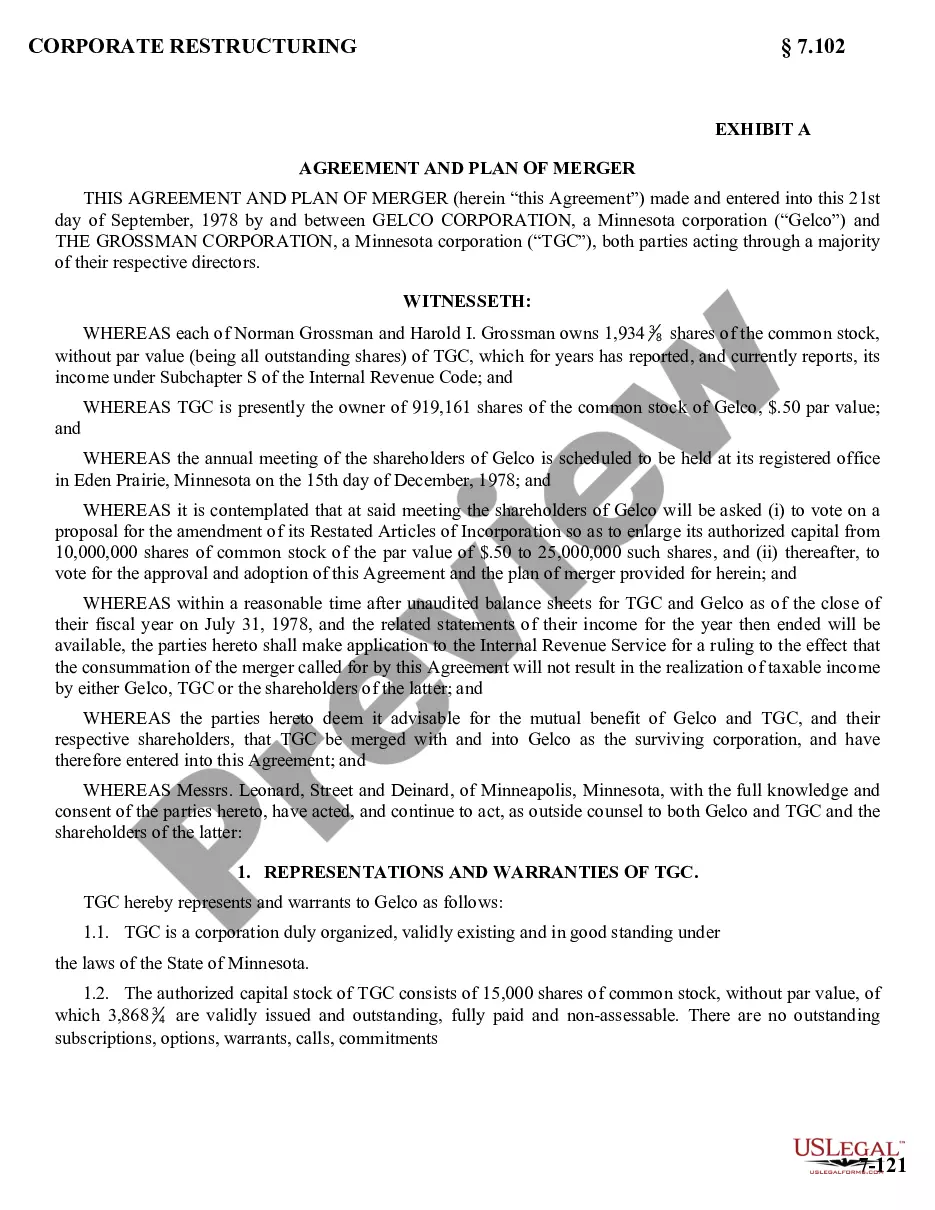

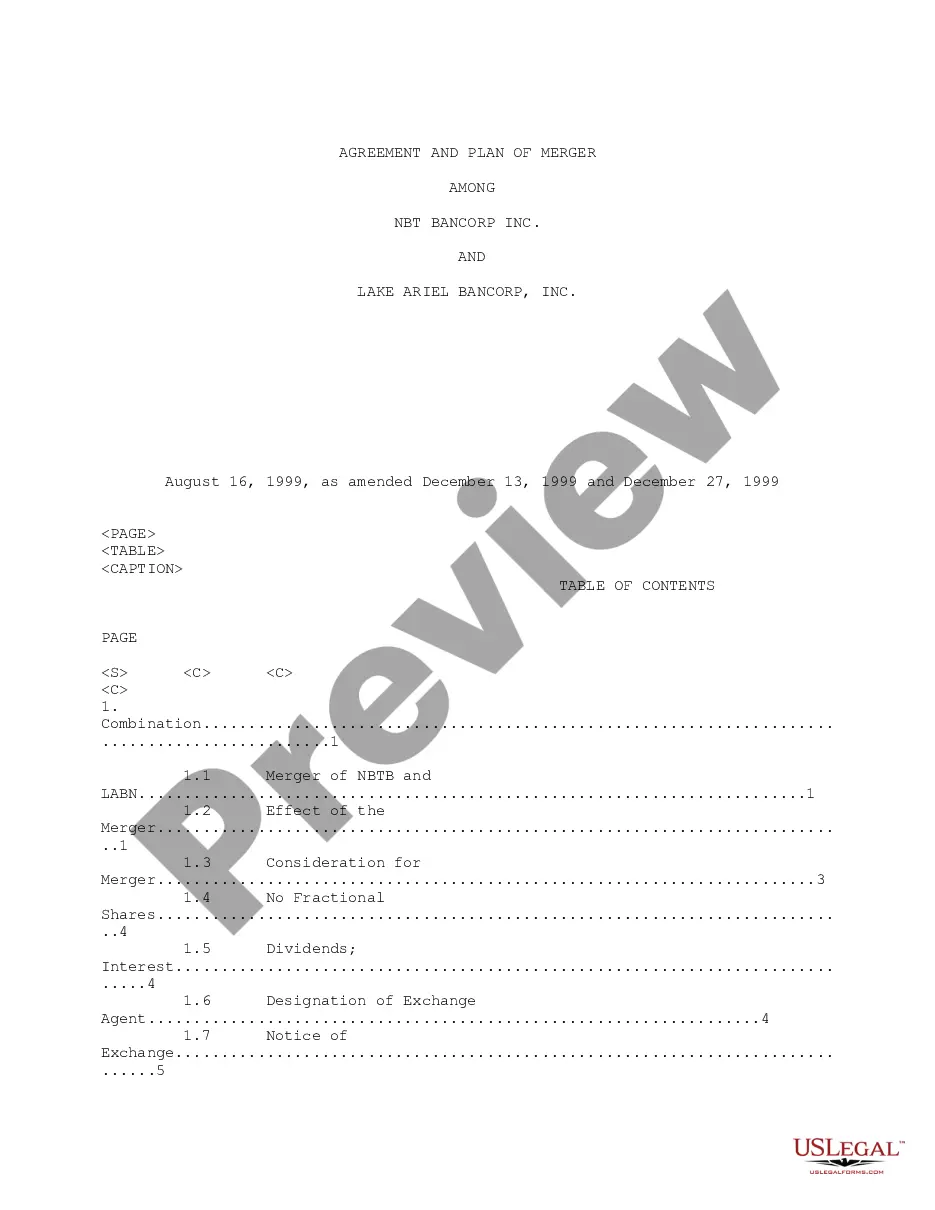

Share Merger Stock For Stock

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Proposed Merger With The Grossman Corporation?

Discovering a reliable source for the most up-to-date and pertinent legal templates is a significant part of navigating bureaucracy.

Locating the appropriate legal documents requires precision and careful consideration, which is why it is essential to obtain Share Merger Stock For Stock samples solely from reputable providers, such as US Legal Forms. An incorrect template can squander your time and hinder your progress.

After obtaining the form on your device, you may modify it using the editor or print it out and complete it manually. Eliminate the stress associated with your legal paperwork. Browse the extensive US Legal Forms library, where you can discover legal samples, verify their applicability to your situation, and download them immediately.

- Utilize the catalog navigation or search bar to find your template.

- Review the form's details to ensure it meets the standards of your state and locality.

- Examine the form preview, if available, to confirm it is indeed the document you need.

- Continue searching for the suitable template if the Share Merger Stock For Stock does not fulfill your requirements.

- Once you are confident in the form's applicability, download it.

- If you are a registered user, click Log in to verify your identity and access your chosen forms in My documents.

- If you have not yet established an account, click Buy now to acquire the template.

- Select the pricing option that aligns with your needs.

- Proceed to the registration process to complete your purchase.

- Conclude your transaction by selecting a payment method (credit card or PayPal).

- Choose the document format for downloading Share Merger Stock For Stock.

Form popularity

FAQ

The 7% rule in stocks refers to a guideline for investors on managing their investment risks. It suggests that you should not lose more than 7% of your initial investment before selling. This rule can help you protect your capital, especially in volatile markets. When considering share merger stock for stock transactions, understanding this rule can be crucial to maintaining your investment strategy.

Buying a stock during a merger can be a strategic decision, especially if you believe in the long-term vision of the new entity. However, it is essential to analyze both companies' financial health and market conditions before investing. The dynamics of share merger stock for stock can influence stock prices, creating opportunities or risks. Conducting thorough research and seeking expert advice, like those provided by US Legal Forms, can enhance your investment choices.

A share for share merger functions similarly to a stock-for-stock merger, where shareholders exchange their shares in the target company for shares in the acquiring company. This exchange is often structured around a specific ratio, determining how many shares they will receive in the new entity. When navigating share merger stock for stock, it is important to consider the long-term value and potential growth of the new shares. For assistance in understanding these transactions, US Legal Forms offers resources to guide you.

Stock for stock mergers work by allowing shareholders of a company to exchange their shares for shares in another company. This exchange is typically based on a predetermined ratio, which reflects the relative values of both companies. The goal is to create a unified entity that benefits from combined resources and market presence. Understanding the mechanics of share merger stock for stock is crucial, and platforms like uslegalforms can assist in navigating the legal and procedural aspects of these mergers.

An example of a stock for stock merger is the merger between Kraft Foods and Heinz, where Kraft shareholders received shares of the newly formed entity. This merger allowed both companies to leverage shared resources and expand their market reach. By studying such cases, you can gain a better understanding of how share merger stock for stock operates. Resources from uslegalforms can help you grasp the implications of these transactions.

Famous merger examples include the merger between Disney and Pixar, which created a powerhouse in animation, and the merger of Exxon and Mobil, forming one of the world's largest oil companies. These mergers reflect strategic decisions to enhance capabilities and market presence. Understanding these high-profile cases can shed light on the potential benefits and challenges of share merger stock for stock transactions. Exploring similar cases can provide valuable insights for your investments.

Filling out a stock transfer form requires you to provide specific details such as the name of the stockholder, the number of shares being transferred, and the name of the new shareholder. Ensure that you have all necessary information on hand, and double-check for accuracy before submitting the form to avoid delays. For ease, you can utilize platforms like uslegalforms that provide templates and guidance in navigating stock transfer processes related to share merger stock for stock.

Typically, the stock of the acquiring company may experience an increase in value following a merger announcement. However, this can vary based on market reactions, the perceived benefits of the merger, and overall economic conditions. It's essential to analyze the specific details of the merger and the companies involved to understand which stock might rise. Staying informed about share merger stock for stock trends can enhance your investment decisions.

forstock merger occurs when two companies combine and shareholders of one company receive shares of the other company in exchange for their existing shares. This type of merger allows the acquiring company to grow its market share while offering existing shareholders a stake in the new entity. Understanding the mechanics of share merger stock for stock can help you navigate the complexities of such transactions. You can find more information on platforms like uslegalforms.