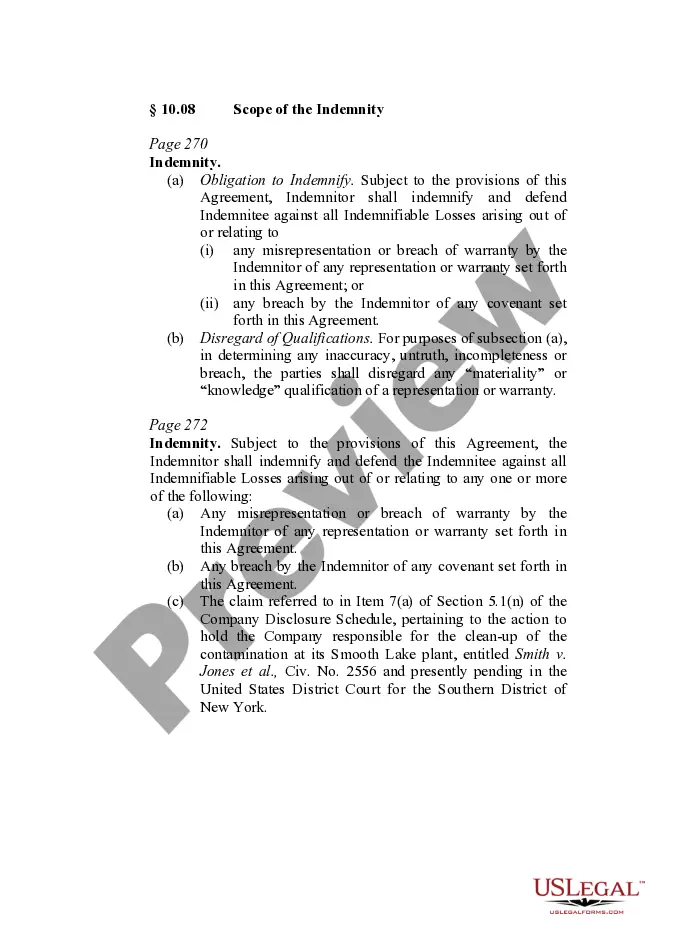

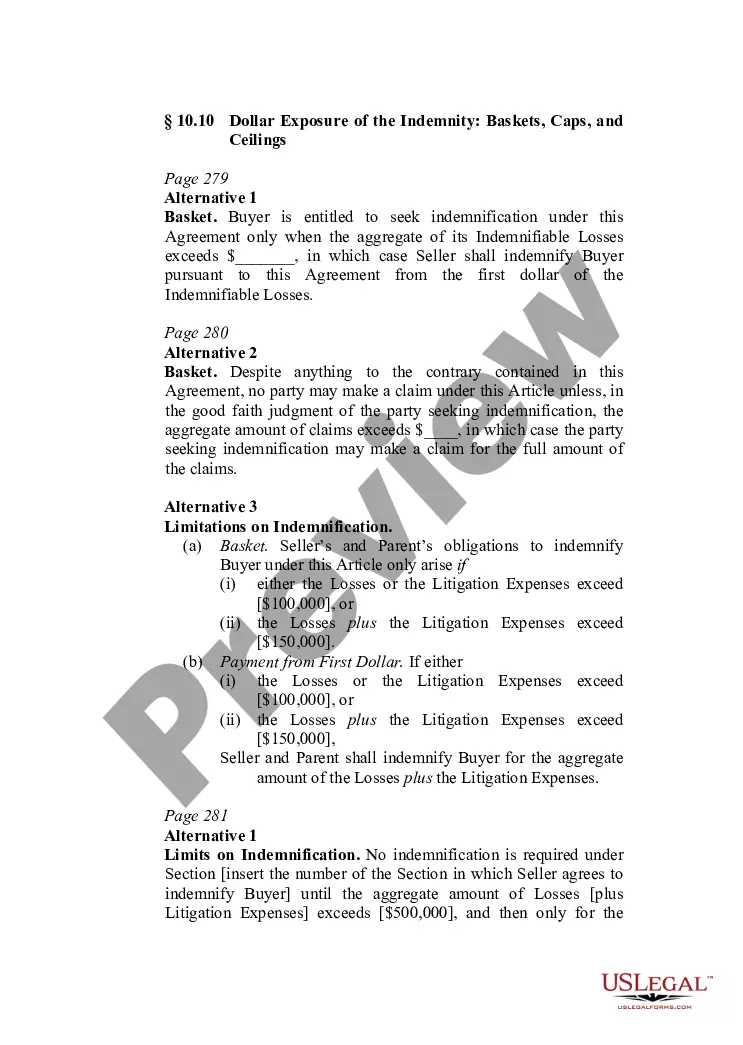

This form provides boilerplate contract clauses that restrict or limit the dollar exposure of any indemnity under the contract agreement with regards to taxes or insurance considerations.

Indiana Indemnity Provisions - Dollar Exposure of the Indemnity regarding Tax and Insurance Considerations

Category:

State:

Multi-State

Control #:

US-ND1011

Format:

Word;

PDF

Instant download

Description

How to fill out Indemnity Provisions - Dollar Exposure Of The Indemnity Regarding Tax And Insurance Considerations?

Have you been inside a situation that you need to have papers for possibly organization or person reasons virtually every working day? There are tons of legitimate file templates available on the net, but discovering ones you can trust isn`t easy. US Legal Forms provides a large number of kind templates, just like the Indiana Indemnity Provisions - Dollar Exposure of the Indemnity regarding Tax and Insurance Considerations, that are composed to satisfy federal and state needs.

If you are already acquainted with US Legal Forms website and possess a merchant account, just log in. Following that, you may down load the Indiana Indemnity Provisions - Dollar Exposure of the Indemnity regarding Tax and Insurance Considerations format.

Unless you offer an account and need to start using US Legal Forms, adopt these measures:

- Find the kind you want and ensure it is for that correct metropolis/area.

- Make use of the Review option to review the shape.

- Browse the outline to ensure that you have chosen the proper kind.

- In case the kind isn`t what you are seeking, use the Look for field to obtain the kind that meets your needs and needs.

- Once you get the correct kind, simply click Buy now.

- Choose the pricing program you desire, complete the necessary details to produce your account, and buy your order using your PayPal or charge card.

- Pick a hassle-free paper formatting and down load your backup.

Find all of the file templates you might have bought in the My Forms menu. You can get a further backup of Indiana Indemnity Provisions - Dollar Exposure of the Indemnity regarding Tax and Insurance Considerations any time, if necessary. Just select the essential kind to down load or print the file format.

Use US Legal Forms, the most substantial selection of legitimate forms, in order to save time and stay away from mistakes. The support provides appropriately produced legitimate file templates that you can use for an array of reasons. Produce a merchant account on US Legal Forms and commence making your life a little easier.

Form popularity

FAQ

For example, in the case of home insurance, the homeowner pays insurance premiums to the insurance company in exchange for the assurance that the homeowner will be indemnified if the house sustains damage from fire, natural disasters, or other perils specified in the insurance agreement. Indemnity: What It Means in Insurance and the Law - Investopedia investopedia.com ? terms ? indemnity investopedia.com ? terms ? indemnity

In a business transaction, a letter of indemnity (LOI) is a contractual document guaranteeing that specific provisions will be met between two parties in the event of a mishap leading to financial loss or damage to goods. An LOI is drafted by third-party institutions such as banks or insurance companies. What is Letter of Indemnity?| Meaning, Sample, Importance & More dripcapital.com ? en-us ? resources ? blog dripcapital.com ? en-us ? resources ? blog

Letters of indemnity should include the names and addresses of both parties involved, plus the name and affiliation of the third party. Detailed descriptions of the items and intentions are also required, as are the signatures of the parties and the date of the contract's execution. What Is a Letter of Indemnity (LOI)? Definition and Example - Investopedia investopedia.com ? terms ? letterofindemnity investopedia.com ? terms ? letterofindemnity

How to Write an Indemnity Agreement Consider the Indemnity Laws in Your Area. ... Draft the Indemnification Clause. ... Outline the Indemnification Period and Scope of Coverage. ... State the Indemnification Exceptions. ... Specify How the Indemnitee Notifies the Indemnitor About Claims. ... Write the Settlement and Consent Clause.

Example 1: A service provider asking their customer to indemnify them to protect against misuse of their work product. Example 2: A rental car company, as the rightful owner of the car, having their customer indemnify them from any damage caused by the customer during the course of the retnal. Indemnification Clause: Meaning & Samples (2022) - Contracts Counsel contractscounsel.com ? indemnification-clause contractscounsel.com ? indemnification-clause

Letters of indemnity should include the names and addresses of both parties involved, plus the name and affiliation of the third party. Detailed descriptions of the items and intentions are also required, as are the signatures of the parties and the date of the contract's execution.

An indemnification clause should clearly define the following elements: who are the indemnifying party and the indemnified party, what are the covered claims or losses, what are the obligations and duties of each party, and what are the exclusions or limitations of the indemnity.

Example 1: A service provider asking their customer to indemnify them to protect against misuse of their work product. Example 2: A rental car company, as the rightful owner of the car, having their customer indemnify them from any damage caused by the customer during the course of the retnal.