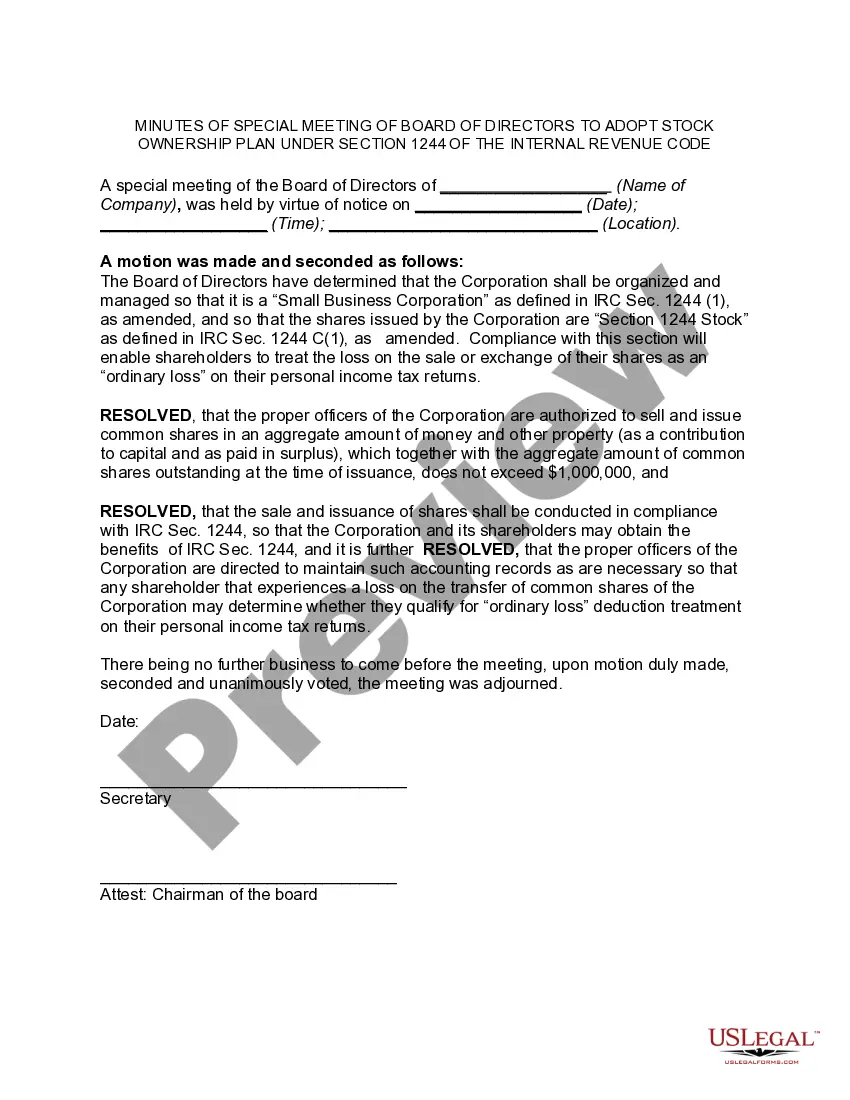

Kansas Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code

Description

to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code")

to Adopt Stock Ownership Plan under Section 1244 of the Internal Revenue Code")

How to fill out Minutes Of Special Meeting Of The Board Of Directors Of (Name Of Corporation) To Adopt Stock Ownership Plan Under Section 1244 Of The Internal Revenue Code?

US Legal Forms - one of the largest repositories of legal forms in the United States - offers a broad selection of legal document templates that you can download or print.

By utilizing the website, you can obtain thousands of forms for both business and personal purposes, organized by categories, states, or keywords.

You can find the latest versions of forms like the Kansas Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Approve Stock Ownership Plan under Section 1244 of the Internal Revenue Code in no time.

If the form doesn’t suit your needs, make use of the Search box at the top of the screen to find one that does.

Once you are satisfied with the form, confirm your choice by clicking the Buy Now button. Then, select your pricing plan and provide your credentials to create an account.

- If you already have an account, Log In to download the Kansas Minutes of Special Meeting of the Board of Directors of (Name of Corporation) to Approve Stock Ownership Plan under Section 1244 of the Internal Revenue Code from the US Legal Forms library.

- The Download button will appear on every form you view.

- You have access to all previously saved forms under the My documents section of your account.

- If you are using US Legal Forms for the first time, here are simple steps to get started.

- Ensure you have selected the correct form for your region/state.

- Preview the form to review its content.

Form popularity

FAQ

To qualify under Section 1244, these five requirements must be adhered to:The stock must be acquired in exchange for cash or property contributed to the corporation.The corporation must issue the stock directly to the investors.The corporation must be an actual, operating company.More items...?

Qualifying for Section 1244 StockThe stock must be issued by U.S. corporations and can be either a common or preferred stock.The corporation's aggregate capital must not have exceeded $1 million when the stock was issued and the corporation cannot derive more than 50% of its income from passive investments.More items...

HW: How are gains from the sale of § 1244 stock treated? losses? The general rule is that shareholders receive capital gain or loss treatment upon the sale or exchange of stock. However, it is possible to receive an ordinary loss deduction if the loss is sustained on small business stock (A§ 1244 stock).

Section 1244 of the Internal Revenue Code allows eligible shareholders of domestic small business corporations to deduct a loss on the disposal of such stock as an ordinary loss rather than a capital loss. Eligible investors include individuals, partnerships and LLCs taxed as partnerships.

1244(b)). Any loss in excess of the limit is a capital loss, subject to the capital loss rules. Thus, if the potential loss exceeds the $50,000 (or $100,000) limit, the stock should be disposed of in more than one year to maximize the ordinary loss treatment.

Section 1244 of the Internal Revenue Code is the small business stock provision enacted to allow shareholders of domestic small business corporations to deduct a loss on the disposal of such stock as an ordinary loss rather than as a capital loss, which is limited to only $3,000 annually.

The determination of whether stock qualifies as Section 1244 stock is made at the time of issuance. Section 1244 stock is common or preferred stock issued for money or other property by a domestic small business corporation (which can be a C or S corporation) that meets a gross receipts test.

1244 losses are allowed for NOL purposes without being limited by nonbusiness income. An annual limitation is imposed on the amount of Sec. 1244 ordinary loss that is deductible. The maximum deductible loss is $50,000 per year ($100,000 if a joint return is filed) (Sec.

Form 4797, Sales of Business Property, is used to report an ordinary loss on the sale of Section 1244 stock or a loss resulting from the stock becoming worthless. Attach Form 4797 to Form 1040.