California Installments Fixed Rate Promissory Note Secured by Commercial Real Estate

What this document covers

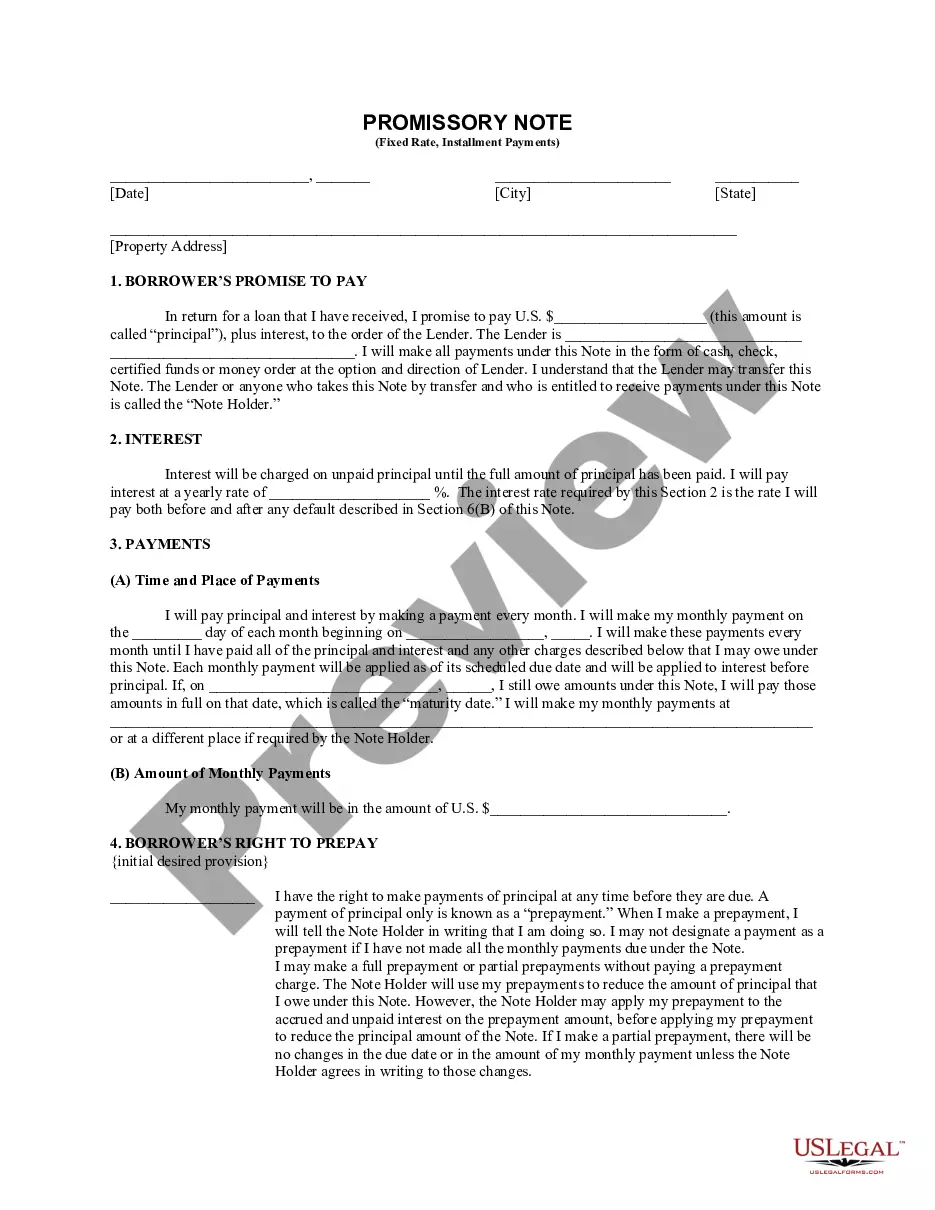

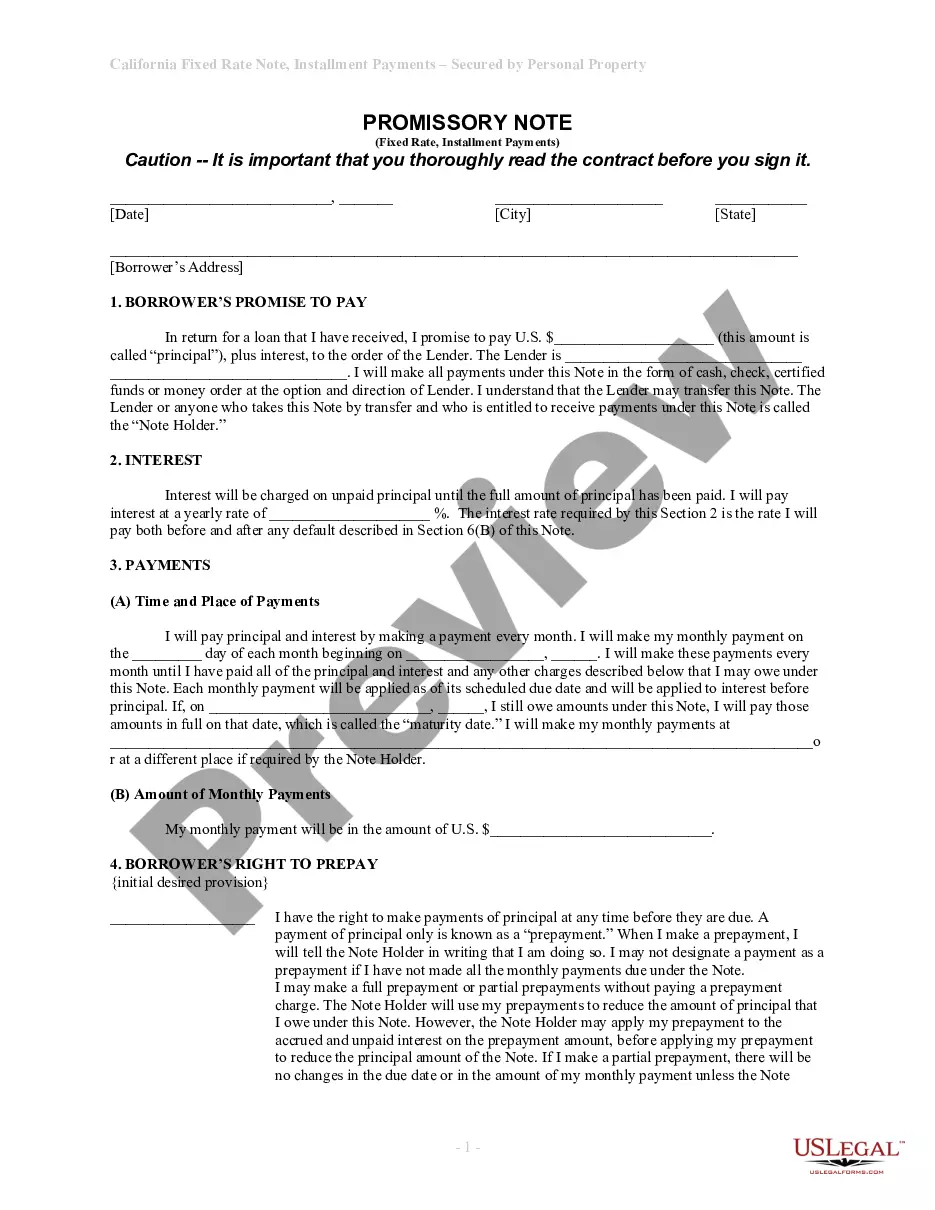

The California Installments Fixed Rate Promissory Note Secured by Commercial Real Estate is a legal document that outlines a borrower's promise to repay a loan secured by commercial property. This document is specifically designed for situations where the loan amount is repaid through fixed monthly installments, distinguishing it from other types of promissory notes that may not have a secured backing. In addition to this note, a separate deed of trust or mortgage is typically required to protect the lender's interests.

What’s included in this form

- Borrower's Promise to Pay: Details the borrower's commitment to repay the principal amount and interest to the lender.

- Interest Rate: Specifies the annual interest rate on the unpaid principal and its application during any defaults.

- Payment Schedule: Outlines the frequency and amount of monthly payments, including the maturity date.

- Prepayment Rights: Describes the borrower's ability to make early payments on the principal without penalties, unless specified otherwise.

- Default Terms: Outlines conditions for default and possible consequences, including late charges and lender notifications.

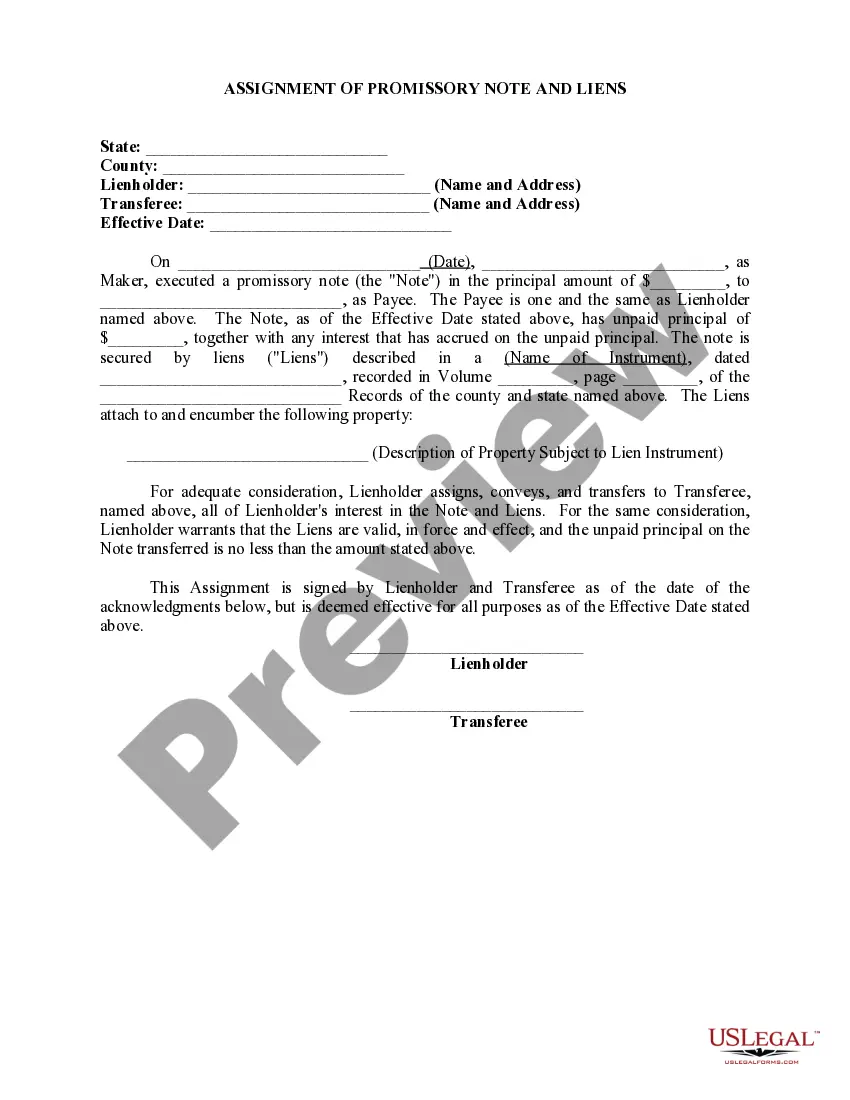

- Security Instrument: Explains the additional legal protections for the lender through a mortgage or deed of trust.

When to use this form

This form is necessary when a borrower seeks a loan secured by commercial property. It is commonly used in commercial real estate transactions where the borrower needs to formalize repayment terms with a fixed interest rate and scheduled payments. Typical scenarios include purchasing commercial real estate or refinancing an existing commercial loan where property serves as collateral.

Who should use this form

- Business owners seeking financing secured by their commercial real estate.

- Real estate investors looking to formalize loan agreements for property transactions.

- Individuals or entities borrowing funds that require a clear and enforceable repayment structure.

- Lenders providing loans against commercial properties who need a legal framework to outline repayment terms.

How to prepare this document

- Identify the parties by entering the borrower's and lender's names and addresses at the top of the document.

- Specify the loan details, including the principal amount and annual interest rate in the respective fields.

- Fill in the payment schedule, including the start date, frequency of payments, and maturity date.

- Document any prepayment rights or penalties as applicable to the loan agreement.

- Sign and date the form to make it legally binding, ensuring all parties receive a copy.

Notarization guidance

This form does not typically require notarization unless specified by local law. It is important to check local regulations to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to specify the exact principal amount or interest rate, which can lead to disputes later.

- Not clearly defining prepayment terms, which may incur unexpected charges.

- Overlooking the need for a separate security instrument, leading to inadequate protection for the lender.

- Incomplete signatures or dates, making the document potentially unenforceable.

Why use this form online

- Convenience of completing the form at any time, from anywhere.

- Editability allows users to customize the document for specific needs without legal assistance.

- Reliability of using templates drafted by licensed attorneys, ensuring compliance with applicable laws.

- This promissory note is enforceable in court, provided all terms are clear and adhered to by both parties.

- It is important to comply with California's lending laws and regulations regarding interest rates and loan charges.

- Default on payments can lead to serious legal consequences, including foreclosure on the secured property.

Summary of main points

- The California Installments Fixed Rate Promissory Note is vital for securing loans against commercial property.

- Clear terms regarding interest, repayment schedules, and defaults protect both borrower and lender.

- Proper completion and understanding of this form are essential to avoid legal disputes.

Looking for another form?

Form popularity

FAQ

To ensure a promissory note is valid in California, it must include essential components, such as a defined repayment plan and the signatures of the involved parties. It should also be executed voluntarily and meet all legal restrictions. When you create a California Installments Fixed Rate Promissory Note Secured by Commercial Real Estate, including these elements helps ensure its validity.

A promissory note may be deemed invalid due to ambiguous terms, absence of borrower identification, or failure to meet state laws. If it does not clearly outline the rights and responsibilities of the involved parties, the note may not stand in legal proceedings. Thus, using a California Installments Fixed Rate Promissory Note Secured by Commercial Real Estate can help ensure all details are clearly defined.

Several factors can void a promissory note, including the presence of duress, fraud, or a lack of capacity from the borrower. If any party influences the agreement improperly, the note may be considered void. To avoid such issues, it's wise to use a California Installments Fixed Rate Promissory Note Secured by Commercial Real Estate that adheres to legal standards.

Yes, promissory notes are generally enforceable in California as long as they comply with state laws. When structured correctly, a California Installments Fixed Rate Promissory Note Secured by Commercial Real Estate can provide lenders with the ability to collect the owed amount. It is crucial to ensure that all requirements for enforceability are met to protect your interests.

A promissory note can become invalid in California for several reasons, such as lacking essential details or not being signed by the borrower. If it fails to meet the statutory requirements, it may not hold up in court. Moreover, a California Installments Fixed Rate Promissory Note Secured by Commercial Real Estate can lose its validity if it contains fraudulent information.

Yes, a promissory note can indeed be secured by real property. This type of arrangement often involves a California Installments Fixed Rate Promissory Note Secured by Commercial Real Estate. Such notes provide a layer of security for lenders, ensuring they have a claim on the property if the borrower defaults.

To secure a promissory note with real property, you typically create a deed of trust or mortgage agreement that pledges the property as collateral. This process involves drafting legal documentation that outlines the terms and conditions binding both parties. With a California Installments Fixed Rate Promissory Note Secured by Commercial Real Estate, this process safeguards the lender's interests while providing the borrower access to funds. Utilizing platforms like uslegalforms can simplify this documentation process, ensuring compliance with legal standards.

The security for a promissory note generally comes from collateral, which can be real estate or other valuable assets. For a California Installments Fixed Rate Promissory Note Secured by Commercial Real Estate, the commercial property acts as this security. This enables lenders to reclaim their investment if the borrower fails to meet repayment obligations and enhances the overall appeal for securing funds.

The document that secures the promissory note to the real property is typically called a deed of trust or a mortgage agreement. In the context of a California Installments Fixed Rate Promissory Note Secured by Commercial Real Estate, this document outlines the terms and conditions under which the property is held as security. By having this documentation in place, both parties understand their rights and obligations clearly, which fosters a smoother transaction.

Yes, promissory notes can indeed be backed by collateral. In fact, a California Installments Fixed Rate Promissory Note Secured by Commercial Real Estate uses the property itself as collateral. This arrangement offers added security for lenders, as they can claim the property if the borrower defaults. This structure not only enhances trust but also informs potential lenders about the stability of their investment.