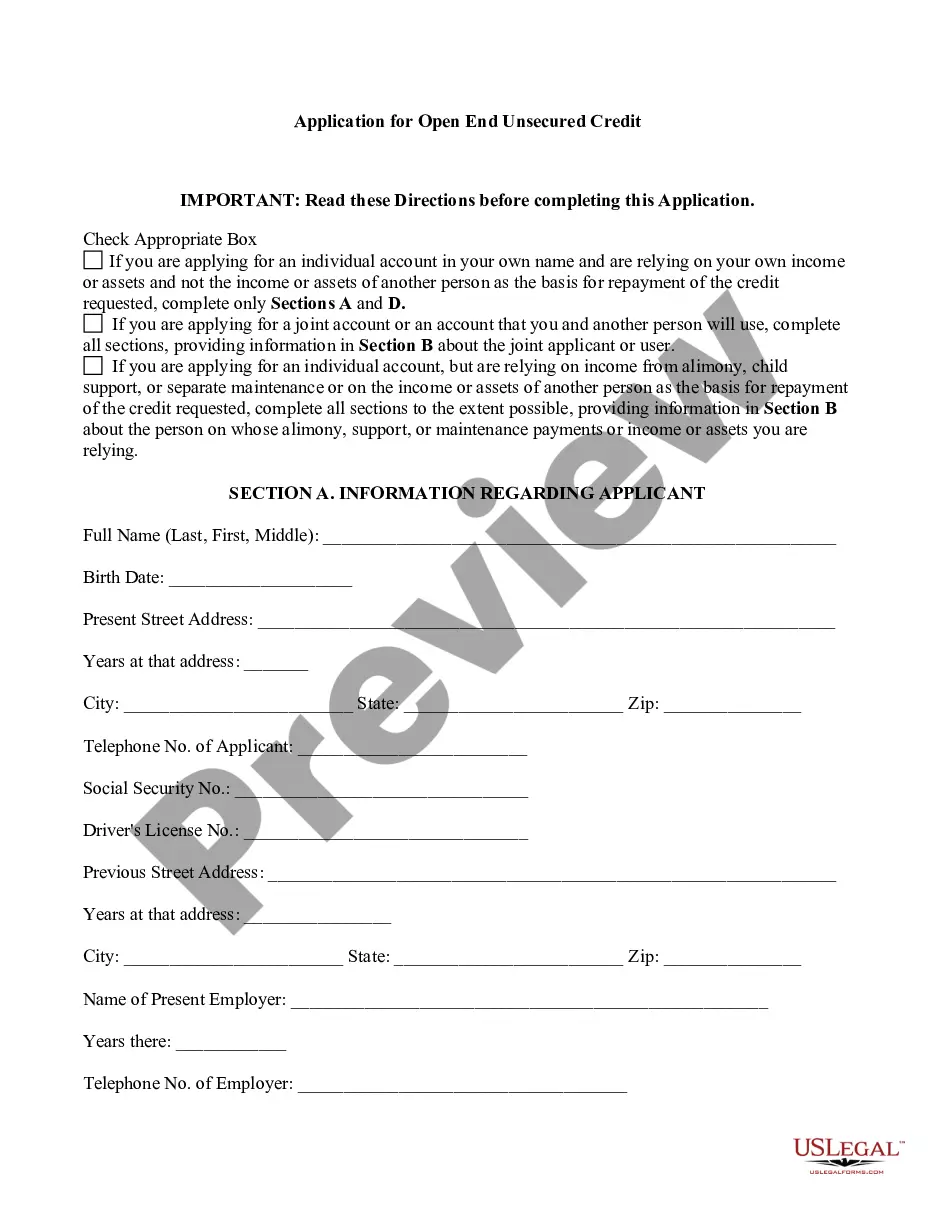

Connecticut Credit Card Application for Unsecured Open End Credit

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Credit Card Application For Unsecured Open End Credit?

US Legal Forms - among the greatest libraries of legitimate kinds in America - offers a wide array of legitimate record web templates you are able to obtain or print out. Making use of the web site, you can get a huge number of kinds for organization and specific functions, sorted by groups, says, or keywords.You can get the newest variations of kinds much like the Connecticut Credit Card Application for Unsecured Open End Credit within minutes.

If you already possess a subscription, log in and obtain Connecticut Credit Card Application for Unsecured Open End Credit in the US Legal Forms library. The Download option will appear on every kind you view. You get access to all formerly saved kinds within the My Forms tab of your bank account.

If you want to use US Legal Forms the first time, here are simple directions to help you get began:

- Ensure you have picked out the best kind for your personal city/state. Go through the Review option to review the form`s content. Look at the kind outline to ensure that you have chosen the proper kind.

- When the kind does not fit your demands, use the Research discipline towards the top of the monitor to find the one which does.

- When you are pleased with the form, validate your selection by clicking on the Buy now option. Then, choose the pricing plan you want and provide your qualifications to register for the bank account.

- Approach the financial transaction. Use your Visa or Mastercard or PayPal bank account to finish the financial transaction.

- Pick the file format and obtain the form on your system.

- Make changes. Fill up, change and print out and sign the saved Connecticut Credit Card Application for Unsecured Open End Credit.

Every template you added to your account lacks an expiration day and is also your own property permanently. So, in order to obtain or print out yet another duplicate, just proceed to the My Forms section and then click on the kind you will need.

Gain access to the Connecticut Credit Card Application for Unsecured Open End Credit with US Legal Forms, probably the most extensive library of legitimate record web templates. Use a huge number of expert and status-particular web templates that meet your company or specific demands and demands.

Form popularity

FAQ

Federal Regulation Z requires mortgage issuers, credit card companies, and other lenders to provide consumers with written disclosure of important credit terms. 1 The type of information that must be disclosed includes details about interest rates and how financing charges are calculated.

TILA disclosures include the number of payments, the monthly payment, late fees, whether a borrower can prepay the loan without penalty and other important terms. TILA disclosures is often provided as part of the loan contract, so the borrower may be given the entire contract for review when the TILA is requested.

To access money from a line of credit, you may: write a cheque drawn on your line of credit. use an automated teller machine ( ATM ) use telephone or online banking to pay a bill. use telephone or online banking to transfer money to your chequing account.

The TILA-RESPA rule consolidates four existing disclosures required under TILA and RESPA for closed-end credit transactions secured by real property into two forms: a Loan Estimate that must be delivered or placed in the mail no later than the third business day after receiving the consumer's application, and a Closing ...

The Connecticut Truth-In-Lending Act generally requires financial institutions and others to clearly and conspicuously disclose to consumers certain loan information (CGS § 36a-675 et seq.).

The Act was signed into law in May 2009, and the majority of its provisions became effective nine months after the passage of the law?in February 2010.

The Truth in Lending Act (and Regulation Z) explains which transactions are exempt from the disclosure requirements, including: loans primarily for business, commercial, agricultural, or organizational purposes. federal student loans.

Total of payments, Payment schedule, Prepayment/late payment penalties, If applicable to the transaction: (1) Total sales cost, (2) Demand feature, (3) Security interest, (4) Insurance, (5) Required deposit, and (6) Reference to contract.