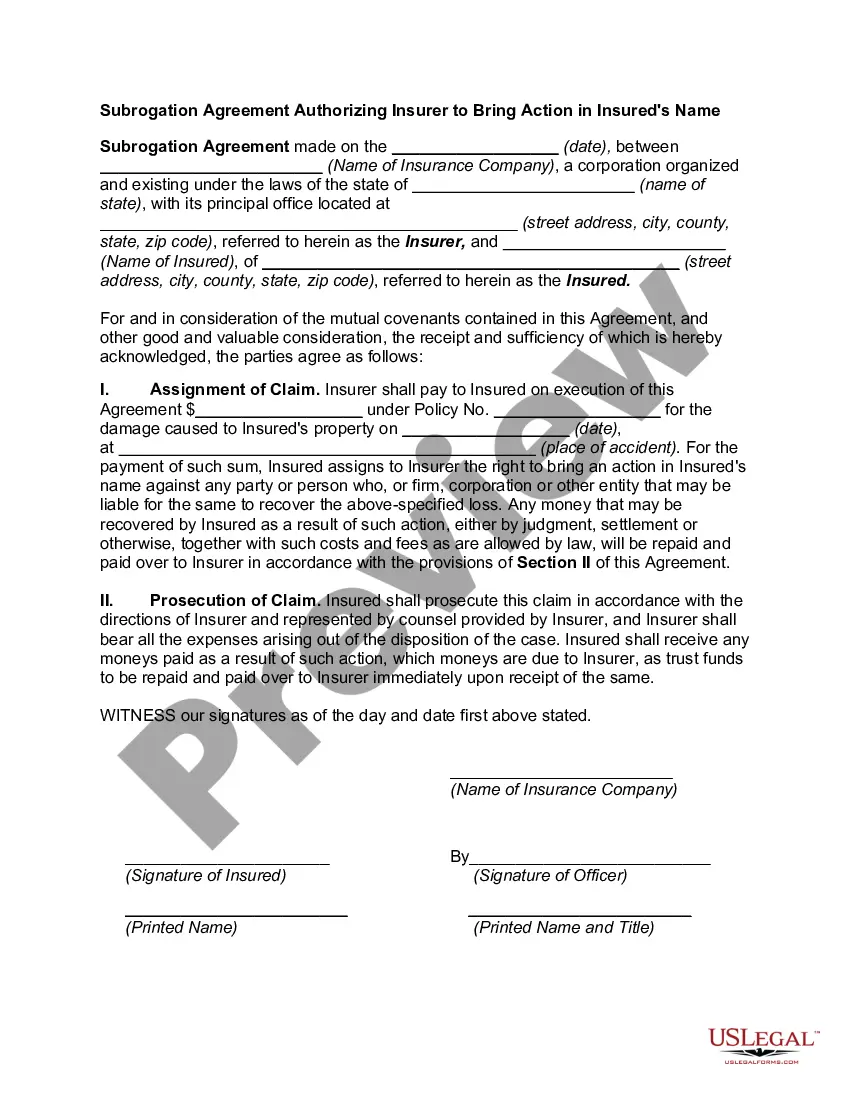

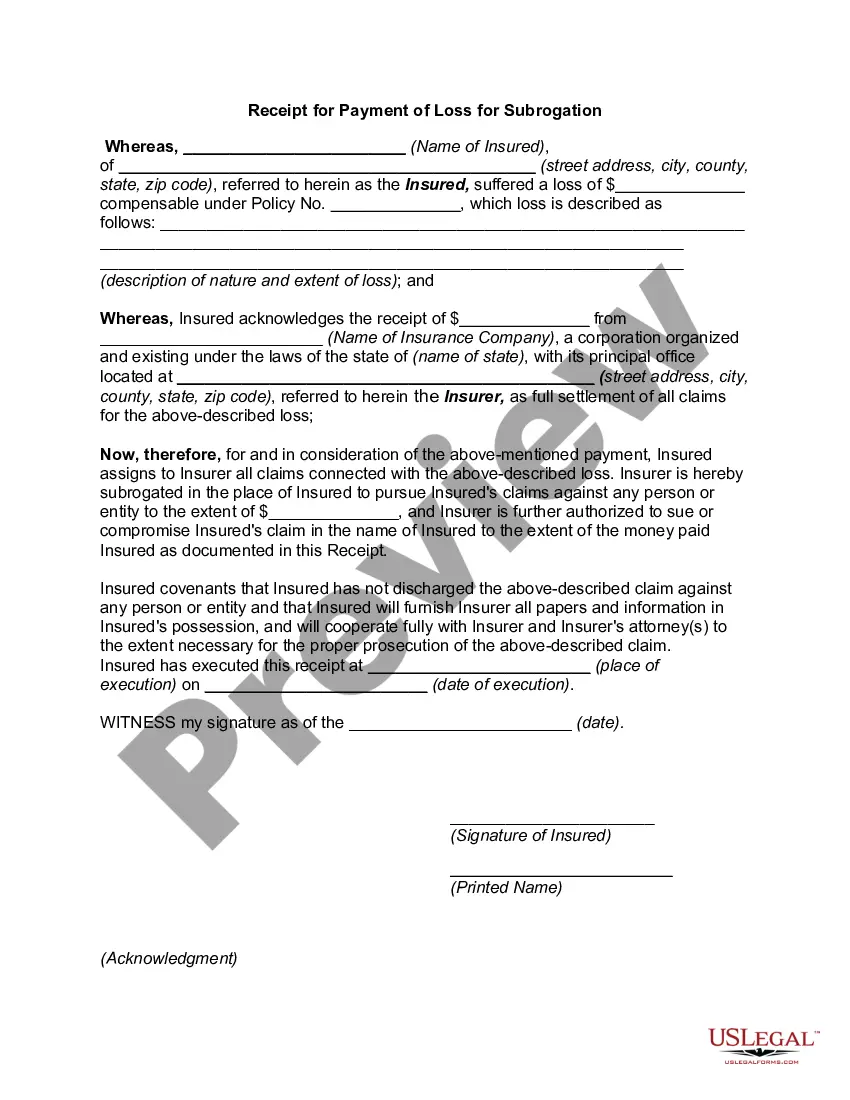

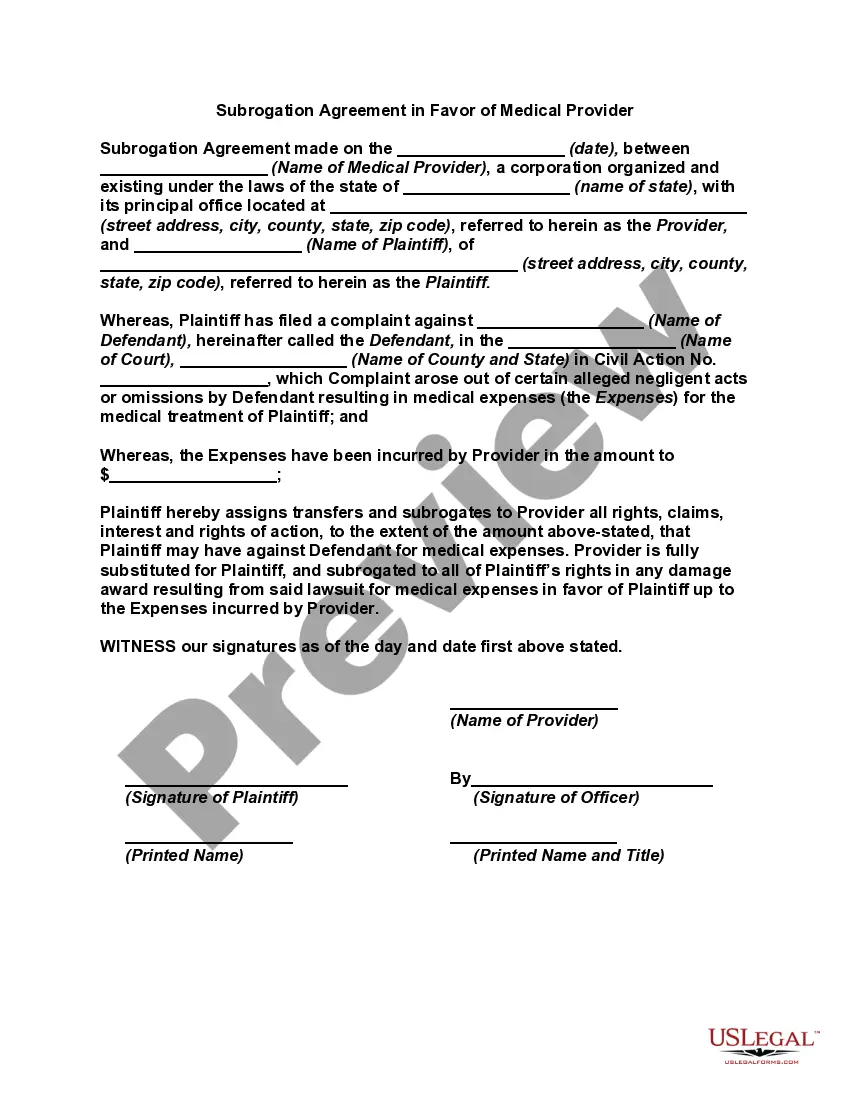

Colorado Subrogation Agreement between Insurer and Insured

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Subrogation Agreement Between Insurer And Insured?

Choosing the best legal file format could be a battle. Naturally, there are tons of templates available on the Internet, but how do you get the legal form you require? Make use of the US Legal Forms internet site. The service provides thousands of templates, like the Colorado Subrogation Agreement between Insurer and Insured, which you can use for organization and private requirements. Each of the forms are checked by specialists and meet up with federal and state requirements.

When you are currently registered, log in to your profile and click on the Down load switch to have the Colorado Subrogation Agreement between Insurer and Insured. Make use of your profile to check throughout the legal forms you have purchased in the past. Check out the My Forms tab of your profile and obtain yet another backup of your file you require.

When you are a fresh user of US Legal Forms, listed below are simple guidelines for you to comply with:

- First, ensure you have selected the proper form for the town/area. You are able to examine the shape using the Review switch and browse the shape information to make certain it will be the right one for you.

- If the form fails to meet up with your expectations, make use of the Seach industry to get the right form.

- When you are certain that the shape would work, click the Get now switch to have the form.

- Select the costs plan you need and enter in the needed information and facts. Make your profile and buy your order with your PayPal profile or charge card.

- Choose the submit structure and down load the legal file format to your product.

- Complete, modify and print and sign the obtained Colorado Subrogation Agreement between Insurer and Insured.

US Legal Forms will be the biggest collection of legal forms that you can discover numerous file templates. Make use of the service to down load professionally-made paperwork that comply with express requirements.

Form popularity

FAQ

Insurance companies argue that the additional insured endorsement is designed to cover only that vicarious liability. If the general contractor was independently negligent, insurance companies argue that the liability for that independent negligence should not be covered by the additional insured endorsement.

An additional insured extends liability insurance coverage beyond the named insured to include other individuals or groups. An additional insured endorsement protects the additional insured under the named insurer's policy allowing them to file a claim if sued.

An insurance company may not subrogate against its own insured or a co-insured. However, when a party claiming to be a co-insured is merely a loss payee to which no liability coverage is afforded, subrogation is permissible.

At Hiscox, the additional named insured and the named insured both have full rights under the policy. The named insured is the one who is responsible for paying the premiums, and who can cancel the policy. The additional named insured doesn't have those obligations to the insurer.

An insurer may attempt to subrogate against an additional insured for completed operations injuries caused by the insured if the additional insured endorsement provides coverage only for ongoing operations injuries.

Colorado law does not require victims to pay subrogation claims if their settlement doesn't make them whole, which means restoring them to the financial position they enjoyed before the accident.

"Subrogation," or "subro" for short, refers to the right your insurance company holds under your policy ? after they've paid a covered claim ? to request reimbursement from the at-fault party. This reimbursement often comes from the at-fault party's insurance company.