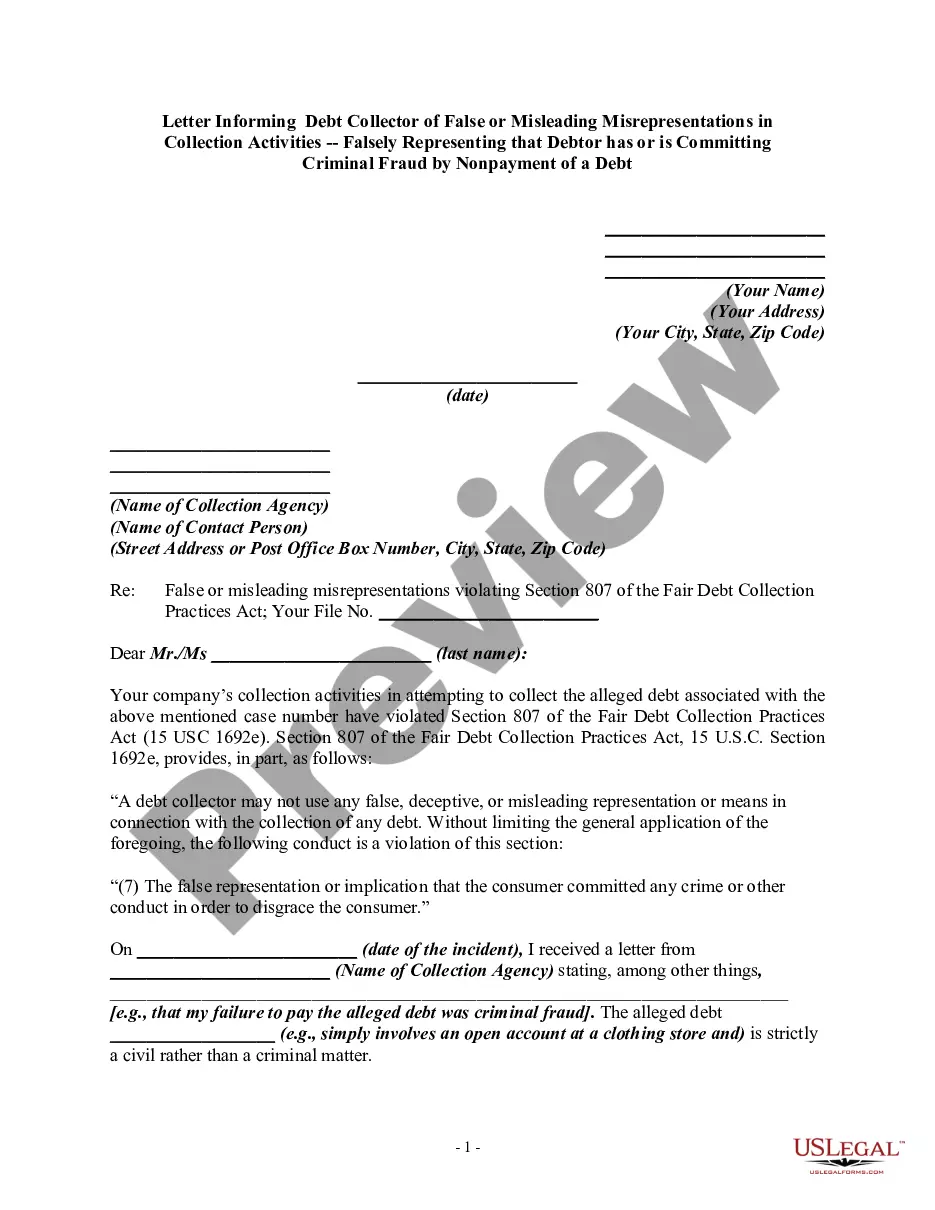

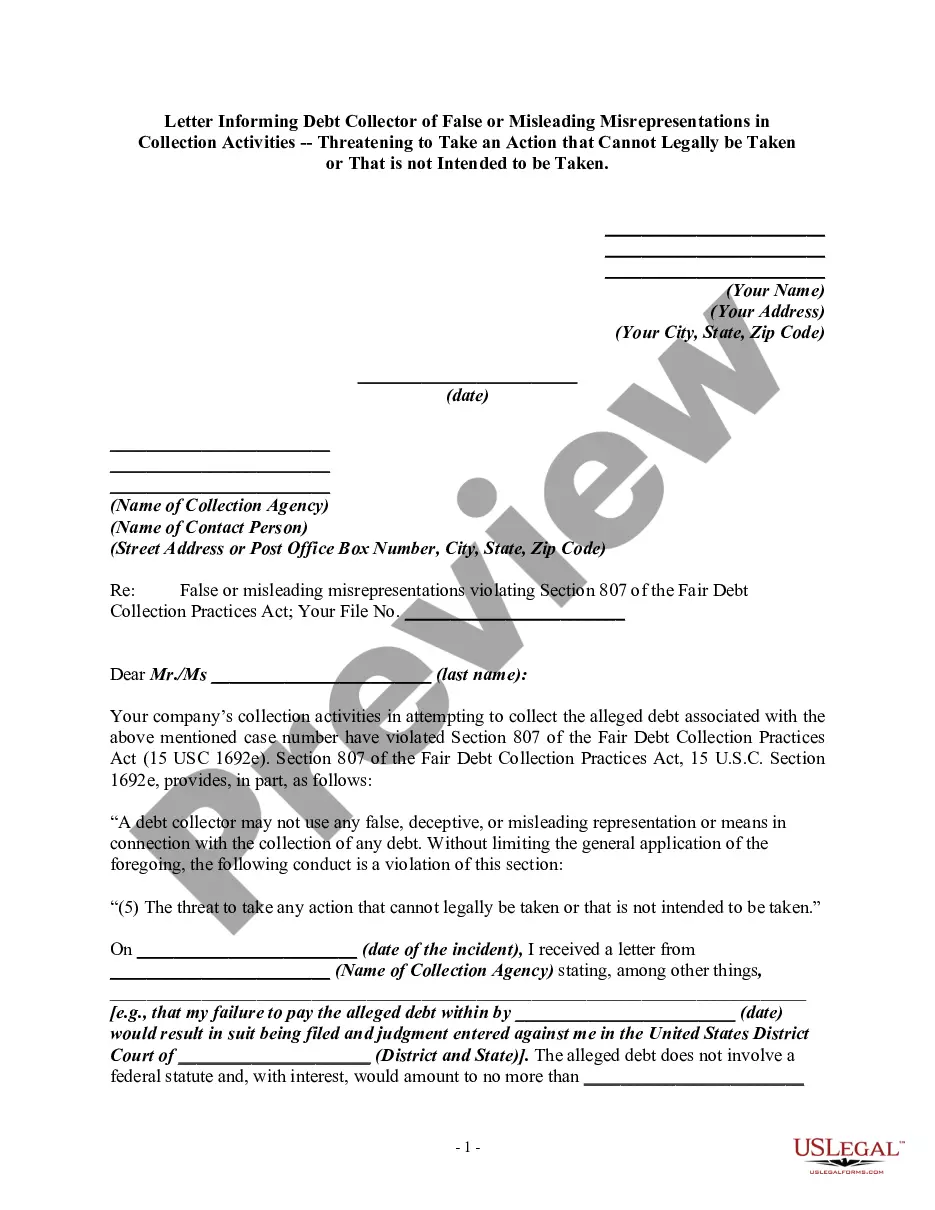

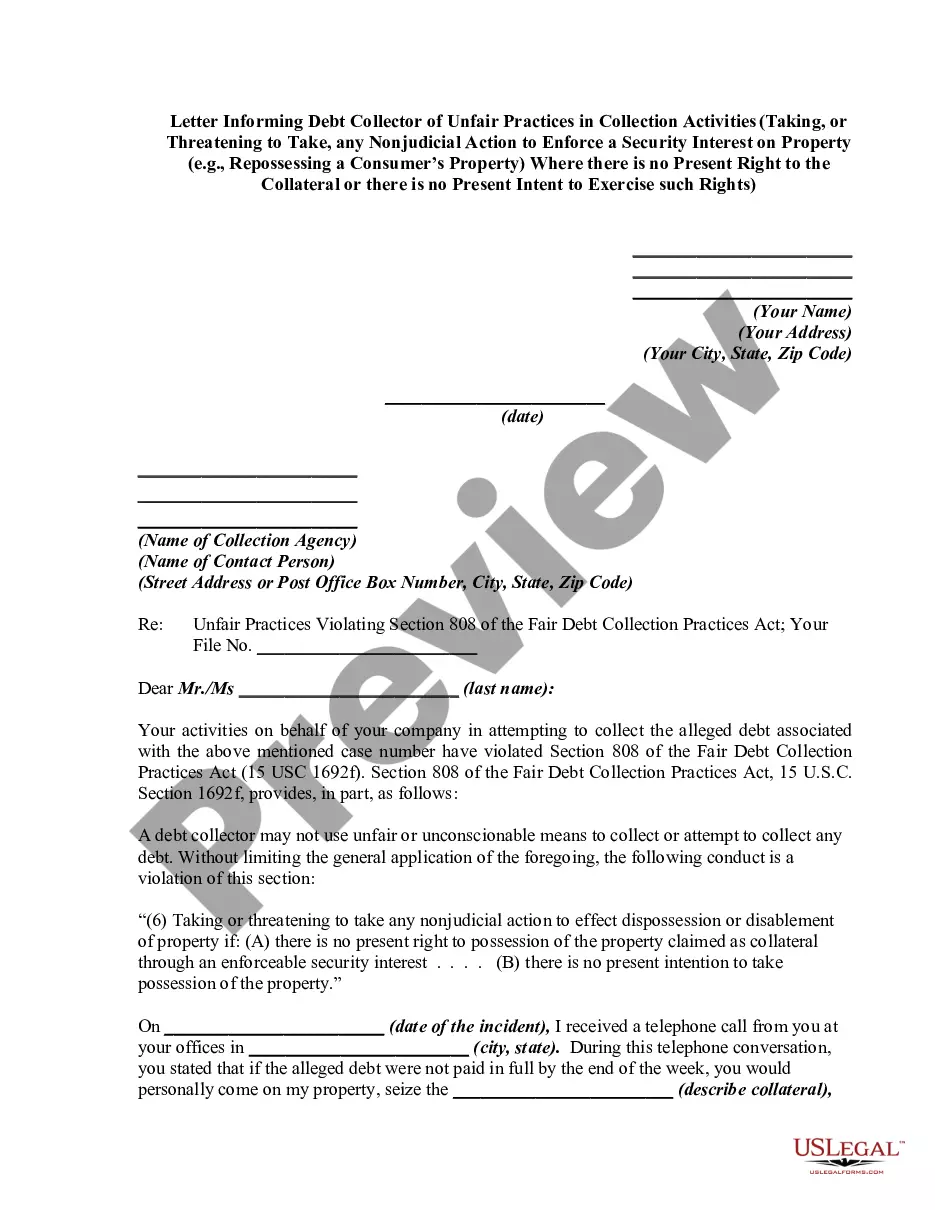

Collector Harassment Involving Force

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Letter Informing Debt Collector Of Harassment Or Abuse In Collection Activities Involving Threats To Use Violence Or Other Criminal Means To Harm The Physical Person, Reputation, And/or Property Of The Debtor?

Locating a reliable source for the most up-to-date and pertinent legal templates is a significant part of managing bureaucracy. Selecting the appropriate legal documents requires precision and carefulness, which is why it is essential to obtain samples of Collector Harassment Involving Force exclusively from trustworthy providers, such as US Legal Forms. An incorrect template will squander your time and prolong the issue you are facing. With US Legal Forms, you can have peace of mind. You can access and verify all the details regarding the document’s applicability and significance for your circumstances and in your jurisdiction.

Follow the outlined steps to complete your Collector Harassment Involving Force.

Once you have the document saved on your device, you can modify it using the editor or print it out and fill it in by hand. Eliminate the complications that come with your legal paperwork. Discover the extensive US Legal Forms library where you can find legal templates, assess their relevance to your case, and download them right away.

- Utilize the catalog navigation or search bar to find your template.

- Check the document’s details to ensure it meets the standards of your state and locality.

- View the form preview, if available, to confirm the template is the one you need.

- Continue your search and seek the appropriate document if the Collector Harassment Involving Force does not meet your requirements.

- Once you are certain about the form’s applicability, download it.

- If you are a registered user, click Log in to verify and access your selected templates in My documents.

- If you have not created an account yet, click Buy now to acquire the form.

- Select the pricing option that suits your needs.

- Proceed to the registration to complete your transaction.

- Finalize your order by choosing a payment method (credit card or PayPal).

- Select the file format for downloading Collector Harassment Involving Force.

Form popularity

FAQ

You can sue a debt collector for harassment under the Fair Debt Collection Practices Act, and the amount can vary. Generally, you may seek damages of up to $1,000, plus any actual damages incurred, such as lost wages or emotional distress. Legal fees can also be recovered if you win your case. If you are facing severe collector harassment involving force, consulting a legal expert can help clarify your potential compensation.

If a debt collector is harassing you, first understand your rights under the Fair Debt Collection Practices Act. Document every instance of harassment and gather evidence, such as call recordings or written communication. You should then send a cease-and-desist letter to the collector. If the harassment persists, seek legal advice to discuss your situation, especially if you are experiencing collector harassment involving force.

The 7 7 7 rule is a guideline suggesting that collectors should wait seven days after sending a debt notice before contacting you again. This rule helps ensure that you have adequate time to respond or address the debt. Understanding this rule can empower you against unwanted interruptions and support your rights against collector harassment involving force. If you feel overwhelmed, platforms like uslegalforms can assist you in managing these communications.

When a collection agency harasses you, start by documenting every interaction. Keep notes of dates, times, and the content of the conversations. Next, inform the agency in writing that you do not wish to be contacted further. If the harassment continues, consider reaching out to a legal professional who specializes in collector harassment involving force to explore your options.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

Hear this out loud PauseYou should dispute a debt if you believe you don't owe it or the information and amount is incorrect. While you can submit your dispute at any time, sending it in writing within 30 days of receiving a validation notice, which can be your initial communication with the debt collector.

Hear this out loud PauseThe first thing to do is to write the debt collector a letter telling them to stop calling you. You can use the sample letter language here. Under the FDCPA, they must follow your written request for no contact. If they do not, you can report them to the Federal Trade Commission (FTC).

Hear this out loud PauseIf you are struggling with debt and debt collectors, Farmer & Morris Law, PLLC can help. As soon as you use the 11-word phrase ?please cease and desist all calls and contact with me immediately? to stop the harassment, call us for a free consultation about what you can do to resolve your debt problems for good.

Hear this out loud PauseThis is where we get our "7-in-7" concept. You can attempt to contact a consumer about 1 debt 7 times in 7 days. And it's the "1 debt" that's key here. Phone numbers do not matter; how many debts your agency has for the consumer does.