609 Letter For Debt Collectors

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Notice Of Violation Of Fair Debt Act - Letter To The Federal Trade Commission?

- If you're an existing user, log in to your account and navigate to your dashboard. Confirm your subscription is active to access the form.

- In the library, check the preview and description of the 609 letter template. Ensure it meets your specific needs and aligns with local requirements.

- If necessary, use the Search tab to locate any additional forms. When you find the correct one, proceed to the next step.

- Purchase the document by clicking the Buy Now button. Choose your preferred subscription plan, and create an account to unlock full access.

- Complete the transaction by entering your payment information, either via credit card or PayPal.

- Download the completed 609 letter and save it to your device. You can also find it later in the My Forms section.

By utilizing US Legal Forms, you gain access to a vast library of over 85,000 legal documents, surpassing competitors in variety and affordability.

With expert assistance available for form completion, you can ensure that your 609 letter is precise and tailored to your situation. Start streamlining your legal processes today!

Form popularity

FAQ

The 623 dispute method involves notifying creditors directly about inaccuracies in the information they report to agencies. This method requires borrowers to send a formal letter, pointing out the inaccuracies and requesting corrections. By combining the 623 dispute method with a 609 letter for debt collectors, you enhance your chances of achieving accurate credit reporting.

The primary difference between a 609 and a 604 dispute letter lies in their purposes. A 609 letter for debt collectors focuses on validation of debts, while a 604 letter typically addresses issues related to the consumer report. Knowing these distinctions can help you decide which letter to use based on your specific situation.

A 623 refers to a specific part of the Fair Credit Reporting Act that governs how creditors should handle disputes about reported information. It establishes the procedure for responding to consumer claims regarding inaccuracies. Utilizing the information from Section 623 can enhance the effectiveness of your 609 letter for debt collectors when addressing errors on your credit report.

Section 623 of the Fair Credit Reporting Act imposes responsibilities on creditors regarding the accuracy of credit reporting. This section requires creditors to investigate and respond to consumer disputes promptly. By understanding this section, you can effectively leverage the 609 letter for debt collectors to ensure fair treatment in your credit dealings.

A 623 dispute letter is used to challenge the accuracy of information provided by creditors to credit reporting agencies. This letter refers to Section 623 of the Fair Credit Reporting Act, which outlines how creditors must respond to disputes. When you employ a 609 letter for debt collectors, this method can complement your efforts by targeting inaccuracies at the source.

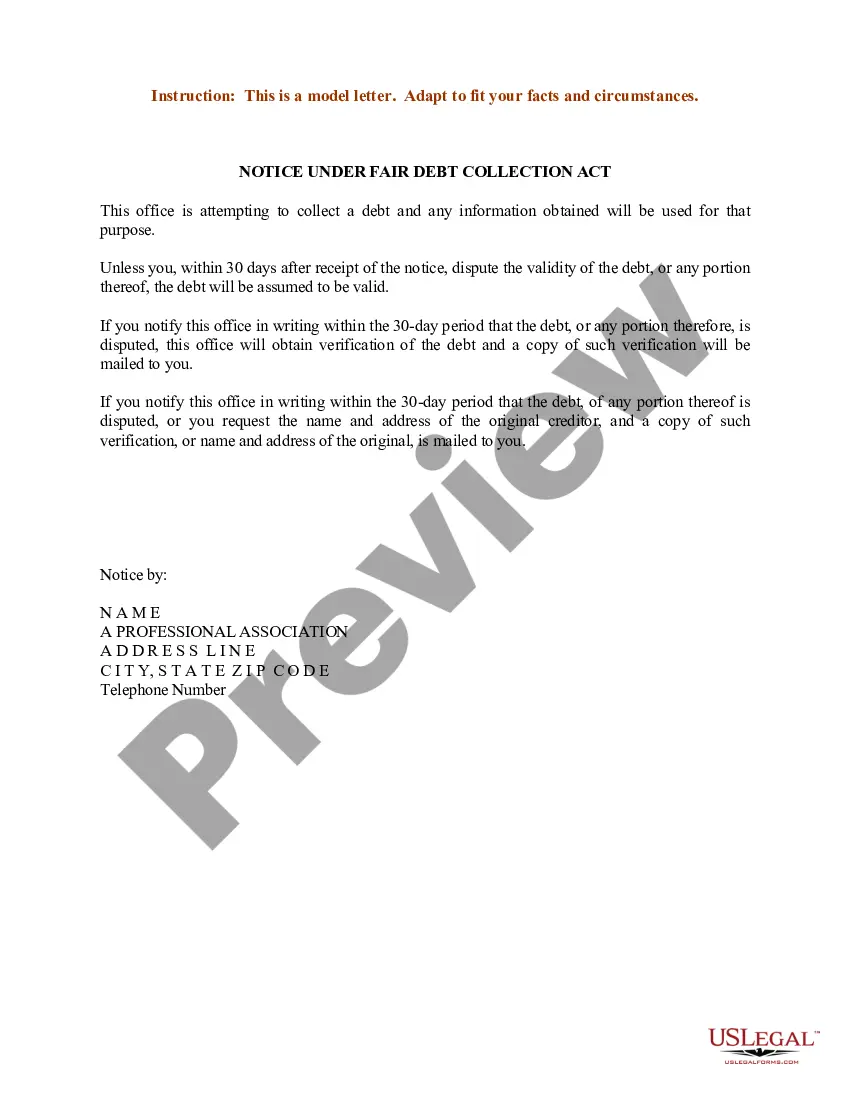

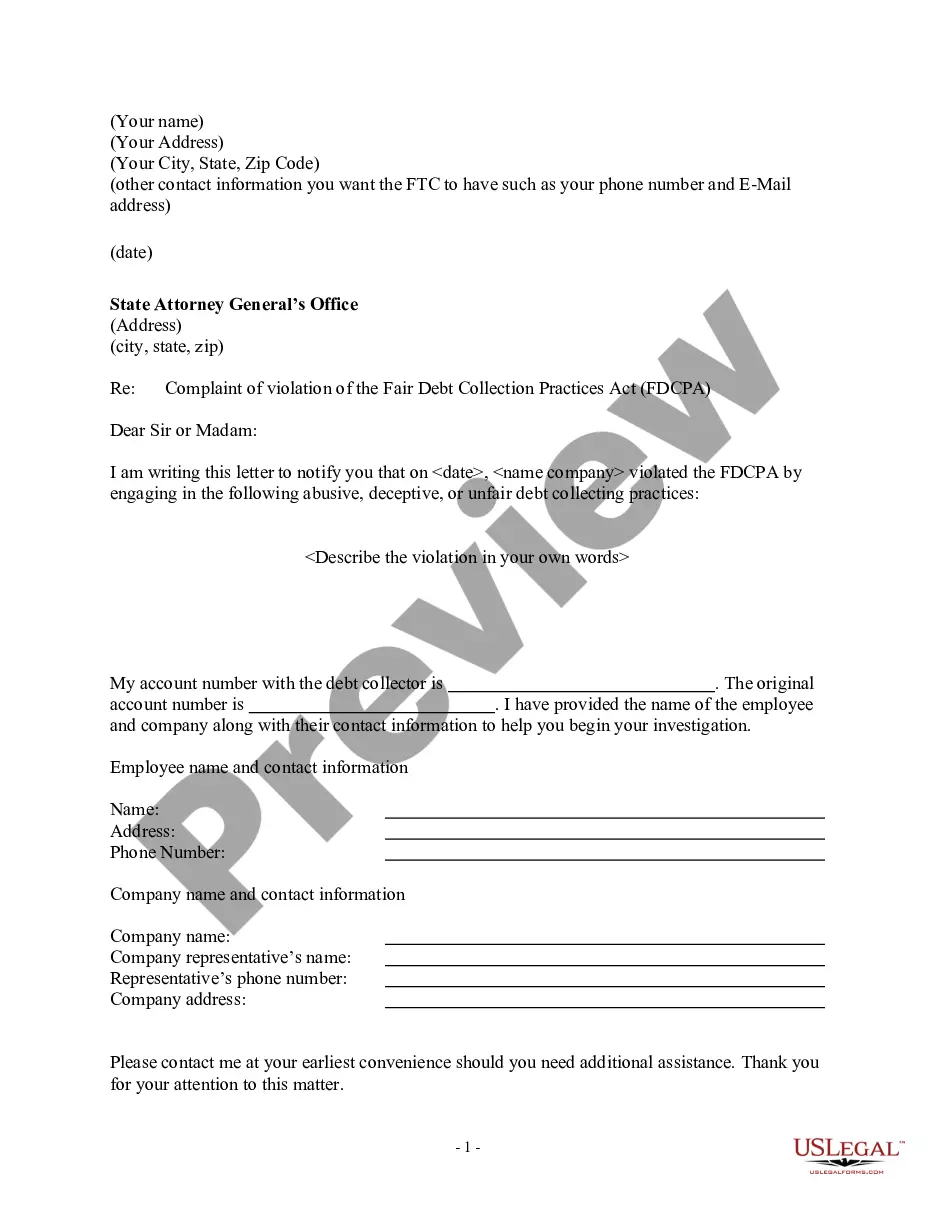

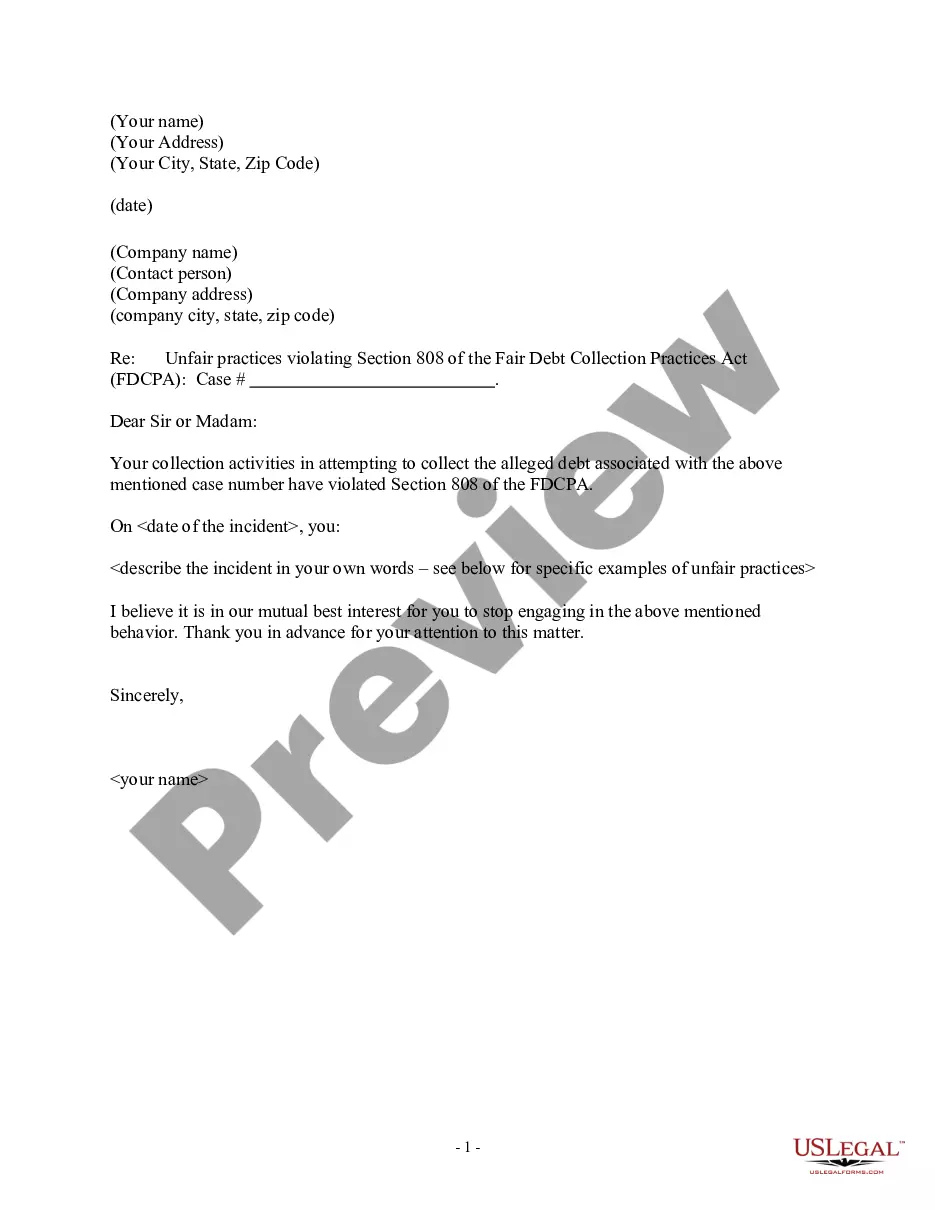

A 609 letter for debt collectors is designed to help individuals dispute inaccurate information on their credit reports. It allows you to request the creditor to provide evidence that they own the debt. If the collector cannot validate the debt, they must remove it from your credit report, making this letter an effective tool in your debt management strategy.

Collection dispute letters, including the 609 letter for debt collectors, can help you challenge inaccuracies in your credit report. If you clearly outline your concerns and include any supporting evidence, collectors must respond or verify the debt. Responding promptly to disputes can lead to credit score improvements if inaccuracies are removed. It’s crucial to keep records of your correspondence.

Yes, sending dispute letters can be effective when dealing with debt collectors. A well-crafted 609 letter for debt collectors can prompt them to investigate the disputed information. When you assert your rights and provide necessary documentation, it increases your chances of achieving a positive outcome. Always include accurate details to support your case.

No, a 609 letter for debt collectors does not need to be notarized. It is typically acceptable to send this letter without notarization. Just ensure that you provide clear identification and all relevant information. This way, the debt collector can verify your request efficiently.

When disputing a collection, it is crucial to refer to the 609 letter for debt collectors as a guide. Clearly state that you are challenging the validity of the debt and require full verification. Additionally, remind the collector that you expect a written response according to fair debt collection practices. This sets a professional tone and protects your rights.