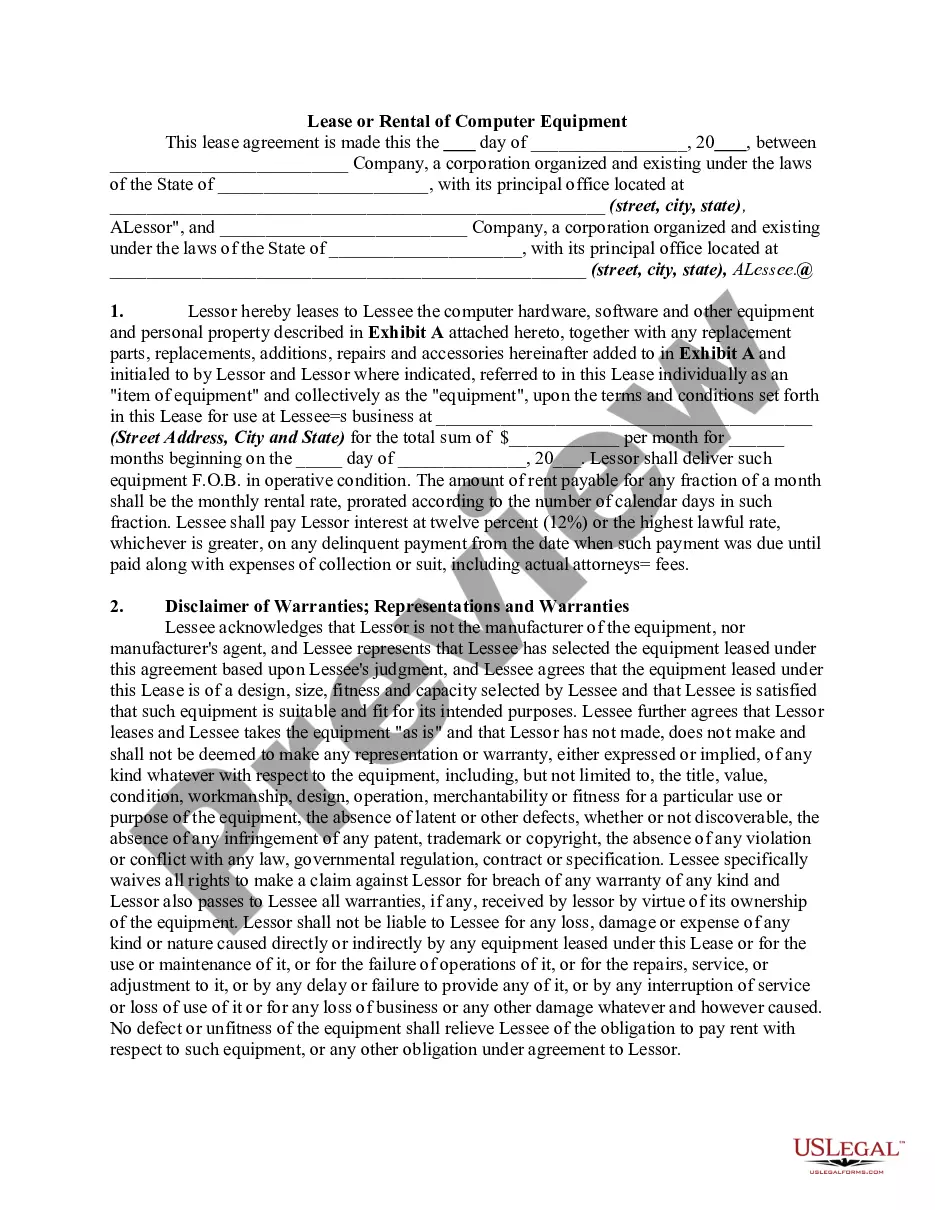

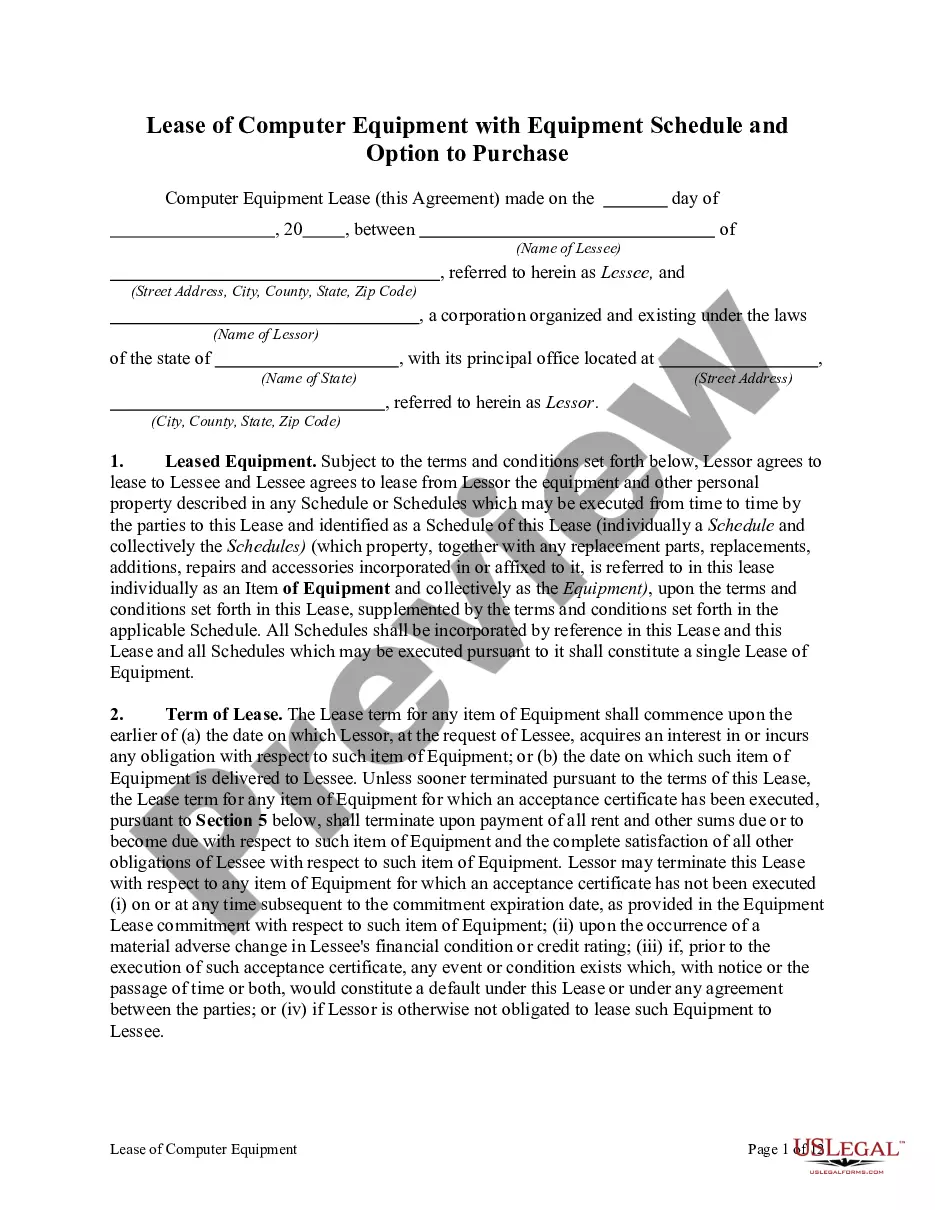

Iowa Computer Equipment Lease with Equipment Schedule

Description

How to fill out Computer Equipment Lease With Equipment Schedule?

You may commit hours online searching for the legal papers design which fits the federal and state needs you require. US Legal Forms offers 1000s of legal kinds which can be evaluated by professionals. It is simple to acquire or printing the Iowa Computer Equipment Lease with Equipment Schedule from our services.

If you currently have a US Legal Forms accounts, you may log in and click on the Down load button. Next, you may total, change, printing, or indication the Iowa Computer Equipment Lease with Equipment Schedule. Every single legal papers design you buy is your own property permanently. To obtain an additional copy for any acquired type, visit the My Forms tab and click on the corresponding button.

If you are using the US Legal Forms internet site the first time, stick to the easy guidelines under:

- Initial, be sure that you have chosen the proper papers design for that county/area of your choice. Read the type information to make sure you have chosen the proper type. If available, use the Review button to check throughout the papers design too.

- If you wish to find an additional variation in the type, use the Look for field to discover the design that fits your needs and needs.

- Once you have discovered the design you would like, click Purchase now to move forward.

- Choose the prices program you would like, key in your accreditations, and register for a free account on US Legal Forms.

- Complete the financial transaction. You can use your charge card or PayPal accounts to cover the legal type.

- Choose the format in the papers and acquire it to the device.

- Make modifications to the papers if needed. You may total, change and indication and printing Iowa Computer Equipment Lease with Equipment Schedule.

Down load and printing 1000s of papers templates using the US Legal Forms website, which provides the biggest variety of legal kinds. Use skilled and condition-particular templates to handle your organization or personal needs.

Form popularity

FAQ

Some goods are exempt from sales tax under Iowa law. Examples include most non-prepared food items, prescription drugs, and medical supplies.

Sales of tangible personal property in Iowa are subject to sales tax unless exempted by state law. Sales of services are exempt from Iowa sales tax unless taxed by state law. The retailer must add the tax to the price and collect the tax from the purchaser.

*Instead of the 6% state sales/use tax (and local option tax where applicable), a 5% state excise tax applies to purchases of the following specific construction machinery and equipment: Self-propelled building equipment.

The rental of tangible personal property in Texas is subject to sales or use tax. A rental occurs when possession but not title to tangible personal property is transferred for consideration.

(5)Lease or rental of all tangible personal property now subject to tax. On and after July 1, 1984, the lease or rental of all tangible personal property is subject to tax. See rule 701-2618. (422) for information concerning additional transactions subject to tax after that effective date.

Manufacturing Exemption Sales of machinery, equipment, replacement parts, supplies, computers, computer peripherals, and materials used to construct or self-construct those items are exempt from tax if the items are any of the following: Directly and primarily used in processing by a manufacturer.

A 5% tax is imposed on the sales price of all equipment, as defined by Iowa Code section 423D. 1, sold or used in Iowa. This tax is reported and remitted on the monthly sales and use tax return. No permit other than an Iowa sales and use tax permit is required to collect and report this tax.

In the state of Iowa, the rental of building equipment is exempt from sales and use tax when used in new construction, reconstruction, alteration, expansion or remodeling.