Sample Restricted Stock Withholding Choices

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

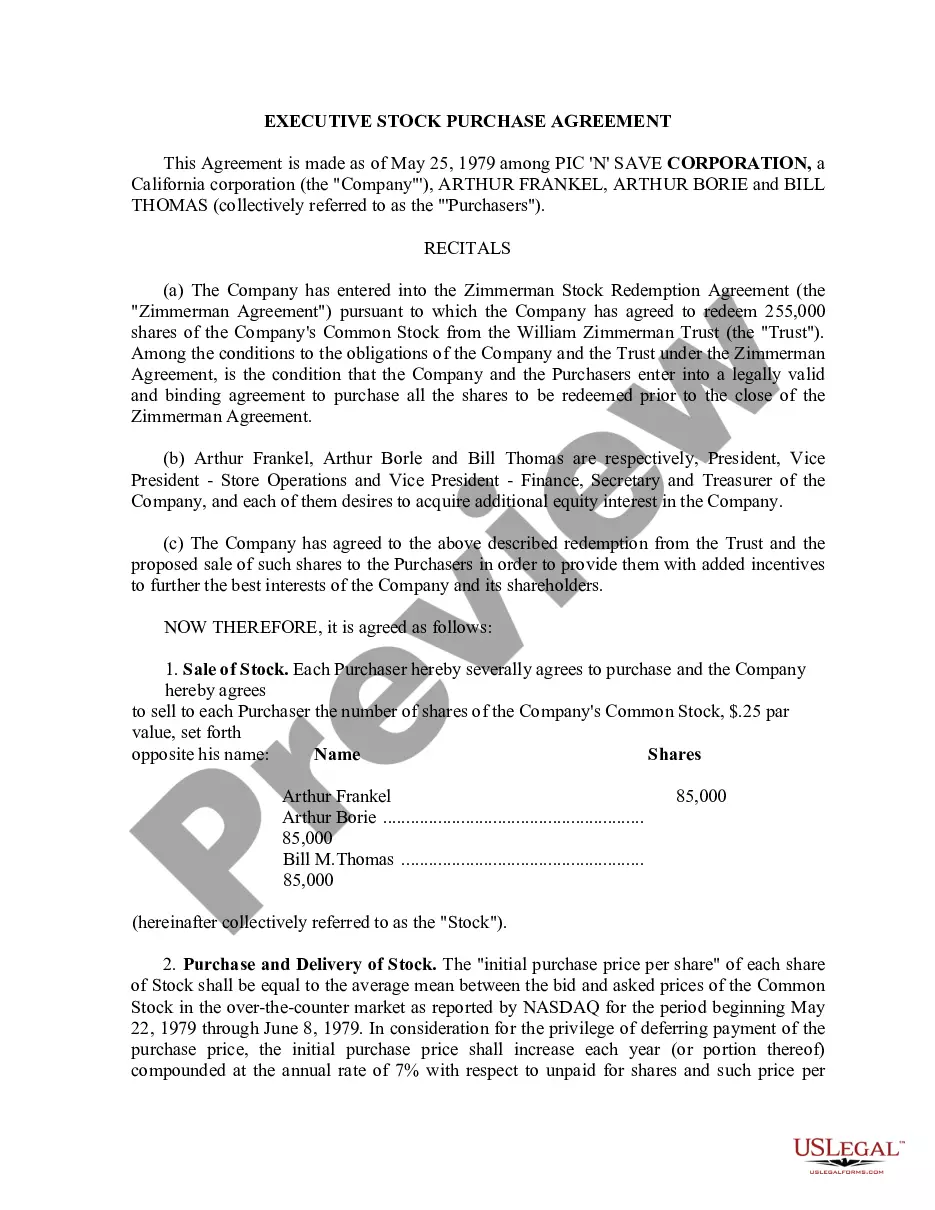

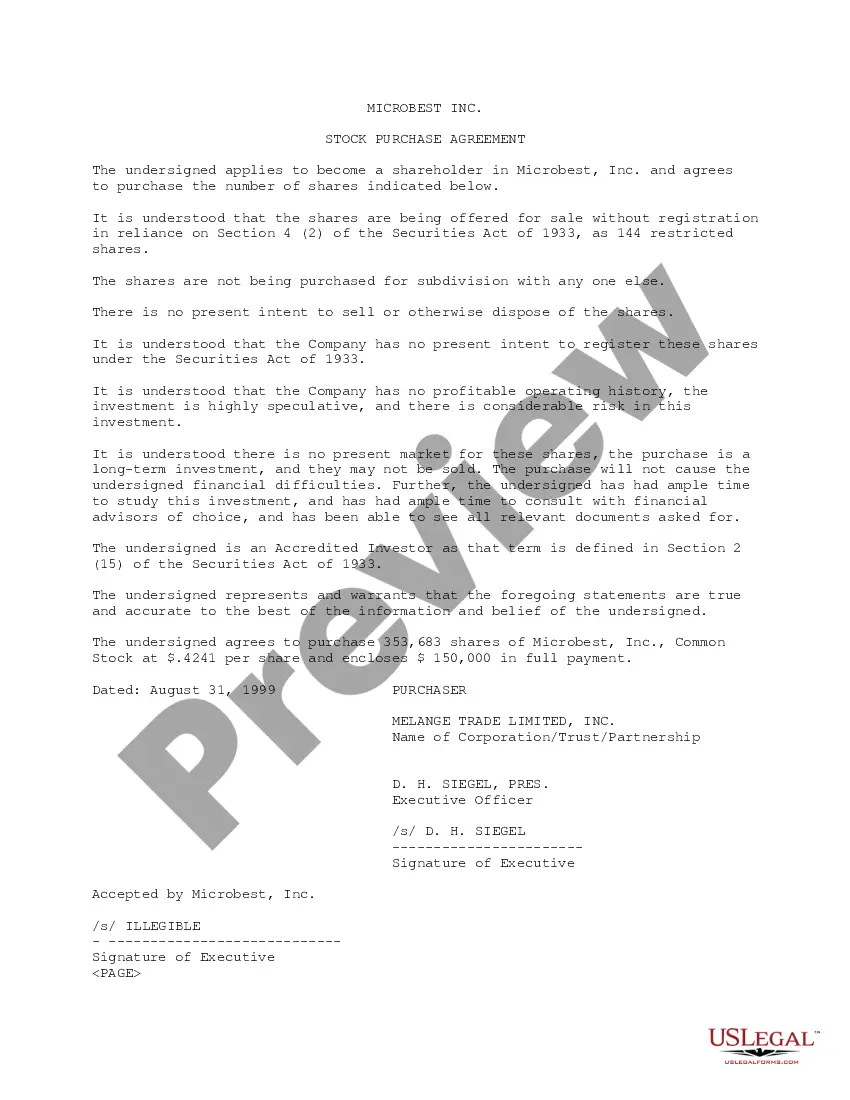

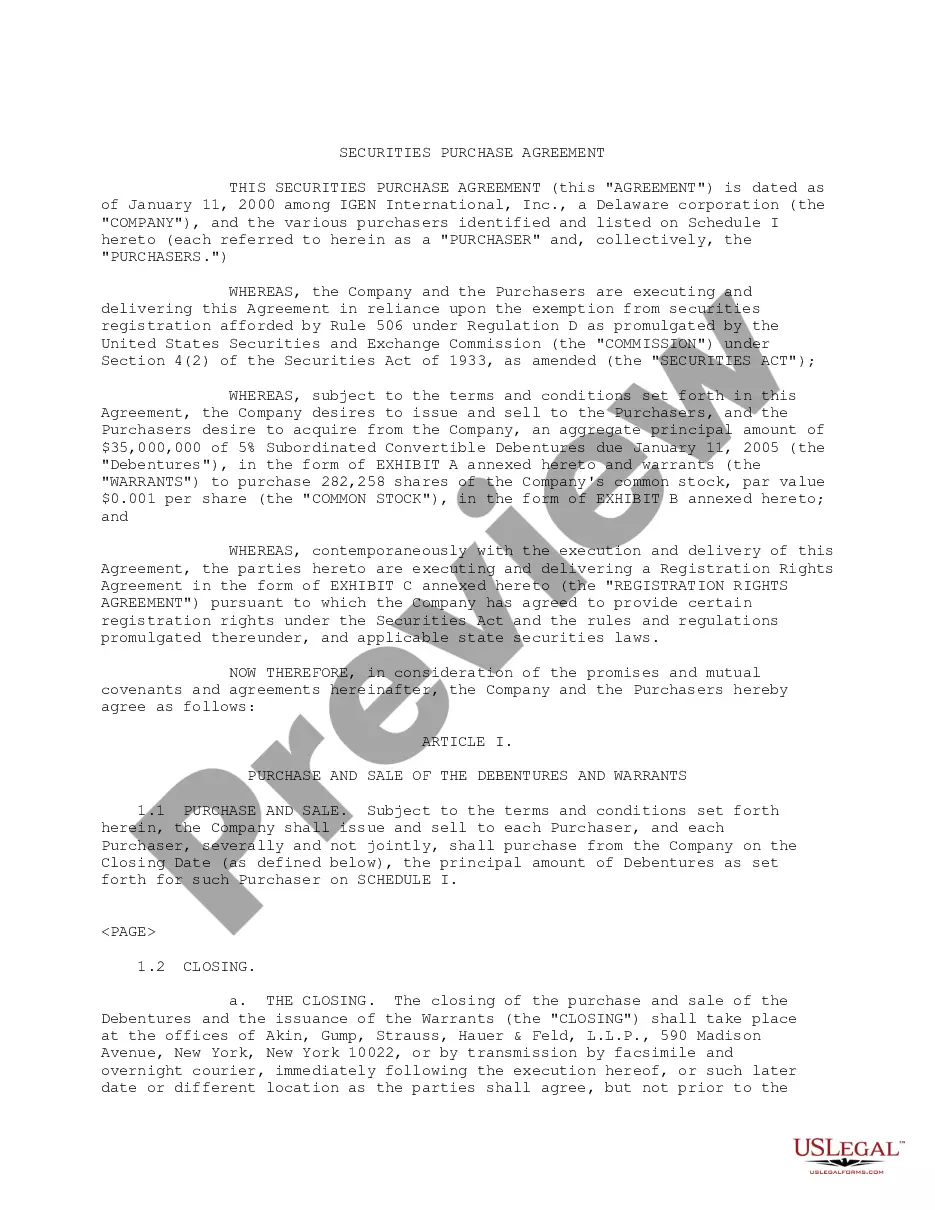

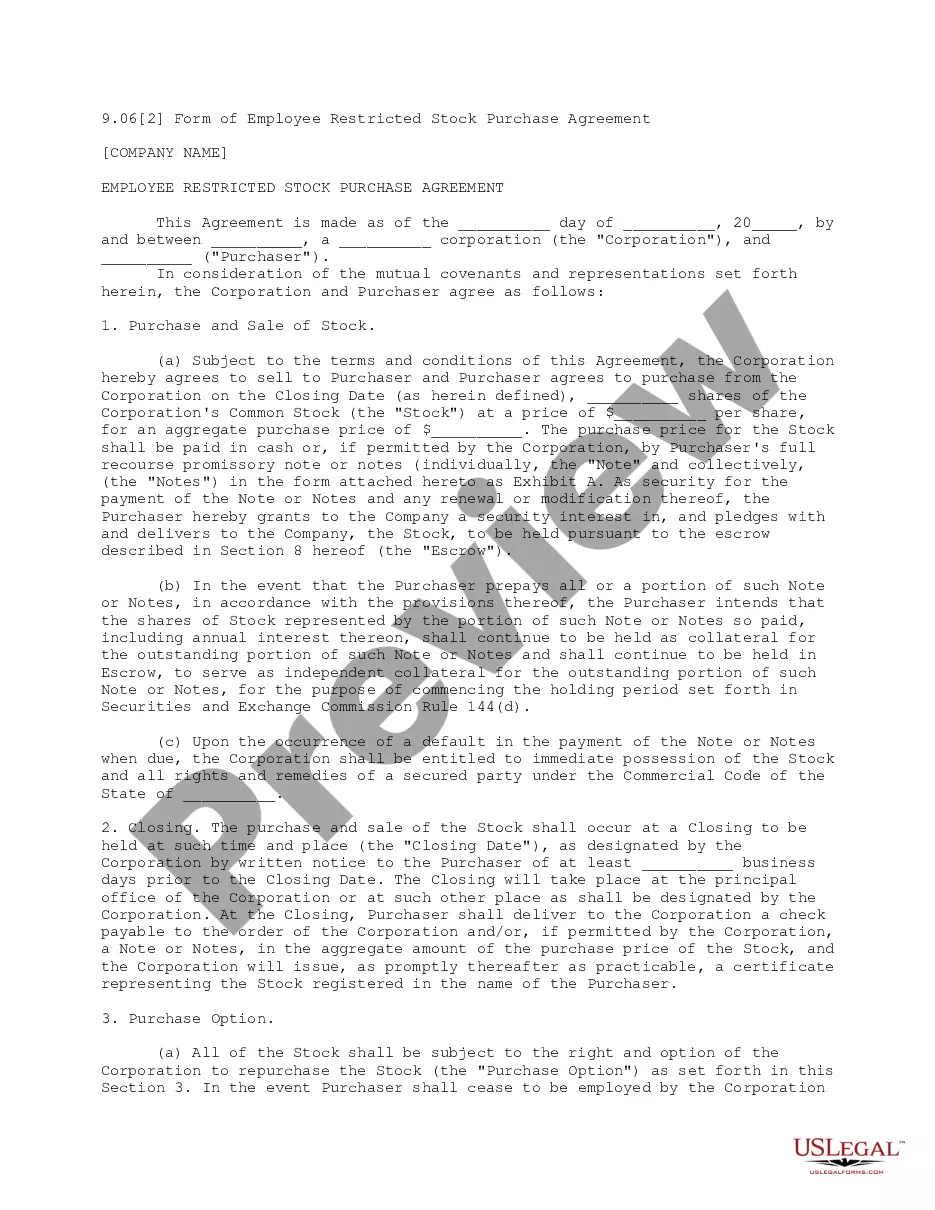

How to fill out Sample Restricted Stock Purchase Agreement Between Intermark, Inc. And Purchasers?

Securing a reliable source for obtaining the latest and suitable legal templates represents a significant part of managing bureaucracy.

Identifying the appropriate legal documents requires accuracy and meticulousness, which is why it is crucial to acquire samples of Sample Restricted Stock Withholding Choices solely from reputable providers, like US Legal Forms. An incorrect template will squander your time and delay the matter at hand. With US Legal Forms, you have minimal concerns.

Once you have the form saved on your device, you can edit it with the editor or print it and fill it out manually. Eliminate the hassle associated with your legal documentation. Explore the vast US Legal Forms library where you can locate legal templates, assess their relevance to your case, and download them instantly.

- Make use of the catalog navigation or search bar to find your template.

- Access the details of the form to ascertain whether it meets the criteria of your state and region.

- Preview the form, if available, to confirm that the template is the one you need.

- Continue searching and locate the appropriate template if the Sample Restricted Stock Withholding Choices does not meet your specifications.

- If you are certain about the form’s applicability, proceed to download it.

- If you are a registered user, click Log in to verify and access your chosen forms in My documents.

- If you do not have an account yet, click Buy now to acquire the template.

- Choose a pricing option that suits your needs.

- Advance to registration to complete your transaction.

- Finish your purchase by selecting a payment method (credit card or PayPal).

- Select the file format for downloading Sample Restricted Stock Withholding Choices.

Form popularity

FAQ

In almost all situations, it will be in your best interest to sell RSUs immediately upon vesting. As mentioned above, there is no tax benefit to holding on to RSU shares. Yes, hanging on to them for a year before selling allows you to pay long term capital gains rates.

A restricted stock unit (RSU) is a form of equity compensation that companies issue to employees. An RSU is a promise from your employer to give you shares of the company's stock (or the cash equivalent) on a future date?as soon as you meet certain conditions.

Income in the form of RSUs will typically be listed on the taxpayer's W-2 in the ?Other? category (Box 14). Taxpayers will simply translate the figure listed in Box 14 to their federal tax return and, if applicable, state tax return(s).

Here's an example. Say you've been granted 1,500 RSUs and the vesting schedule is 20% after one year of service, and then equal quarterly installments thereafter for the next three years. This would mean that after staying with your company for a year, 300 shares would vest and become yours.

RSUs are considered a form of compensation and are included in your taxable income when they vest. Because RSU income is considered supplemental, the withholding rate can vary between 22% and 37%. Usually, your employer will liquidate a percentage of the shares to cover the withholding requirement.