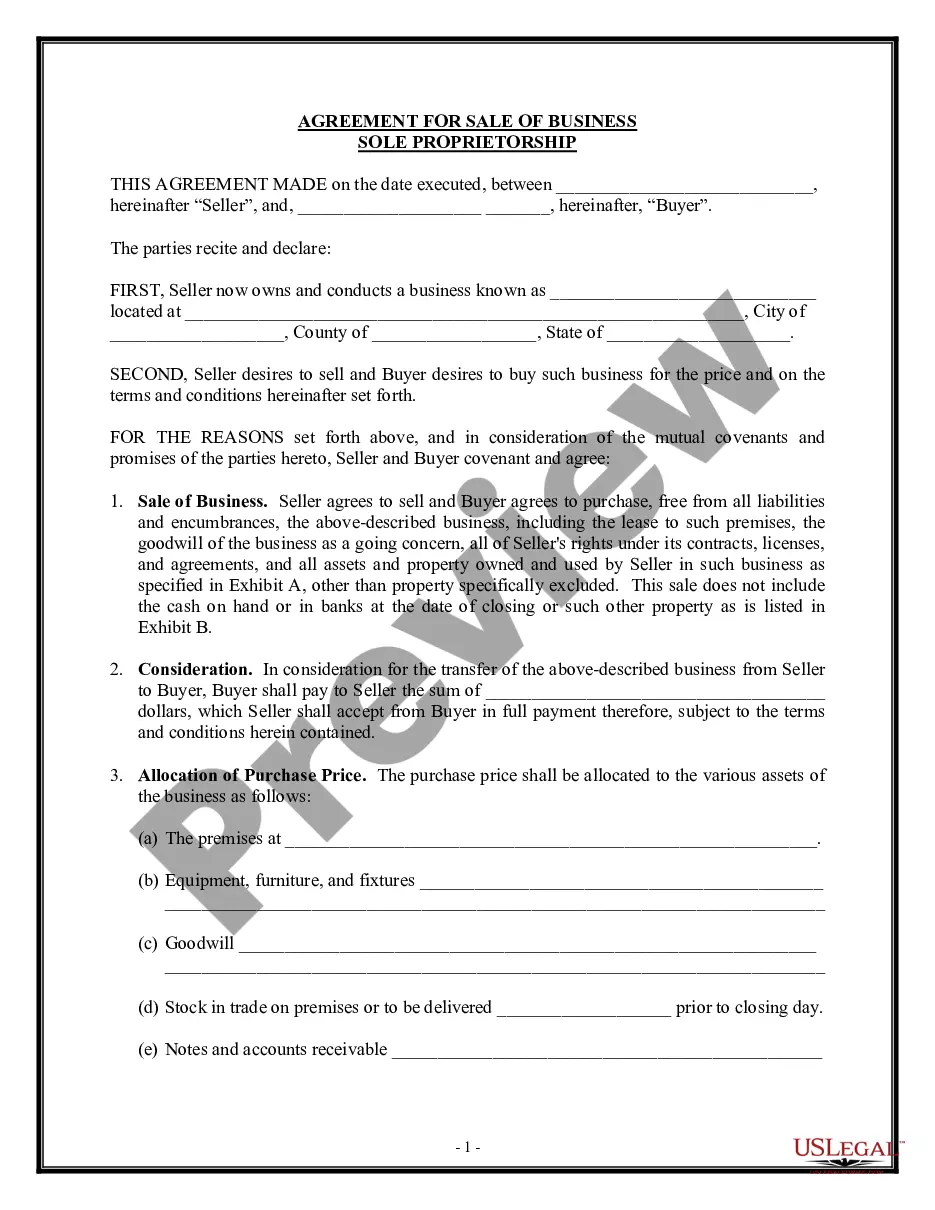

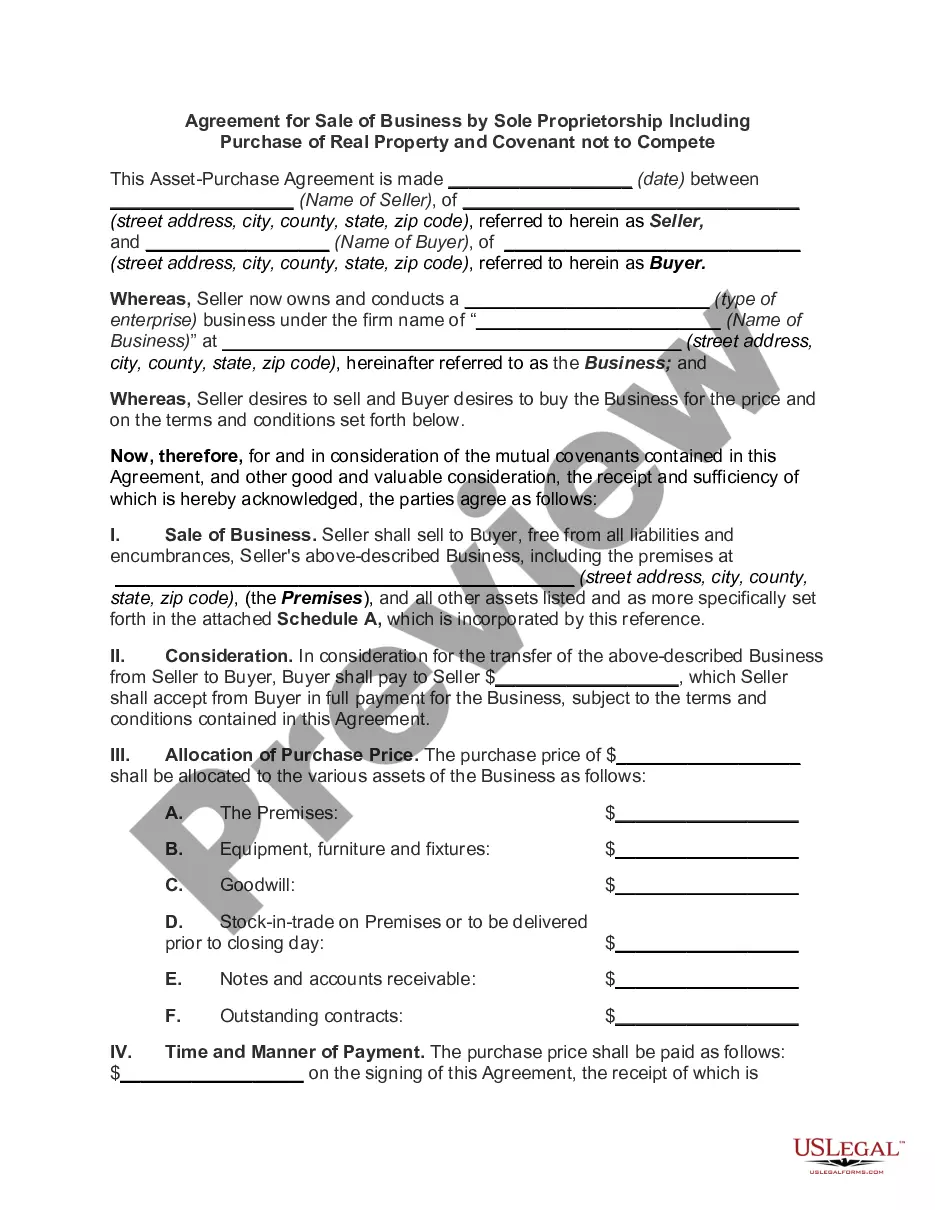

This form involves the sale of a small business where the real estate on which the Business is located is leased from a third party. This form assumes that the Seller has received the right to assign the lease from the lessor/owner.

Massachusetts Agreement for Sale of Business by Sole Proprietorship with Leased Premises

Instant download

Description

Free preview

How to fill out Agreement For Sale Of Business By Sole Proprietorship With Leased Premises?

Discovering the right authorized record design can be quite a struggle. Of course, there are plenty of templates available on the Internet, but how do you discover the authorized kind you need? Utilize the US Legal Forms web site. The assistance gives a large number of templates, such as the Massachusetts Agreement for Sale of Business by Sole Proprietorship with Leased Premises, which can be used for enterprise and personal requirements. Each of the kinds are inspected by pros and fulfill federal and state needs.

Should you be already listed, log in to your account and then click the Download button to find the Massachusetts Agreement for Sale of Business by Sole Proprietorship with Leased Premises. Use your account to search throughout the authorized kinds you might have purchased formerly. Visit the My Forms tab of your account and get an additional copy of your record you need.

Should you be a new consumer of US Legal Forms, allow me to share straightforward recommendations for you to adhere to:

- Initially, be sure you have chosen the right kind to your area/region. You may examine the shape while using Preview button and look at the shape outline to make certain it will be the right one for you.

- When the kind fails to fulfill your preferences, use the Seach industry to get the correct kind.

- When you are certain that the shape would work, go through the Acquire now button to find the kind.

- Opt for the costs program you want and enter the needed information. Create your account and purchase the order utilizing your PayPal account or credit card.

- Choose the file structure and obtain the authorized record design to your product.

- Comprehensive, modify and print out and signal the obtained Massachusetts Agreement for Sale of Business by Sole Proprietorship with Leased Premises.

US Legal Forms may be the greatest local library of authorized kinds for which you can find different record templates. Utilize the service to obtain appropriately-created documents that adhere to express needs.

Form popularity

FAQ

Asset Sale ? Capital Gains Tax Capital gains tax is the proceeds of your asset sale minus the original cost. You'll pay tax on the capital gain or loss on the assets sold. Here's a quick equation: Sale price ? purchase price = net proceeds.

Overview. A sole proprietorship cannot be sold as a single entity like a corporation. Instead, when a sole proprietor sells the business, the sale is treated as the sale of the separate and identifiable assets of the business. The sale of a disregarded entity is also treated as the sale of the entity's assets.

Sole proprietors and partners pay themselves simply by withdrawing cash from the business. Those personal withdrawals are counted as profit and are taxed at the end of the year.

A sole proprietorship cannot be sold as a single entity like a corporation. Instead, when a sole proprietor sells the business, the sale is treated as the sale of the separate and identifiable assets of the business.

A sole proprietor is someone who owns an unincorporated business by himself or herself.

As there is no separate entity under the law for a sole proprietorship business, contracts are normally signed by owner under his or her personal name. Even if the business uses a fictitious name, the owner will usually have his or her name written down in the checks issued by the clients.