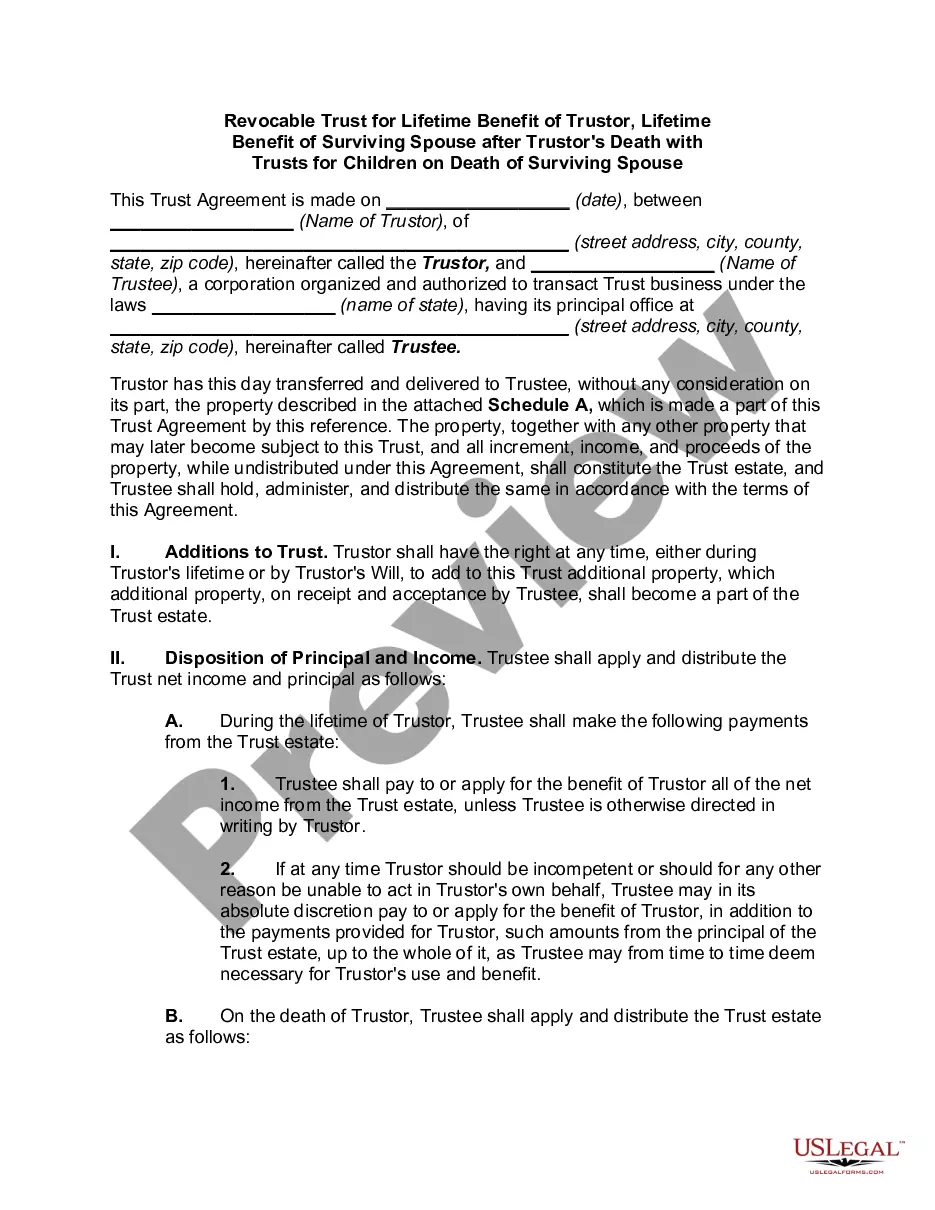

Georgia Revocable Trust for Lifetime Benefit of Trustor for Lifetime Benefit of Surviving Spouse after Death of Trustor's with Annuity

Description

How to fill out Revocable Trust For Lifetime Benefit Of Trustor For Lifetime Benefit Of Surviving Spouse After Death Of Trustor's With Annuity?

Are you in a circumstance where you need documents for either business or personal purposes almost consistently.

There are numerous legitimate templates available online, but finding ones you can rely on is challenging.

US Legal Forms offers thousands of document templates, such as the Georgia Revocable Trust for Lifetime Benefit of Trustor for Lifetime Benefit of Surviving Spouse after Death of Trustor's with Annuity, designed to meet both federal and state regulations.

Once you find the right form, click Buy now.

Choose the pricing plan you want, provide the necessary details to create your account, and complete the payment using your PayPal or credit card.

- If you are familiar with the US Legal Forms website and have an account, simply Log In.

- Next, you can download the Georgia Revocable Trust for Lifetime Benefit of Trustor for Lifetime Benefit of Surviving Spouse after Death of Trustor's with Annuity template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Find the form you need and ensure it is for your correct city/region.

- Use the Preview button to review the form.

- Check the description to confirm you have selected the correct form.

- If the form is not what you are looking for, use the Search box to locate the form that suits your requirements.

Form popularity

FAQ

What happens in this type of trust is that the trust is a joint revocable trust when both spouses are alive. When one of the spouses dies, the trust will then split into two trusts automatically. Each trust will have half the assets of the trust along with the separate property of the spouse.

The reason for naming a trust as the primary beneficiary is that, upon your death, the life insurance proceeds would be payable to your trust, and subject to the rules of your trust. This can be very beneficial if you want to place conditions and restrictions on the distribution of life insurance proceeds.

The primary disadvantage of naming a trust as beneficiary is that the retirement plan's assets will be subjected to required minimum distribution payouts, which are calculated based on the life expectancy of the oldest beneficiary.

Trusts are not considered individuals; therefore, life insurance proceeds paid to trusts are generally subjected to estate tax. Also, the proceeds payable to a trust may not qualify for the inheritance tax exemption provided by some states for insurance payable to a named beneficiary.

200dThe bottom line is that if you are using revocable living trusts as an estate tax planning vehicle, the trust should be listed as the primary beneficiary of your life insurance policy as opposed to your spouse.

An irrevocable trust or a revocable trust can both be listed your life insurance beneficiary, and they each come with their own set of pros and cons. Most young families (including my own) have a revocable trust.

A revocable living trust becomes irrevocable once the sole grantor or dies or becomes mentally incapacitated. If you have a joint trust for you and your spouse, then a portion of the joint trust can become irrevocable when the first spouse dies and will become irrevocable when the last spouse dies.

After one spouse dies, the surviving spouse is free to amend the terms of the trust document that deal with his or her property, but can't change the parts that determine what happens to the deceased spouse's trust property. You can make a valid living trust online, quickly and easily, with Nolo's Online Living Trust.

Upon the death of the grantor, grantor trust status terminates, and all pre-death trust activity must be reported on the grantor's final income tax return. As mentioned earlier, the once-revocable grantor trust will now be considered a separate taxpayer, with its own income tax reporting responsibility.

Under typical circumstances, the surviving spouse would become the sole trustee after the death of one spouse. The surviving spouse would control the shared property, and the personal property of the deceased spouse would be distributed to the beneficiaries.