Granting Stock Options To Foreign Employees

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Stock Option Grants And Exercises And Fiscal Year-End Values?

Managing legal paperwork can be exasperating, even for the most seasoned experts.

When you're looking for a Granting Stock Options To Foreign Employees and don't have the opportunity to spend time finding the correct and current version, the processes can be overwhelming.

US Legal Forms addresses any needs you may have, from personal to business documentation, all in one location.

Utilize sophisticated tools to complete and manage your Granting Stock Options To Foreign Employees.

Here are the steps to follow after accessing the desired form: Confirm this is the correct form by previewing it and reviewing its description. Ensure that the sample is recognized in your state or county. Click Buy Now when you are ready. Choose a monthly subscription plan. Select your preferred format and Download, fill out, eSign, print, and send your document. Take advantage of the US Legal Forms online library, backed by 25 years of experience and reliability. Streamline your everyday document management into a seamless and user-friendly process today.

- Access a valuable repository of articles, guidelines, and materials relevant to your circumstances and requirements.

- Save time and effort searching for the documents you require and use US Legal Forms’ advanced search and Preview feature to find Granting Stock Options To Foreign Employees and obtain it.

- If you have a subscription, Log In to your US Legal Forms account, locate the form, and acquire it.

- Check your My documents section to view the documents you have previously saved and to organize your folders as needed.

- If this is your first experience with US Legal Forms, create a free account and gain unlimited access to all the benefits of the library.

- A robust online form library could significantly improve the management of these situations.

- US Legal Forms stands as a leader in digital legal documents, offering over 85,000 state-specific legal forms available at any time.

- With US Legal Forms, you have access to tailored legal and business forms.

Form popularity

FAQ

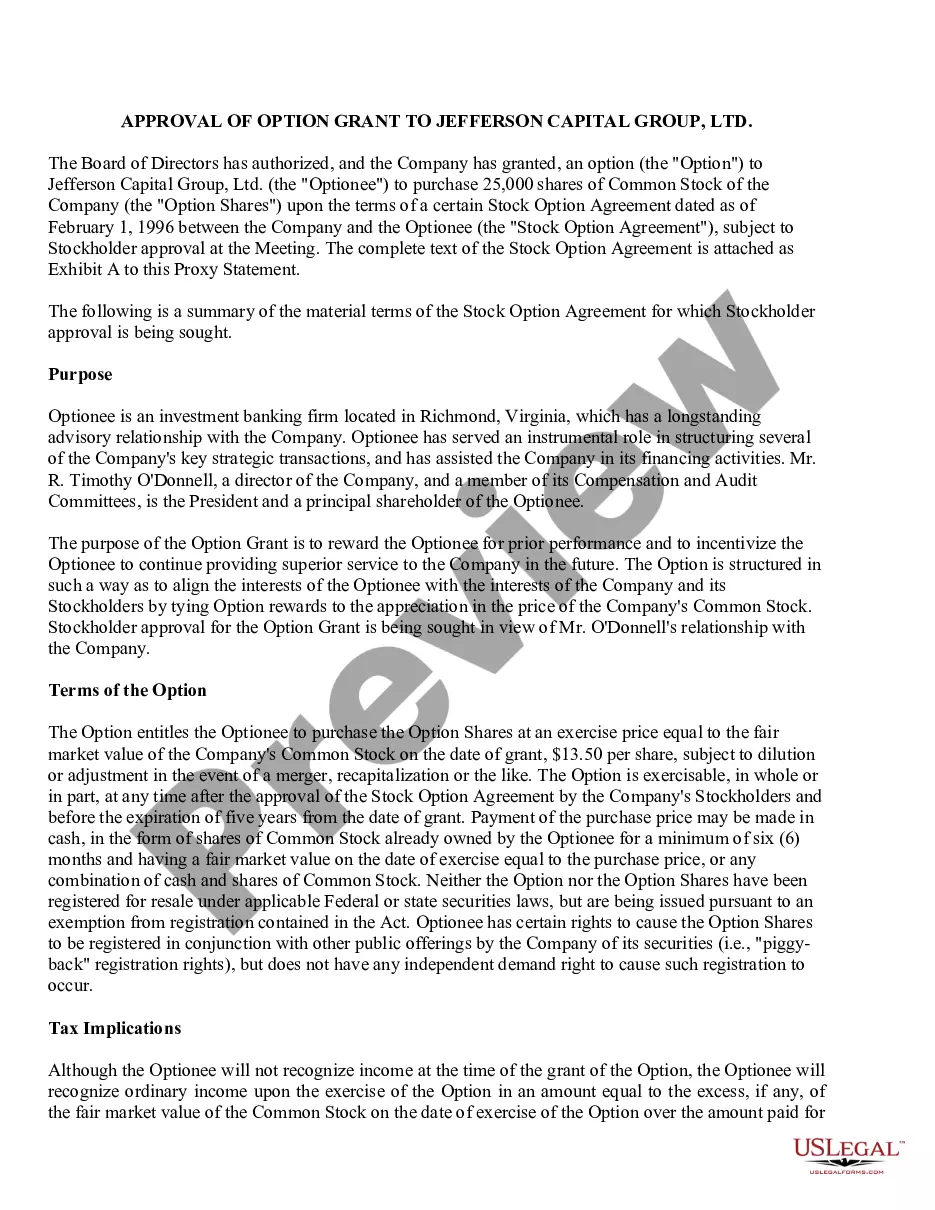

You cannot offer stock options to employees in other countries without having a firm grasp of those countries' labor laws. For example, some countries may prohibit certain performance metrics from being considered as part of an equity grant, while others may not allow performance to be considered at all.

Employee stock ownership plans (ESOPs) Employees can choose when to buy shares, usually at a predetermined price; purchasing shares makes the employee a partial owner, or shareholder, of the company. US-based and foreign employees are eligible to participate in an ESOP.

Generally speaking (it depends on the country), an overseas employee of a US company will not receive the tax benefit of an ISO, as most countries tax stock options when exercised. For this reason, US companies are more likely to issue NSOs to foreign employees.

Companies can grant ISOs or NSOs to their employees. However, they cannot grant ISOs to non-employees. Therefore, options granted to contractors/consultants, advisors and non-employee directors - can only be NSOs.

If an employee works for a qualifying U.S. company, they can receive ISOs. However, depending on the tax legislation of the country where the foreign employee resides, they may not receive the tax benefits that U.S. employees receive with ISOs. In this case, NSOs are often a better option for foreign employees.