Colorado Information Sheet - When are Entertainment Expenses Deductible and Reimbursable

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Information Sheet - When Are Entertainment Expenses Deductible And Reimbursable?

It is feasible to spend hours online searching for the legal documents template that fulfills the federal and state requirements you need.

US Legal Forms offers a vast array of legal documents which are examined by experts.

It is easy to acquire or print the Colorado Information Sheet - When are Entertainment Expenses Deductible and Reimbursable from the service.

If available, utilize the Review button to preview the document template as well. If you wish to find another version of the form, use the Search section to locate the template that satisfies your needs and requirements.

- If you already have a US Legal Forms account, you can Log In and press the Download button.

- After that, you can complete, modify, print, or sign the Colorado Information Sheet - When are Entertainment Expenses Deductible and Reimbursable.

- Every legal document template you purchase is yours indefinitely.

- To obtain another copy of the purchased form, visit the My documents tab and click on the corresponding button.

- If you are using the US Legal Forms site for the first time, follow the straightforward directives below.

- First, ensure you have selected the correct document template for the area/town of your choice.

- Review the document information to confirm you have selected the appropriate form.

Form popularity

FAQ

Yes, some entertainment expenses are not tax deductible. According to the guidelines laid out in the Colorado Information Sheet - When are Entertainment Expenses Deductible and Reimbursable, expenses that do not directly contribute to business operations or do not have a clear business purpose cannot be claimed. It is essential to keep accurate records and be aware of the types of entertainment that are eligible for deductions. This awareness can help you maximize your tax benefits responsibly.

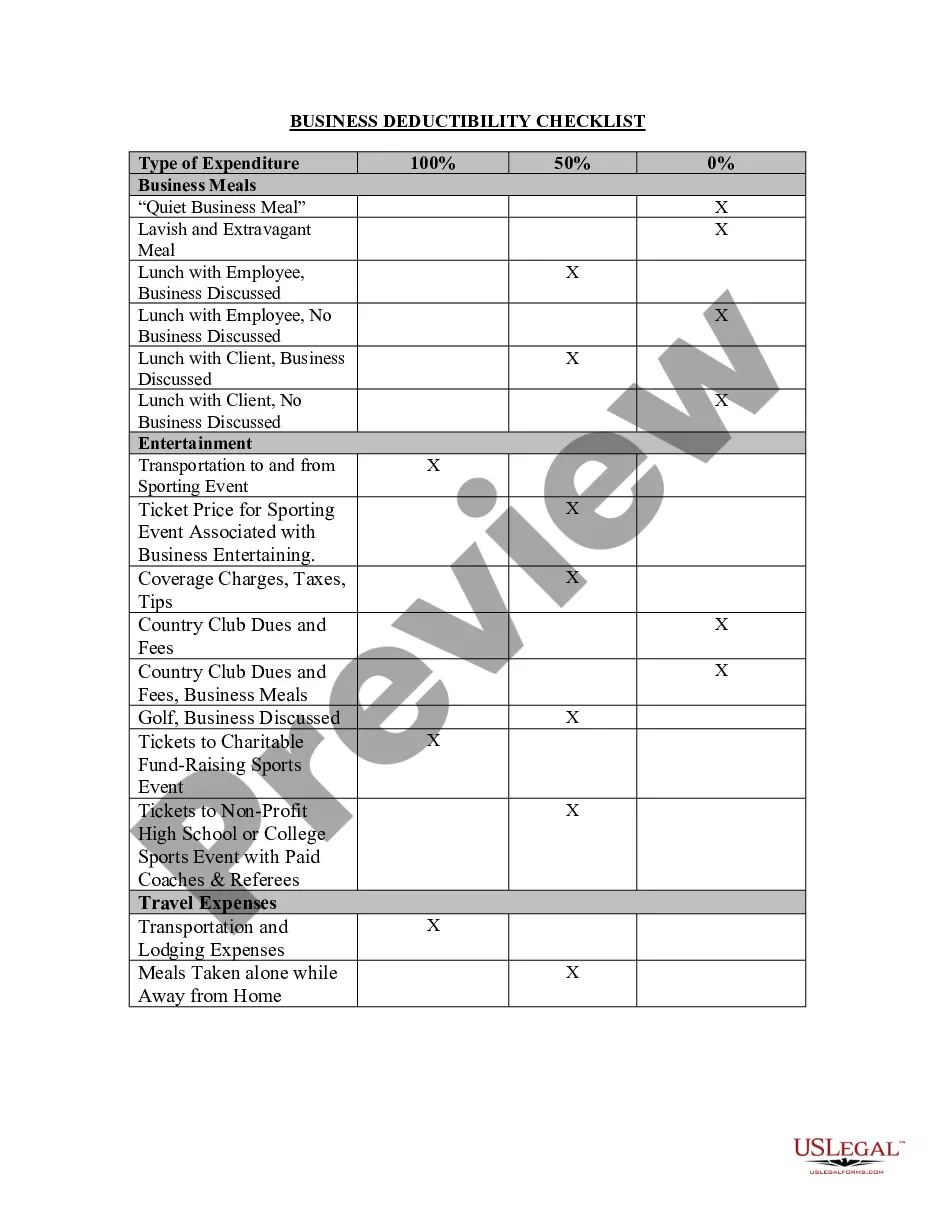

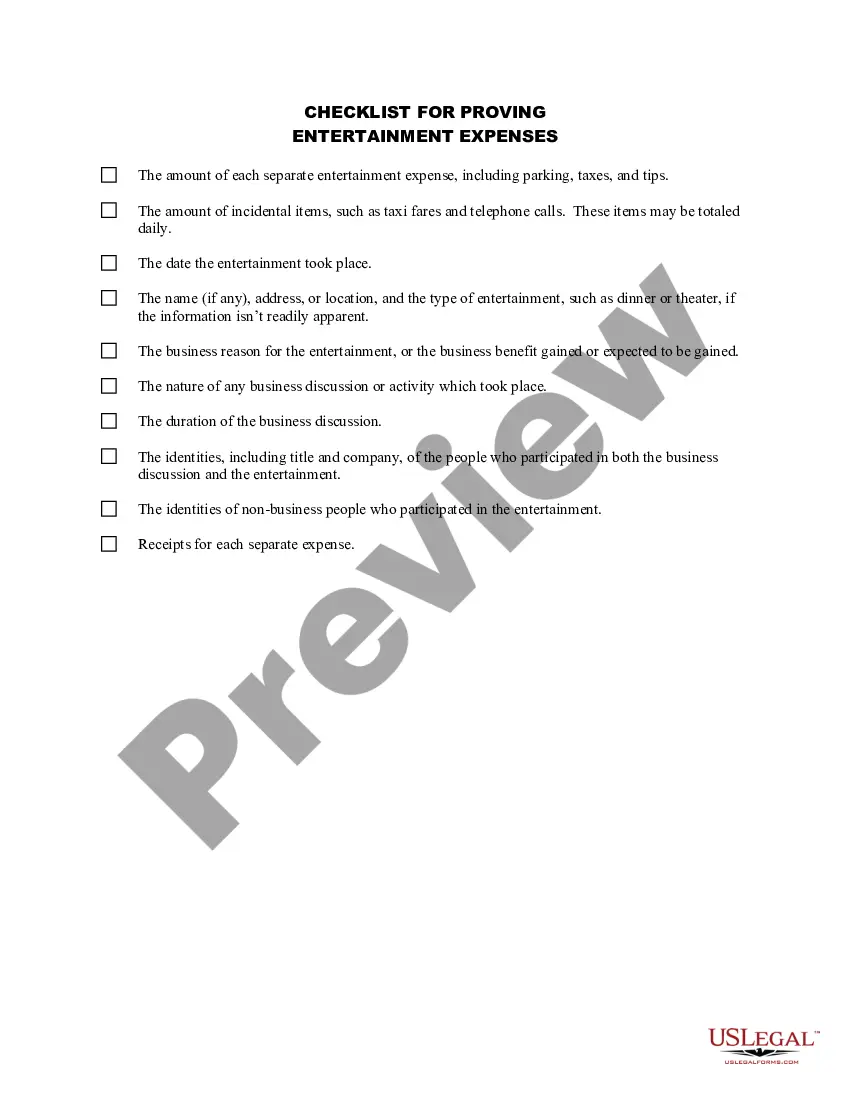

The IRS on Wednesday issued final regulations (T.D. 9925) implementing provisions of the law known as the Tax Cuts and Jobs Act (TCJA), P.L. 115-97, that disallow a business deduction for most entertainment expenses.

Your business can deduct 100% of the cost of food, beverages, and entertainment that is made available to the general public (for example, free snacks at a car dealership or free food and music provided at a promotional event open to the public).

As part of the 2018 tax reform created by the Tax Cuts and Jobs Act (TCJA), Congress made several significant changes to the deductions for meals, entertainment, and employee fringe benefits, including making business entertainment expenses entirely nondeductible and reducing the deduction for most meals to 50%.

The new tax act establishes additional limitations on the deductibility of certain business meals and entertainment expenses. Under the act, entertainment expenses incurred or paid after Dec. 31, 2017 are nondeductible unless they fall under the specific exceptions in Code Section 274(e).

2022 meals and entertainment deduction As part of the Consolidated Appropriations Act signed into law on December 27, 2020, the deductibility of meals is changing. Food and beverages will be 100% deductible if purchased from a restaurant in 2021 and 2022. Entertaining clients (concert tickets, golf games, etc.)

Businesses will be permitted to fully deduct business meals that would normally be 50% deductible. Although this change will not affect your 2020 tax return, the savings will offer a 100% deduction in 2021 and 2022 for food and beverages provided by a restaurant.

The deduction for unreimbursed non-entertainment-related business meals is generally subject to a 50% limitation. You generally can't deduct meal expenses unless you (or your employee) are present at the furnishing of the food or beverages and such expense is not lavish or extravagant under the circumstances.

For 2018 and beyond, the Tax Cuts and Jobs Act (TCJA) permanently eliminated deductions for most business-related entertainment expenses.

Entertainment expenses, like a sporting event or tickets to a show, are still non-deductible.