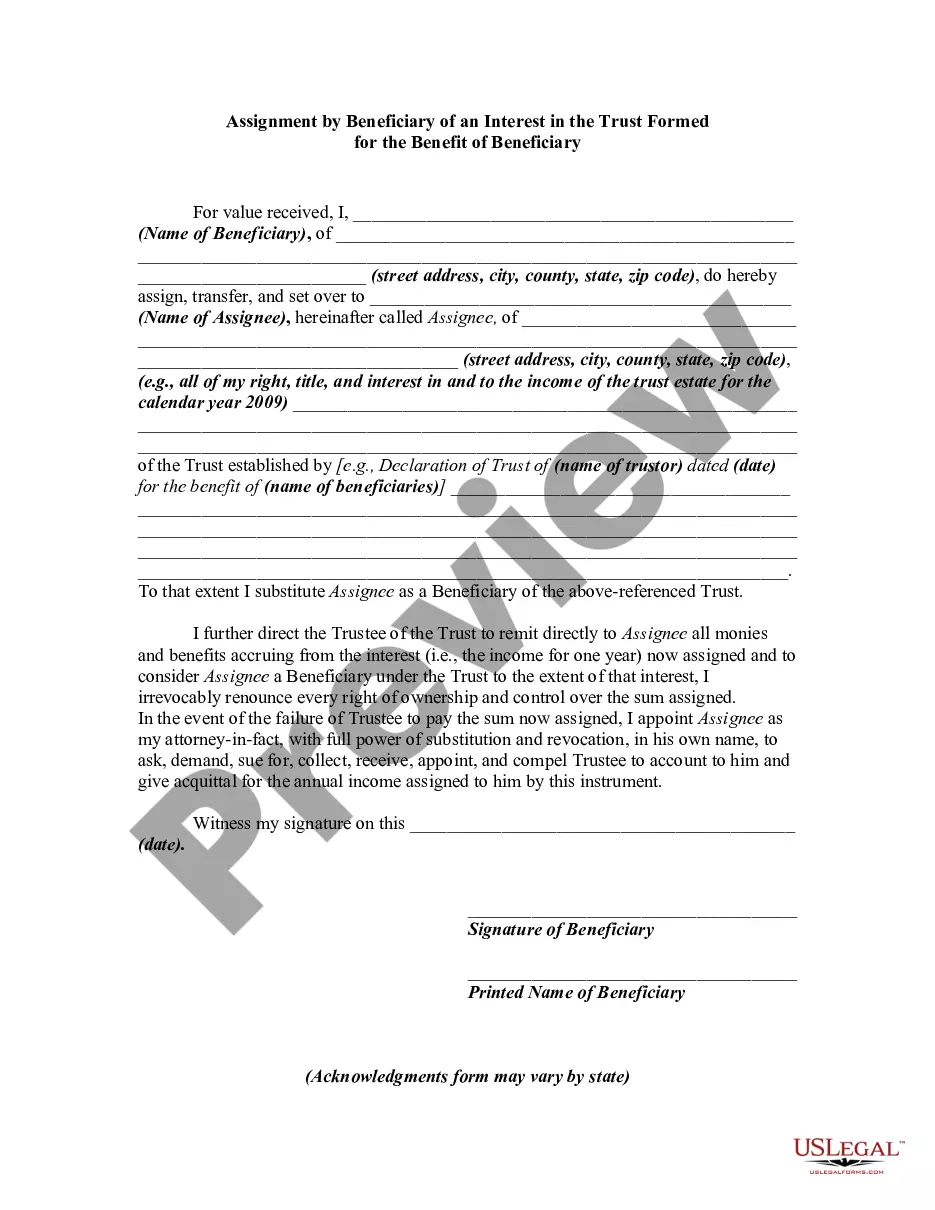

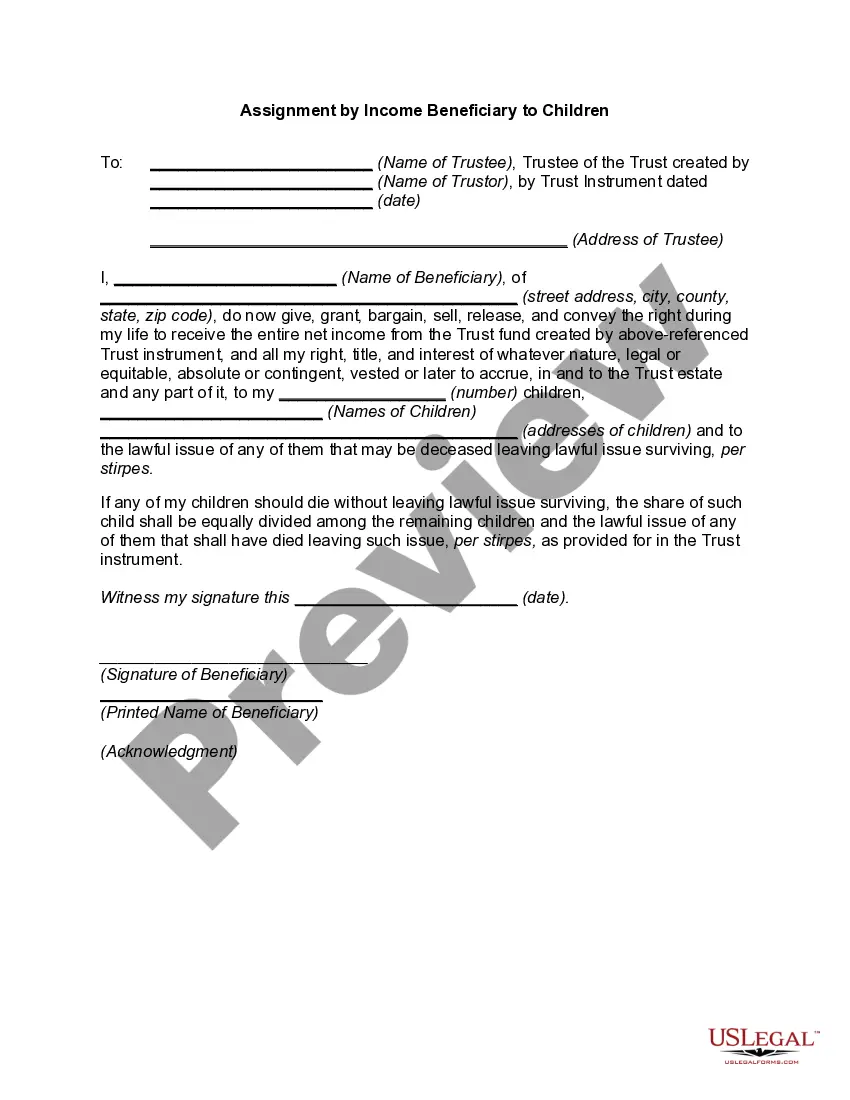

An assignment by a beneficiary of a portion of his or her interest in a trust is usually regarded as a transfer of a right, title, or estate in property rather than a chose in action (like an account receivable). As a general rule, the essentials of such an assignment or transfer are the same as those for any transfer of real or personal property. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust

Instant download

Description

Free preview

How to fill out Assignment By Beneficiary Of A Percentage Of The Income Of A Trust?

Locating the appropriate authentic document template can be quite a challenge.

Of course, there are numerous templates available online, but how can you find the genuine type you need.

Utilize the US Legal Forms website. This service provides thousands of templates, such as the Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust, which you can use for business and personal purposes.

If the form does not meet your requirements, use the Search area to find the correct type. Once you are certain that the form is appropriate, click on the Buy now button to obtain the form. Select the pricing plan you prefer and provide the necessary information. Create your account and pay for your order using your PayPal account or credit card. Choose the file format and download the legal document template to your system. Complete, edit, print, and sign the obtained Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust. US Legal Forms is the largest collection of legal forms from which you can find a variety of document templates. Use the service to download professionally-crafted papers that meet state standards.

- Each of these forms is reviewed by professionals and complies with federal and state regulations.

- If you are already signed up, Log In to your account and press the Download button to get the Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust.

- Use your account to explore the authorized forms you have previously acquired.

- Visit the My documents tab within your account and retrieve another copy of the document you require.

- If you are a new user of US Legal Forms, here are simple instructions for you to follow.

- Firstly, ensure that you have chosen the correct type for the city/county. You can examine the form using the Review button and read the details to confirm it's suitable for you.

Form popularity

FAQ

Typically, you do not receive a 1099 for income distributed from a trust; instead, you get a Schedule K-1. Some exceptions exist depending on the type of income, but the K-1 will provide relevant details for your tax reporting. When dealing with an Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust, make sure to consult with a tax professional to ensure you are following proper reporting procedures.

To report income from a trust, you will generally receive a Schedule K-1 from the trust, detailing your share of the income. This income will be included on your personal tax return. It's important to include this information accurately to comply with tax regulations. If you're utilizing an Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust, understand how it may affect your tax obligations.

Trust income is generally taxed to the beneficiary in the year it is distributed. When you engage in an Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust, you must report the income received on your tax return. This taxation can vary based on the type of income and the laws applicable in your state. Staying informed about tax implications helps beneficiaries make smart financial decisions.

The distribution of income from a trust refers to how the earnings generated by the trust assets are allocated to the beneficiaries. In the case of an Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust, beneficiaries receive a specified portion of the income, allowing for planned financial support. This setup can help beneficiaries manage their finances and provide stability. Understanding how these distributions work is essential for effective trust management.

Allocating trust income to beneficiaries involves following the provisions set out in the trust agreement. You will need to take into account the percentages or specific instructions given for income distribution. If your situation includes an Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust, you should ensure that each beneficiary receives their correct allocation as outlined in the trust.

A beneficiary is a broad term that refers to anyone entitled to receive benefits from a trust or estate. In contrast, an income beneficiary specifically receives income generated by the trust's assets. Understanding these distinctions is essential, especially with an Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust, as it dictates who receives what portion of trust income.

Typically, beneficiaries do not receive a 1099 form directly from the trust. Instead, they receive a Schedule K-1, which details their share of the trust's income. If you're a beneficiary of an Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust, you should rely on this form for accurate income reporting to the IRS.

Yes, you usually need to report beneficiary income on your tax return, especially if it comes from a trust. If you receive an Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust, this income is likely taxable and requires reporting. Proper reporting ensures compliance with tax laws and prevents future issues with the IRS.

Yes, income from a trust can be taxable to the beneficiary, depending on the type of trust and its structure. If you receive an Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust, you'll generally need to report this income on your tax return. Consult with a tax professional to accurately assess your tax obligations regarding trust income.

Beneficiary income of a trust refers to the share of income that a beneficiary receives from the trust’s earnings. This can include interest, dividends, and other income generated by the trust assets. If you're involved with an Indiana Assignment by Beneficiary of a Percentage of the Income of a Trust, the income received will typically be proportionate to your designated percentage. Understanding this can help beneficiaries manage their tax responsibilities.