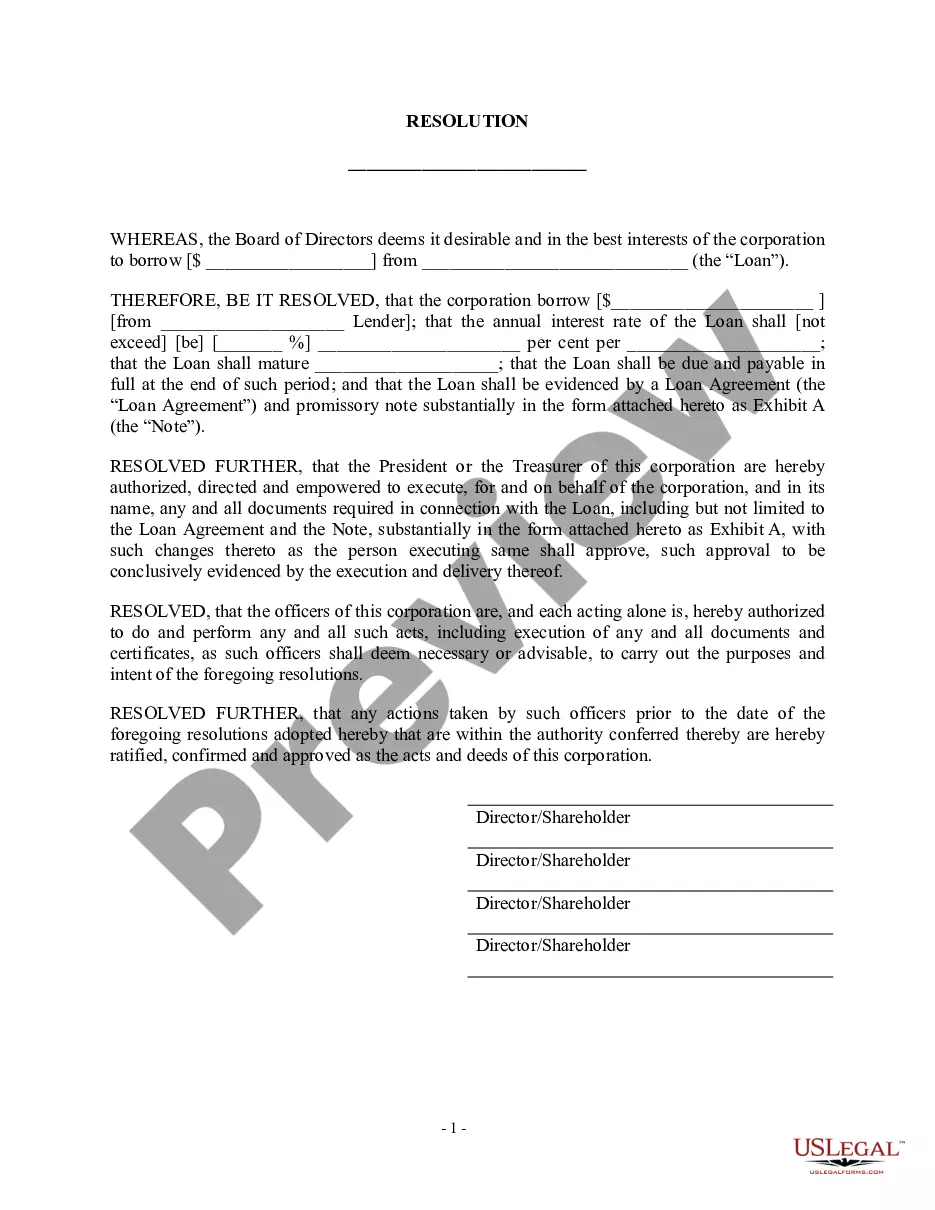

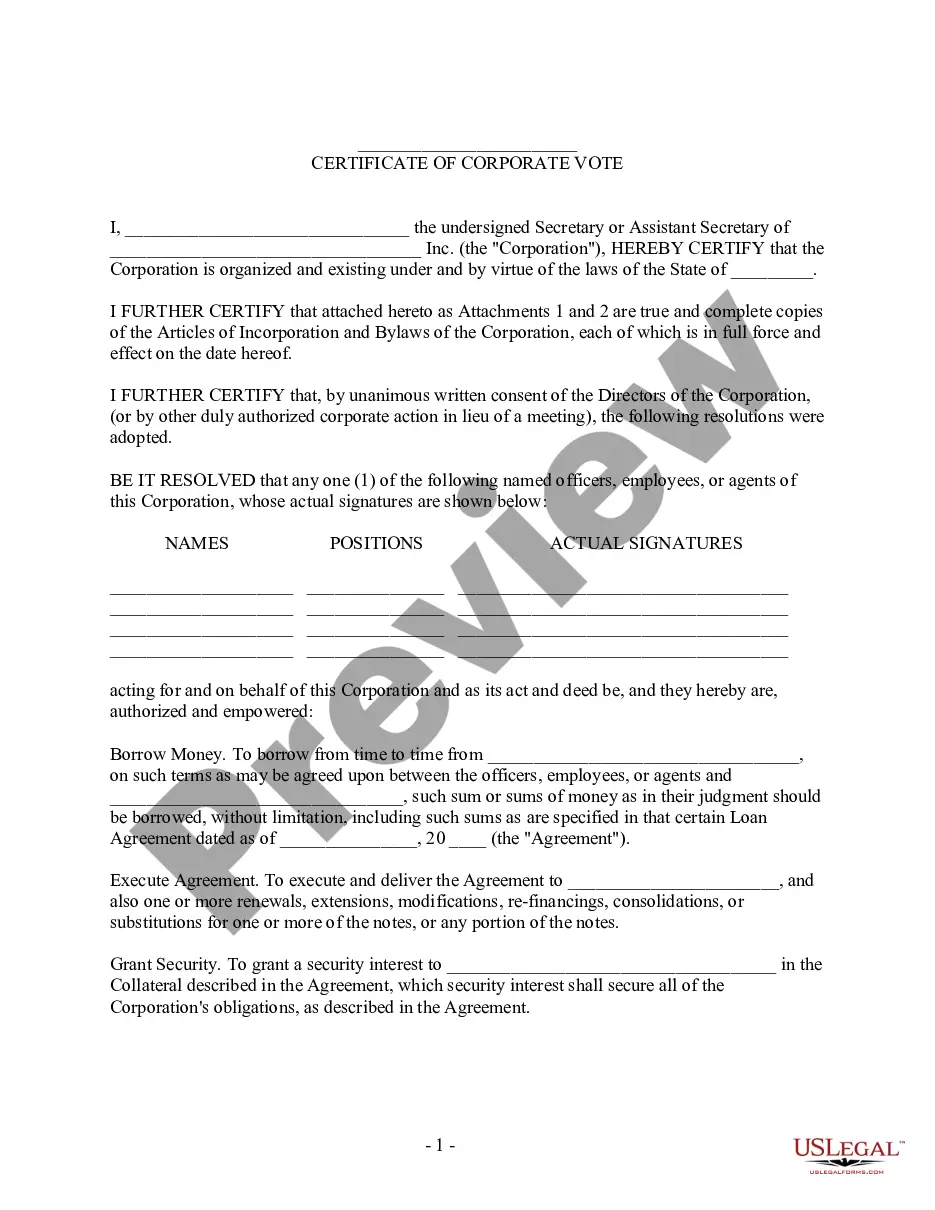

Form with which the directors of a corporation may authorize an officer or representative to take necessary steps to issue a promissory note on behalf of the corporation.

Alabama Borrow Money on Promissory Note - Resolution Form - Corporate Resolutions

Category:

State:

Multi-State

Control #:

US-0062-CR

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Borrow Money On Promissory Note - Resolution Form - Corporate Resolutions?

Are you presently in a location where you frequently require documentation for both professional and personal purposes almost every business day.

There are numerous legal document templates accessible online, but finding reliable ones can be challenging.

US Legal Forms offers thousands of form templates, including the Alabama Borrow Money on Promissory Note - Resolution Form - Corporate Resolutions, which are designed to comply with state and federal regulations.

Once you acquire the appropriate form, click Buy now.

Select the payment plan you prefer, fill out the necessary information to create your account, and pay for your order using your PayPal or Visa/Mastercard.

- If you are already familiar with the US Legal Forms website and have an account, just Log In.

- After that, you can download the Alabama Borrow Money on Promissory Note - Resolution Form - Corporate Resolutions template.

- If you do not possess an account but wish to start using US Legal Forms, follow these steps.

- Find the form you need and ensure it corresponds to the correct city/area.

- Utilize the Review button to examine the form.

- Read the description to confirm you have selected the right form.

- If the form isn’t what you’re looking for, use the Search field to find a form that meets your needs.

Form popularity

FAQ

What Is a Promissory Note? A promissory note is a debt instrument that contains a written promise by one party (the note's issuer or maker) to pay another party (the note's payee) a definite sum of money, either on-demand or at a specified future date.

Unlike a promissory note, a loan agreement imposes obligations on both parties, which is why both the borrower and lender must sign the agreement. A loan agreement should state what purpose the loan is used for, and whether the borrower must provide compensation if the lender suffers loss.

Promissory notes may also be referred to as an IOU, a loan agreement, or just a note. It's a legal lending document that says the borrower promises to repay to the lender a certain amount of money in a certain time frame. This kind of document is legally enforceable and creates a legal obligation to repay the loan.

2. They both usually cover the consequences of non-payment. Neither a promissory note nor a loan agreement would be complete without including certain information about what should be done in case the borrower doesn't pay the lender back.

Generally, as long as the promissory note contains legally acceptable interest rates, the signatures of the two contracted parties, and are within the applicable Statute of Limitations, they can be upheld in a court of law.

Often there is no legal requirement that a promise to pay be evidenced in a promissory note, nor any prohibition from including it in a loan or credit agreement. Although promissory notes are sometimes thought to be negotiable instruments, this typically is not the case.

Homebuyers usually think of the mortgage as the contract they're signing with the lender to borrow money to buy a house. But the promissory note is the document that contains the promise to repay the amount borrowed. The purpose of the mortgage is to provide security for the loan that's evidenced by a promissory note.

A promissory note represents an underlying debt owed by one person to another. The signed promissory note is not the debt itself, but evidence the debt exists. The buyer, called the debtor or payor, signs the note and delivers it to the lender or carryback seller, called the creditor.

While a promissory note, a loan agreement, and a mortgage are evidence of a debt owed from the borrower to the lender, the loan agreement has more extensive definitions and clauses than the promissory note. Only the borrower signs the promissory note, whereas both the lender and the borrower sign a loan agreement.

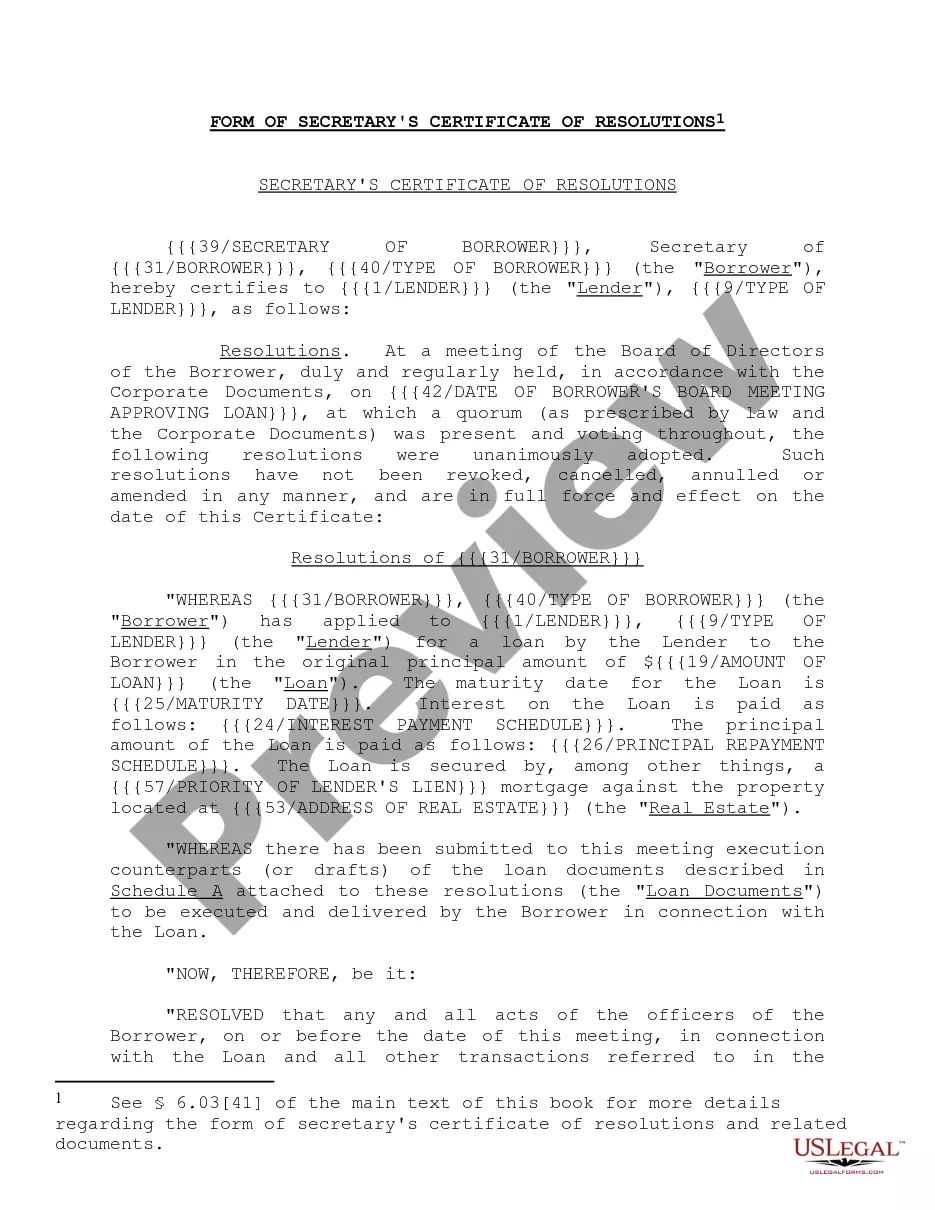

A corporate resolution that authorizes borrowing on a line of credit is often referred to a borrowing resolution. This resolution indicates that the members (LLC) or Board of Directors (Corporation) have held a meeting and conducted a vote allowing the company to borrow a specific loan amount.