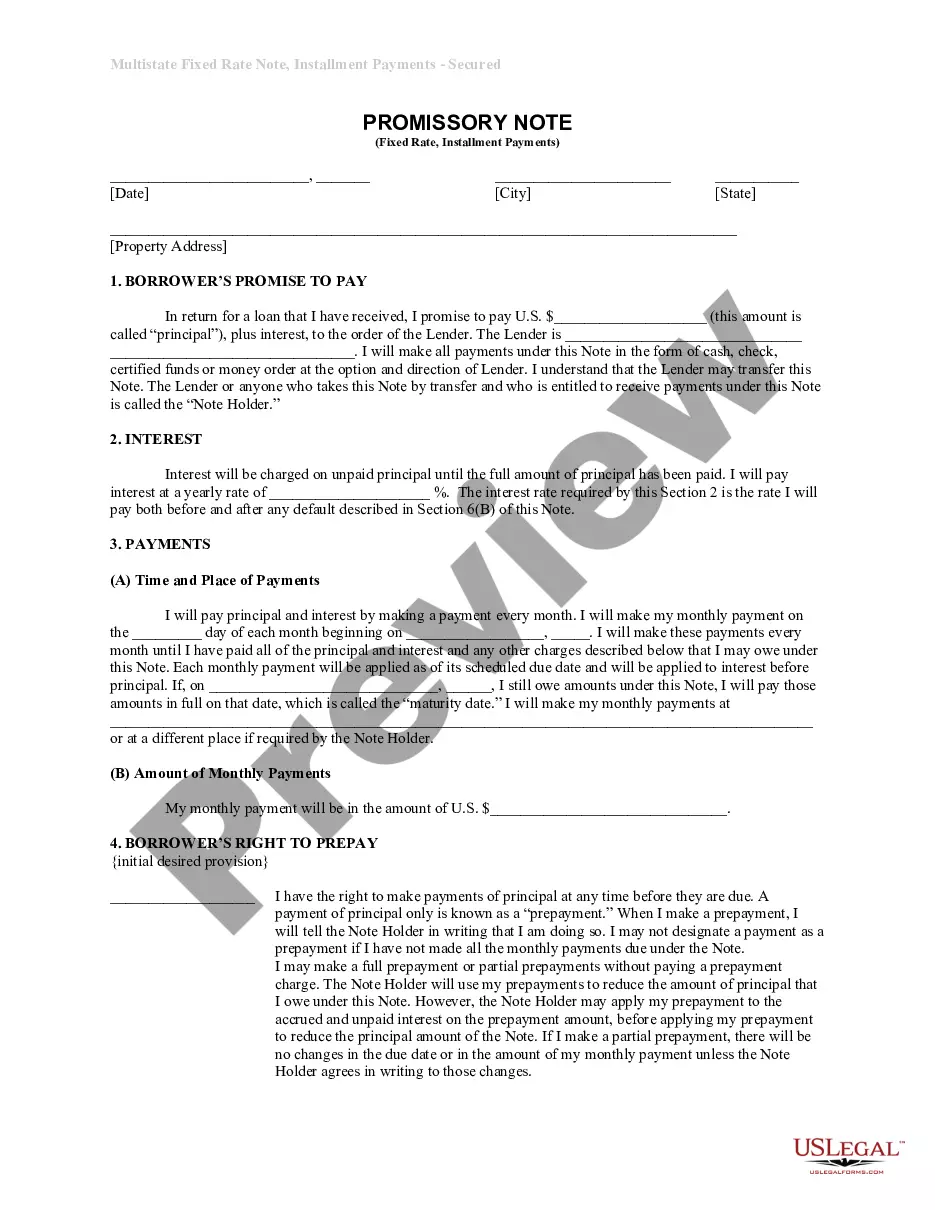

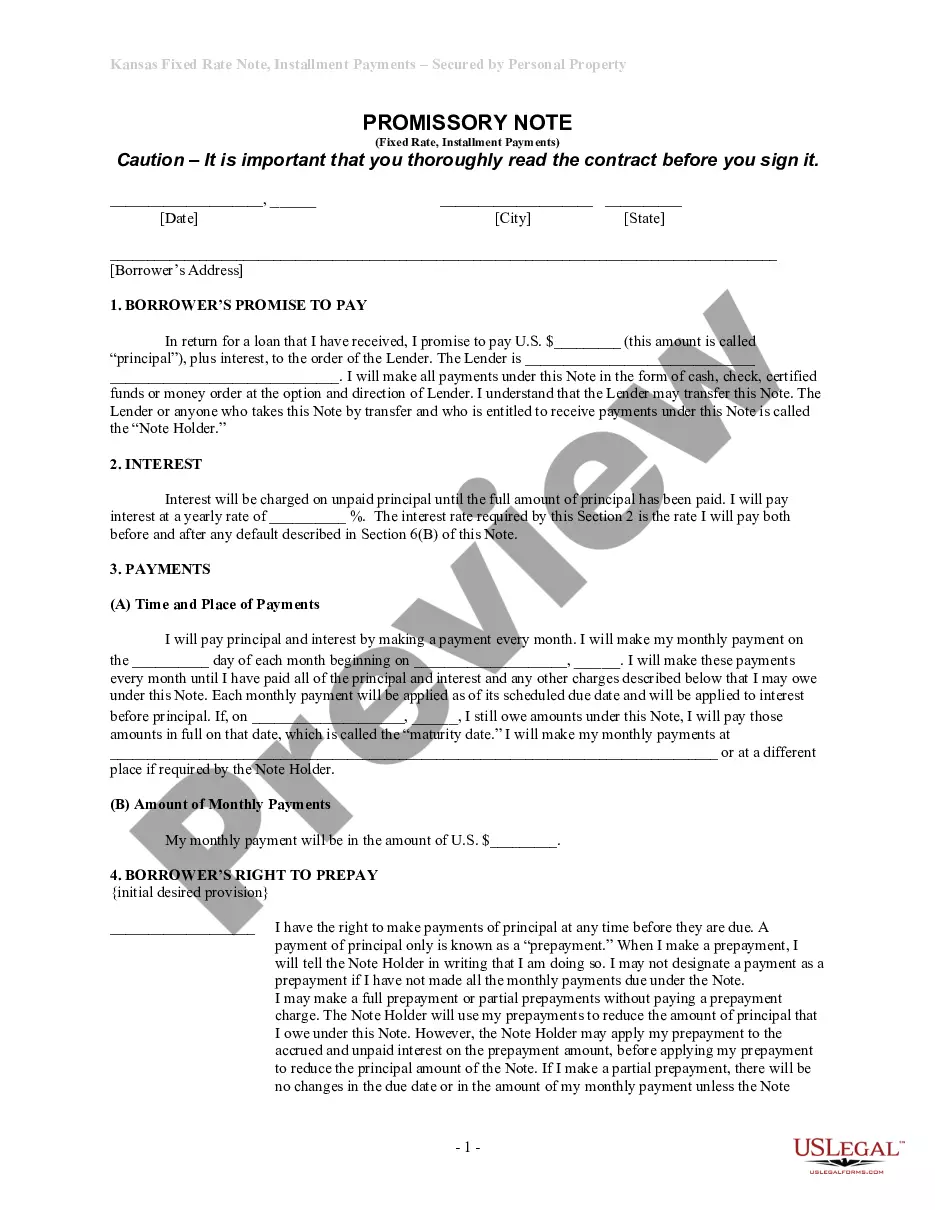

Kansas Installments Fixed Rate Promissory Note Secured by Commercial Real Estate

Overview of this form

The Kansas Installments Fixed Rate Promissory Note Secured by Commercial Real Estate is a legal document that outlines a borrower's promise to repay a loan with specific terms. This form is distinct from other promissory notes as it secures the loan with commercial real estate, ensuring the lender has a claim on the property if the borrower defaults. It establishes clear conditions regarding payment schedules, interest rates, and obligations, making it essential for any borrowing situation involving commercial properties.

What’s included in this form

- Date, city, and state of the loan agreement

- Borrower(s) and lender's details, including addresses

- Principal amount and interest rate terms

- Payment schedule and method of payment

- Prepayment rights and penalties

- Late payment charges and default conditions

- Secured status of the note by a mortgage or deed of trust

When to use this document

This form is typically used when a borrower needs to secure funding for a business-related purpose by providing commercial real estate as collateral. It is appropriate in situations such as purchasing property for a business, financing construction or renovations, or consolidating debts with secured financing. When a borrower intends to spread out repayments while offering their commercial property as security, this document is essential.

Intended users of this form

- Business owners seeking to finance commercial properties

- Individuals looking to borrow against their commercial real estate

- Lenders providing loans secured by real estate

- Real estate investors requiring structured payment terms from borrowers

How to prepare this document

- Identify the parties involved in the loan: the borrower(s) and lender.

- Specify the loan amount (principal) along with the interest rate.

- Enter the payment schedule, including the monthly payment amount and due dates.

- Communicate any prepayment options or penalties clearly.

- Ensure all parties sign and date the document to make it legally binding.

Does this form need to be notarized?

This form needs to be notarized to ensure legal validity. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to accurately document the loan amount or interest rate.

- Omitting necessary dates, which could lead to confusion about payment timelines.

- Not providing a clear description of the secured property.

- Leaving out signatures or failing to date the form correctly.

Why use this form online

- Convenience of completing and saving the form at your own pace.

- Editable fields that allow for easy input of specific information.

- Access to reliable legal templates drafted by licensed attorneys.

Legal use & context

- The promissory note legally binds the borrower to repay the specified amount under agreed terms.

- This form is enforceable in a court of law, provided it is completed correctly and includes all necessary information.

- Defaulting on the note can lead to significant legal consequences, including foreclosure on the secured property.

Quick recap

- The Kansas Installments Fixed Rate Promissory Note is essential for securing loans against commercial real estate.

- Proper completion and understanding of the terms can minimize legal risks.

- This form offers flexibility for prepayment options under specific conditions.

- Know the implications of default and the importance of timely payments to avoid penalties.

Looking for another form?

Form popularity

FAQ

Mortgage notes can be purchased through mortgage note brokerages (you can find hundreds online). They can also be purchased in shares of mortgage bundles through real estate investment trusts or other similar products.

Co-signers, often parents or other relatives with excellent credit and income, help under-qualified borrowers obtain mortgages. They act as guarantors and do not live in the home or hold an ownership interest. Lenders require co-signers to sign the note, but not the deed, at closing.

When you buy a note and mortgage, you're buying the debt that remains to be paid on the note, secured by the asset outlined in the mortgage. You're not buying the property -- you're buying the debt and secured interest in the property.

Private note holders, usually seller-financed property or business sales. Hedge or private equity funds that buy in bulk from banks and servicers and then resell. Note exchanges and marketplaces.

Mortgage notes can be a good real estate investment for people seeking passive income. When you buy a mortgage note, you receive monthly payments that include both interest and principle.

Home equity lines of credit. Business lines of credit. Business loans. Credit cards. Crowdfunding. Personal signature loans and lines of credit.

A promissory note is often referred to as a mortgage note and is the document generated and signed at closing. A mortgage, or mortgage loan, is a loan that allows a borrower to finance a home.The promissory note is exactly what it sounds like the borrower's written, signed promise to repay the loan.

The mortgage note is part of your closing papers and you will receive a copy at closing. If you lose your closing papers or they get destroyed, you can obtain a copy of your mortgage note by searching the county's records or contacting the registry of deeds.

Private note holders, usually seller-financed property or business sales. Hedge or private equity funds that buy in bulk from banks and servicers and then resell. Note exchanges and marketplaces.