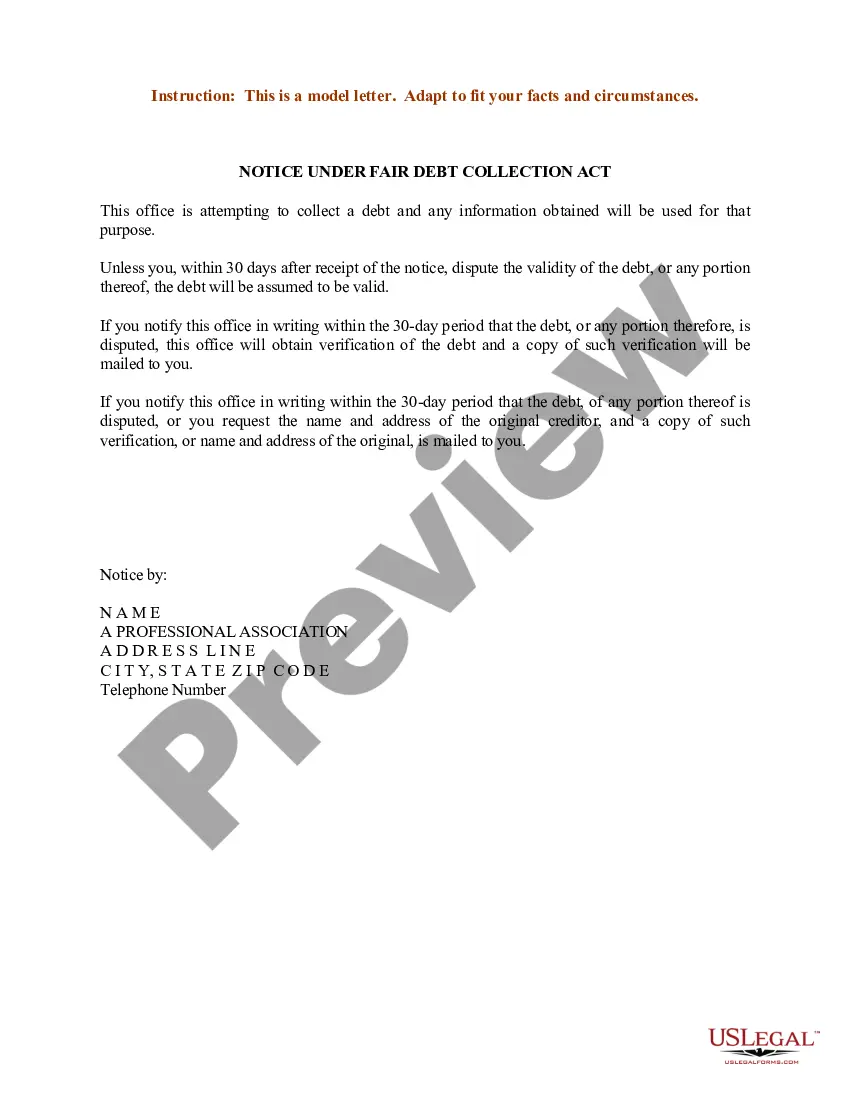

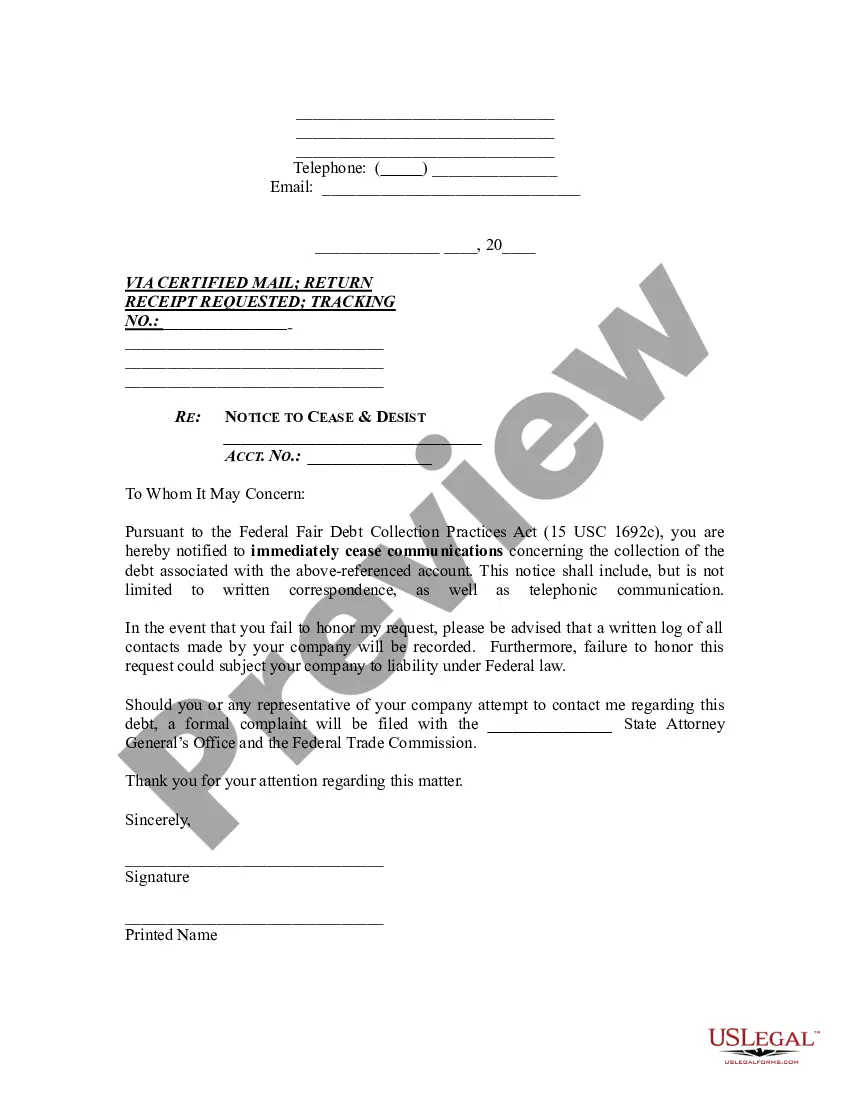

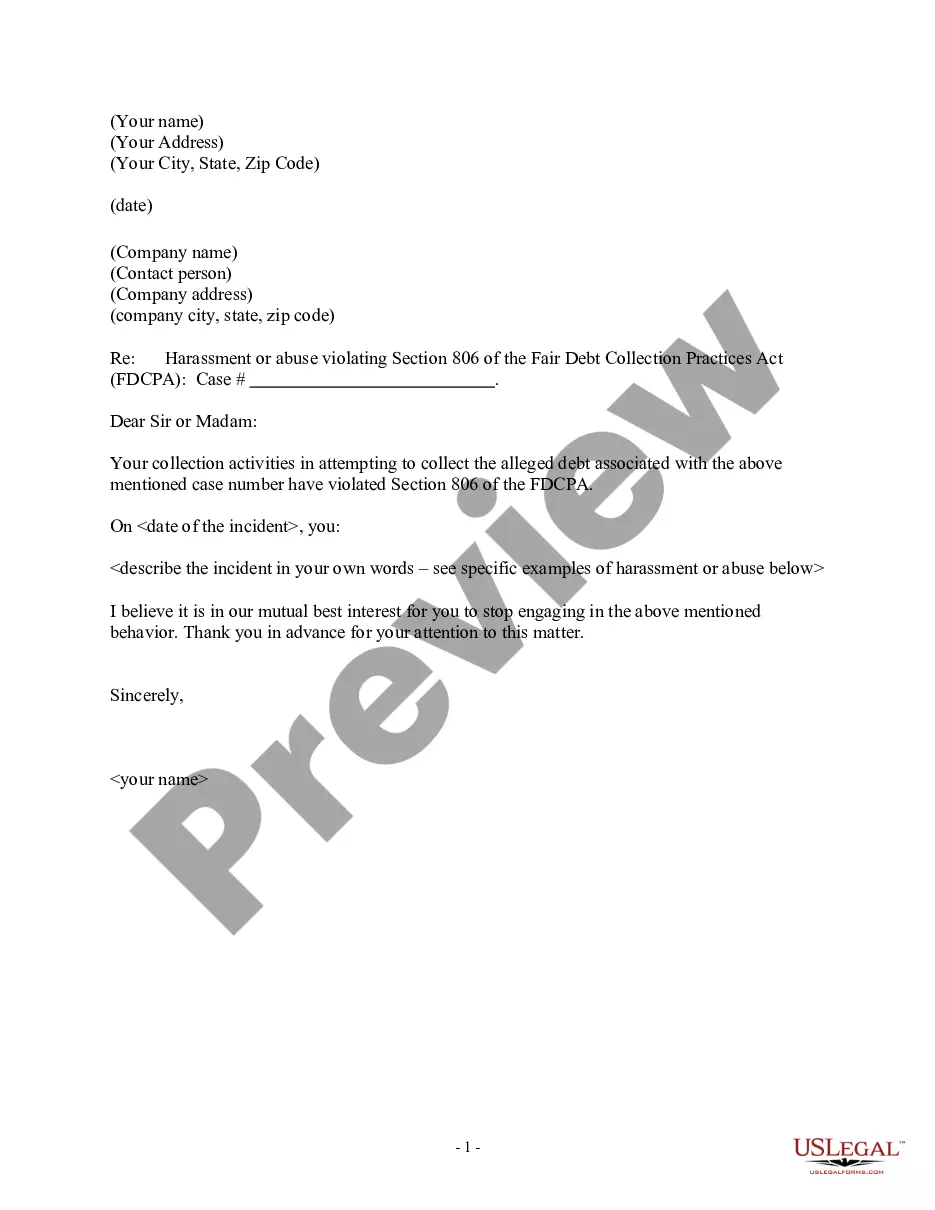

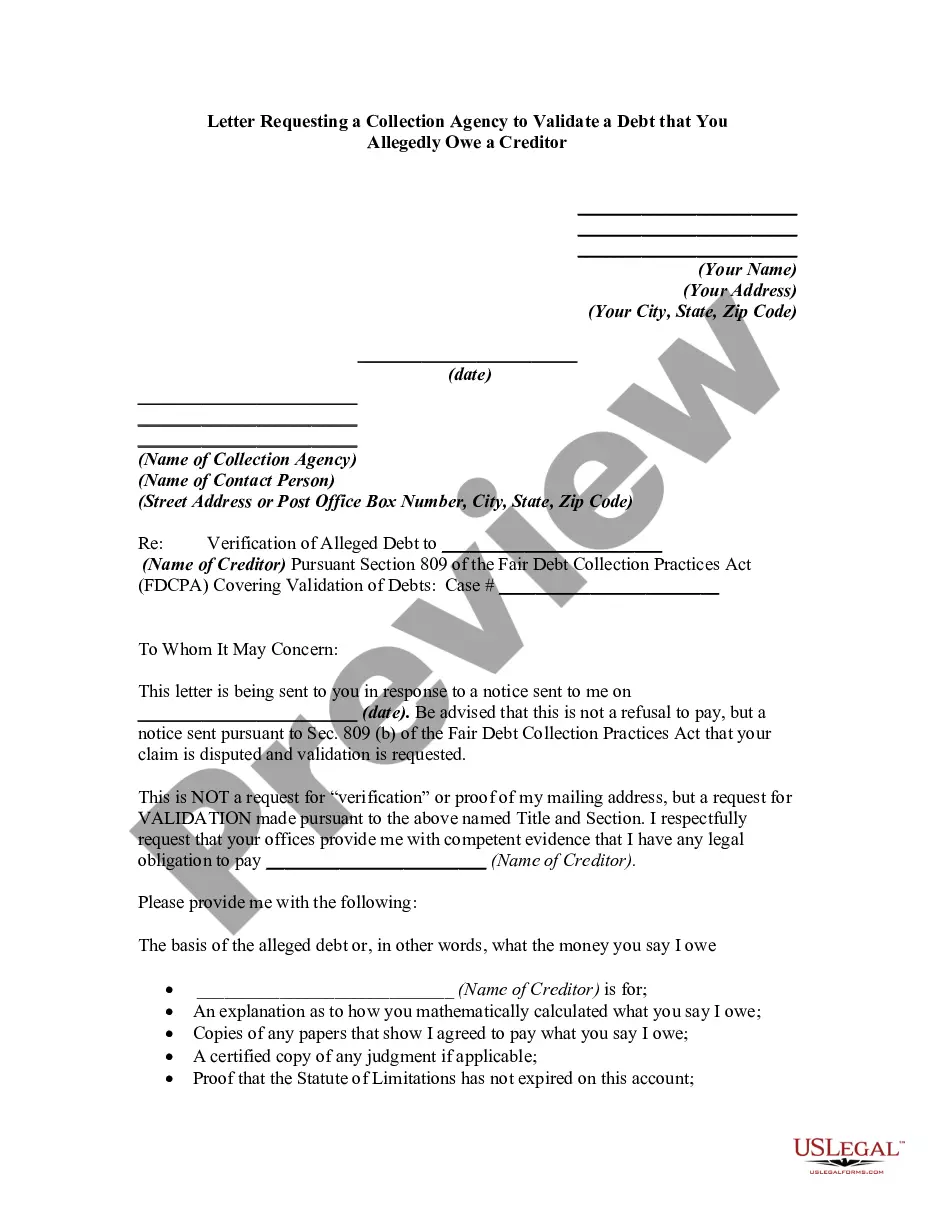

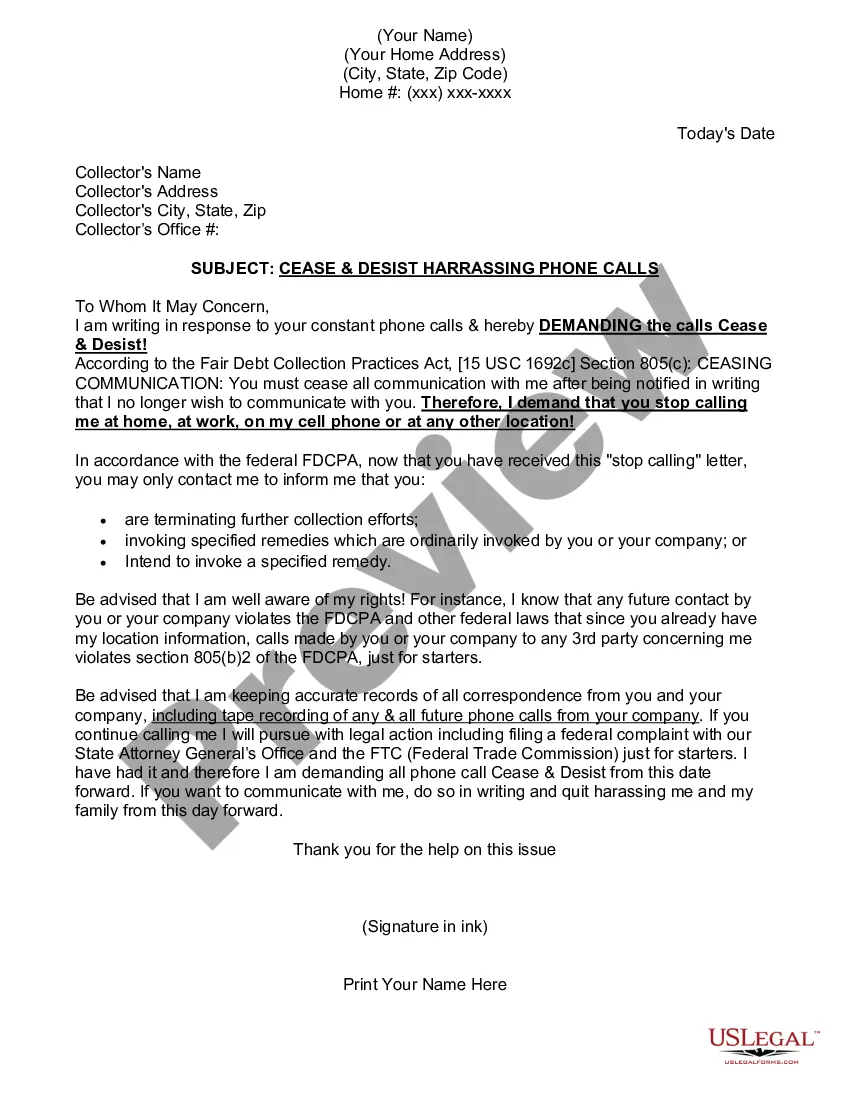

This NOTICE OF HARRASSMENT & VALIDATION OF DEBT is to be used when creditors call you repeatedly and mail you letters too. This form includes a cease and desist and a validation of debt, 2 letters in one.

Delaware Notice of Harassment and Validation of Debt

Instant download

Description

How to fill out Notice Of Harassment And Validation Of Debt?

If you want to total, download, or print legal document templates, utilize US Legal Forms, the largest selection of legal forms available online.

Take advantage of the site’s straightforward and convenient search to find the documents you need.

Numerous templates for business and personal purposes are organized by categories and states, or keywords. Use US Legal Forms to obtain the Delaware Notice of Harassment and Validation of Debt in just a few clicks.

Every legal document template you purchase is yours indefinitely. You have access to every form you acquired in your account. Click on the My documents section and select a form to print or download again.

Compete and download, and print the Delaware Notice of Harassment and Validation of Debt with US Legal Forms. There are thousands of professional and state-specific forms available for your business or personal needs.

- If you are currently a US Legal Forms user, Log In to your account and click the Download button to access the Delaware Notice of Harassment and Validation of Debt.

- You can also retrieve forms you previously acquired from the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Ensure you have chosen the form for the correct city/state.

- Step 2. Use the Preview option to review the form’s details. Don’t forget to read the description.

- Step 3. If you are not satisfied with the form, use the Search box at the top of the screen to find alternative versions of the legal form template.

- Step 4. Once you have found the form you need, click the Buy now button. Select your preferred pricing plan and enter your credentials to create an account.

- Step 5. Complete the payment. You can use your credit card or PayPal account to finalize the transaction.

- Step 6. Choose the format of the legal form and download it to your device.

- Step 7. Fill out, edit, and print or sign the Delaware Notice of Harassment and Validation of Debt.

Form popularity

FAQ

To dispute the validity of a debt, you should write a formal dispute letter to the creditor, outlining your reasons for the dispute. Include any evidence you have that supports your claim, such as payment records. It’s crucial to send this letter via certified mail to ensure you have proof of your communication. The US Legal platform can assist you by providing templates and guidance for creating an effective dispute letter related to your Delaware Notice of Harassment and Validation of Debt.

Yes, pursuing debt validation is often beneficial for consumers. It allows you to confirm the accuracy of the debt and ensures that you are not paying for a debt that is invalid or incorrectly attributed to you. This process can help protect your financial interests and give you peace of mind. Using the US Legal platform can further enhance your understanding and execution of the Delaware Notice of Harassment and Validation of Debt.

To file a debt validation claim, first request a debt validation letter from the creditor or collection agency. This letter should include details about the debt and verify its legitimacy. If the creditor fails to provide this information, you can dispute the debt formally. Utilizing the US Legal platform can simplify this process by providing templates and resources for your Delaware Notice of Harassment and Validation of Debt.

Filing a harassment complaint in Delaware involves gathering evidence, such as texts or messages that demonstrate the harassment. You can then submit your complaint to the appropriate local law enforcement agency or the Delaware Department of Justice. It’s important to include a detailed account of the incidents and any supporting documentation. For additional guidance, consider using the US Legal platform, which can assist you in drafting your Delaware Notice of Harassment.

To obtain a debt validation letter, you should first request it from the creditor or debt collector. This letter is essential for understanding the details of the debt and ensuring its validity. Under the Delaware Notice of Harassment and Validation of Debt, you have the right to ask for this information. If you need assistance, platforms like USLegalForms can help you create the necessary documents to formally request a debt validation letter.

When responding to a debt validation letter, start by reviewing the details provided in the letter. If you believe the debt is incorrect, you can dispute it in writing, requesting further verification from the collector. It's important to send your response within 30 days to ensure your rights are protected. For further assistance and useful templates, visit US Legal Forms, especially regarding the Delaware Notice of Harassment and Validation of Debt.

A debt validation notice must include essential details such as the amount owed, the name of the creditor, and the consumer's rights regarding debt verification. This notice also needs to inform you of your right to dispute the debt within 30 days. Ensuring that you receive all required information helps protect your rights as a consumer. If you need templates or guidance, the US Legal Forms platform can assist you with the Delaware Notice of Harassment and Validation of Debt.

In the United States, you generally cannot go to jail simply for owing a debt. However, failing to respond to court summons related to a debt can lead to serious consequences, including potential jail time for contempt. It is crucial to address any legal notices you receive regarding debt to avoid further complications. For more information and support, explore the options available through the US Legal Forms website, particularly concerning the Delaware Notice of Harassment and Validation of Debt.

A debt validation notice is sent to inform you of a debt that has been assigned or sold to a collector. This notice gives you the necessary details about the debt, including the amount owed and the creditor’s information. By sending this notice, the collector ensures compliance with the Fair Debt Collection Practices Act. If you have questions about your rights related to the Delaware Notice of Harassment and Validation of Debt, US Legal Forms can provide valuable resources and templates.

You received a debt validation letter because a creditor or debt collector is required to provide proof of the debt you owe. This letter serves as your formal notice, allowing you to verify the legitimacy of the debt. It's important to review this information carefully, as understanding your rights can help you manage your financial obligations appropriately. If you need assistance, consider using the US Legal Forms platform for guidance regarding the Delaware Notice of Harassment and Validation of Debt.