Louisiana Agreement Replacing Joint Interest with Annuity

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Agreement Replacing Joint Interest With Annuity?

Locating the right sanctioned document template can be challenging. Naturally, there are numerous templates accessible online, but how do you obtain the sanctioned form you require.

Utilize the US Legal Forms platform. The service offers an extensive selection of templates, including the Louisiana Agreement Replacing Joint Interest with Annuity, which can be utilized for both business and personal purposes.

All forms are reviewed by professionals and comply with federal and state regulations.

Once you are confident that the form is appropriate, click the Get now button to obtain the form. Select the pricing plan you'd like and enter the required information. Create your account and pay for the order using your PayPal account or credit card. Choose the file format and download the sanctioned document template to your device. Complete, edit, print, and sign the obtained Louisiana Agreement Replacing Joint Interest with Annuity. US Legal Forms is indeed the largest collection of authorized forms where you can find various document templates. Take advantage of the service to acquire correctly designed documents that adhere to state regulations.

- If you are already registered, sign in to your account and click the Download button to retrieve the Louisiana Agreement Replacing Joint Interest with Annuity.

- Use your account to browse the authorized forms you have previously acquired.

- Navigate to the My documents section of your account and obtain an additional copy of the document you require.

- If you are a new user of US Legal Forms, here are straightforward steps for you to follow.

- First, ensure you have selected the correct form for your locality/region. You can view the form using the Review button and check the form details to confirm it is suitable for you.

- If the form does not meet your requirements, use the Search field to find the correct form.

Form popularity

FAQ

Non-residents working or earning income in Louisiana need to use Form IT-540NR to report their income. This form ensures compliance with state tax regulations even if you are not a resident. If you have engaged in a Louisiana Agreement Replacing Joint Interest with Annuity, it may be beneficial to consult with a tax professional to navigate any associated tax implications.

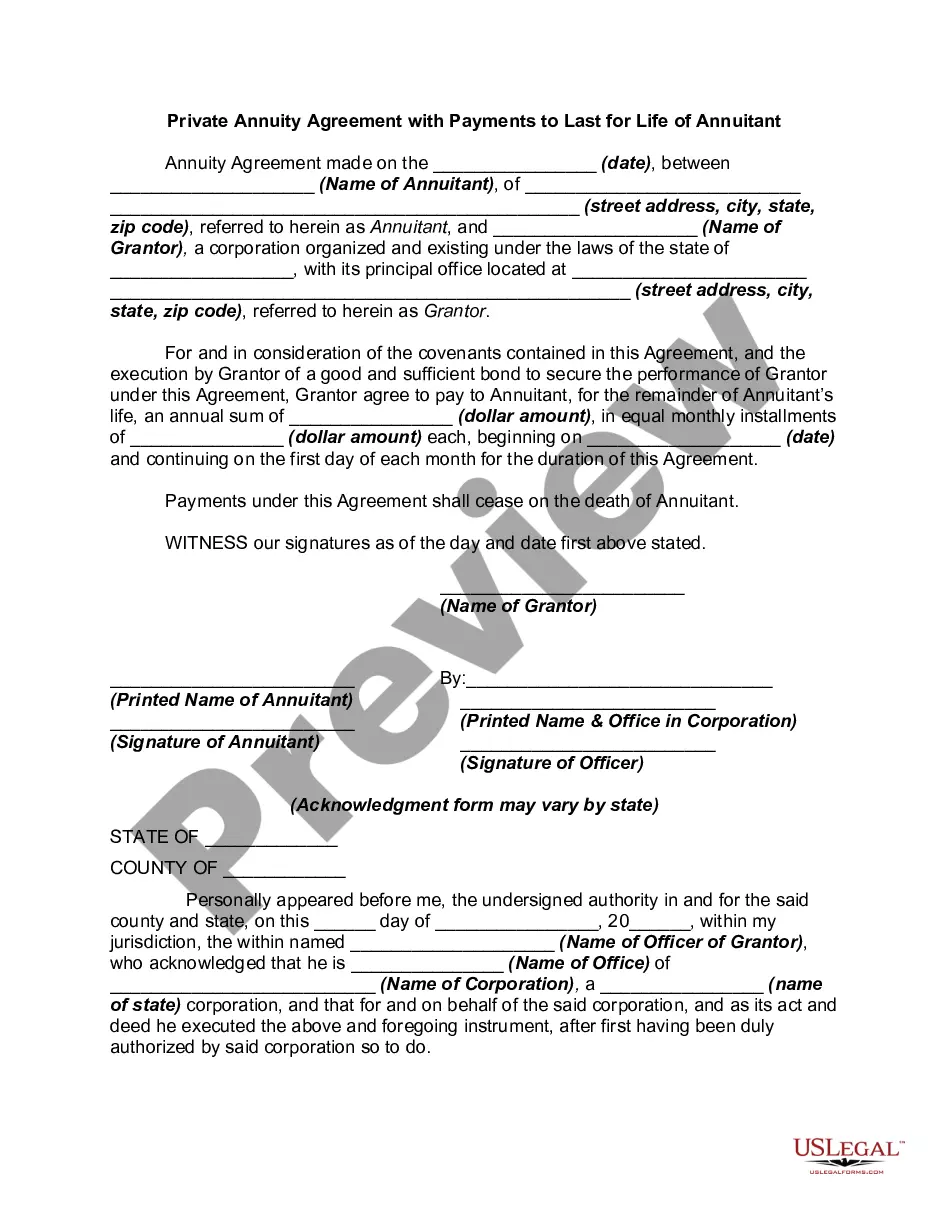

Definition: Replacement is any transaction where, in connection with the purchase of New Insurance or a New Annuity, you lapse, surrender, convert to Paid-up Insurance, Place on Extended Term, or borrow all or part of the policy loan values on an existing insurance policy or an annuity.

Generally, the Section 1035 exchange rules allow the owner of a financial product, such as a life insurance or annuity contract, to exchange one product for another without treating the transaction as a saleno gain is recognized when the first contract is disposed of, and there is no intervening tax liability.

The Section 1035 exchange rules allow the owner of a life insurance or annuity contract to exchange one product for another without treating the transaction as a taxable sale. A life insurance policy can be exchanged for an annuity, but you cannot exchange an annuity contract for new life insurance.

Key TakeawaysA whole life annuity is an annuity that pays a person for their lifetime, starting at an age agreed upon in the contract. The payment schedule can vary and can be as often as monthly or as infrequently as on an annual basis.

So what is not allowable in a 1035 exchange? Single Premium Immediate Annuities (SPIAs), Deferred Income Annuities (DIAs), and Qualified Longevity Annuity Contracts (QLACs) are not allowed because these are irrevocable income contracts.

Jointly owned annuities are similar to annuities owned by a single person in that the death benefit is triggered by the death of one of the owners. This means that although the second owner is still alive, the annuity will pay out the death benefit to the beneficiary.

A life insurance policy can be exchanged for an annuity under the rules of a 1035 exchange, but you cannot exchange an annuity contract for a life insurance policy.

So what is not allowable in a 1035 exchange? Single Premium Immediate Annuities (SPIAs), Deferred Income Annuities (DIAs), and Qualified Longevity Annuity Contracts (QLACs) are not allowed because these are irrevocable income contracts.

Through what's known as a 1035 exchange, you can convert your life insurance into an income annuity without paying taxes on your gains. You'll give up the death benefit, but you'll no longer have to pay premiums, and you'll lock in income for the rest of your life (or a specific number of years).