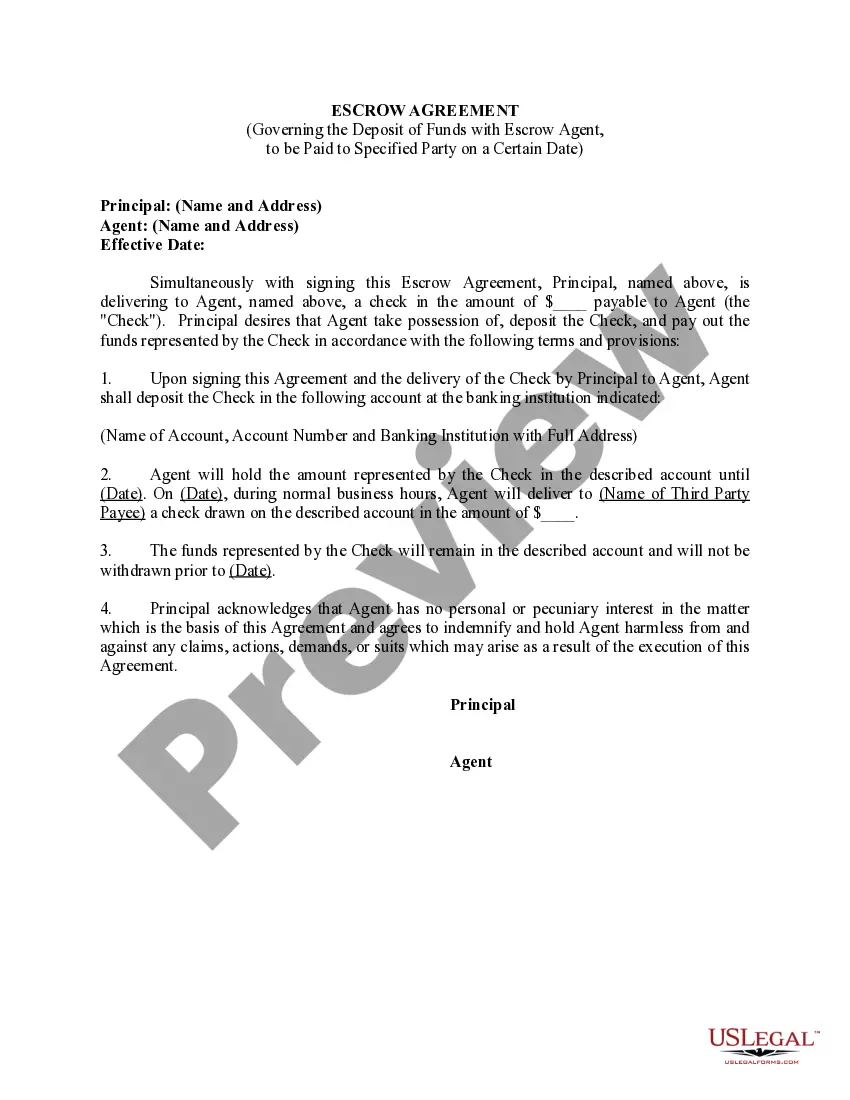

Escrow Agreement Between For Repairs After Closing

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Escrow Agreement Between Depositor, Inc., And Multimedia Licensor, Inc.?

Individuals often connect legal documentation with something intricate that only an expert can manage.

In a way, this is accurate, as creating an Escrow Agreement For Repairs After Closing demands considerable knowledge of relevant criteria, including state and local regulations.

However, with US Legal Forms, the process has become simpler: pre-made legal documents for any personal and business situation tailored to state laws are gathered in a single online repository and are now accessible to all.

Print your document or upload it to an online editor for quicker completion. All templates in our collection are reusable: once purchased, they remain stored in your profile. You can access them anytime you need via the My documents tab. Discover all the benefits of using the US Legal Forms platform. Subscribe today!

- US Legal Forms offers more than 85,000 contemporary forms categorized by state and purpose, so searching for an Escrow Agreement For Repairs After Closing or any other specific template takes just a few minutes.

- Previously registered users with an active subscription must Log In to their account and click Download to acquire the document.

- New users to the platform will first need to create an account and subscribe before they can save any paperwork.

- Here is a step-by-step guide on how to access the Escrow Agreement For Repairs After Closing.

- Review the page content carefully to ensure it fulfills your requirements.

- Read the form description or examine it through the Preview option.

- Look for another example using the Search field above if the previous one is not suitable.

- Click Buy Now when you identify the appropriate Escrow Agreement For Repairs After Closing.

- Select a subscription plan that meets your needs and budget.

- Register for an account or Log In to continue to the payment page.

- Pay for your subscription via PayPal or with your credit card.

- Choose the format for your document and click Download.

Form popularity

FAQ

An escrow holdback agreement is when money is set aside at the closing of a home to complete repairs. Generally, this is done at the seller's expense, though not always. Money is held in an escrow account until the repairs are completed.

Can a mortgage loan be denied after closing? Though it's rare, a mortgage can be denied after the borrower signs the closing papers. For example, in some states, the bank can fund the loan after the borrower closes. It's not unheard of that before the funds are transferred, it could fall apart, Rueth said.

In its simplest terms, a repair escrow is an account established to pay for any necessary repairs on a home after the closing date. For example, let's say that you need to sell your home, but the roof leaks.

Federal law gives borrowers what is known as the "right of rescission." This means that borrowers after signing the closing papers for a home equity loan or refinance have three days to back out of that deal.

A closing statement is an accounting, in writing, prepared at the close of escrow which sets forth the charges and credits of your account.