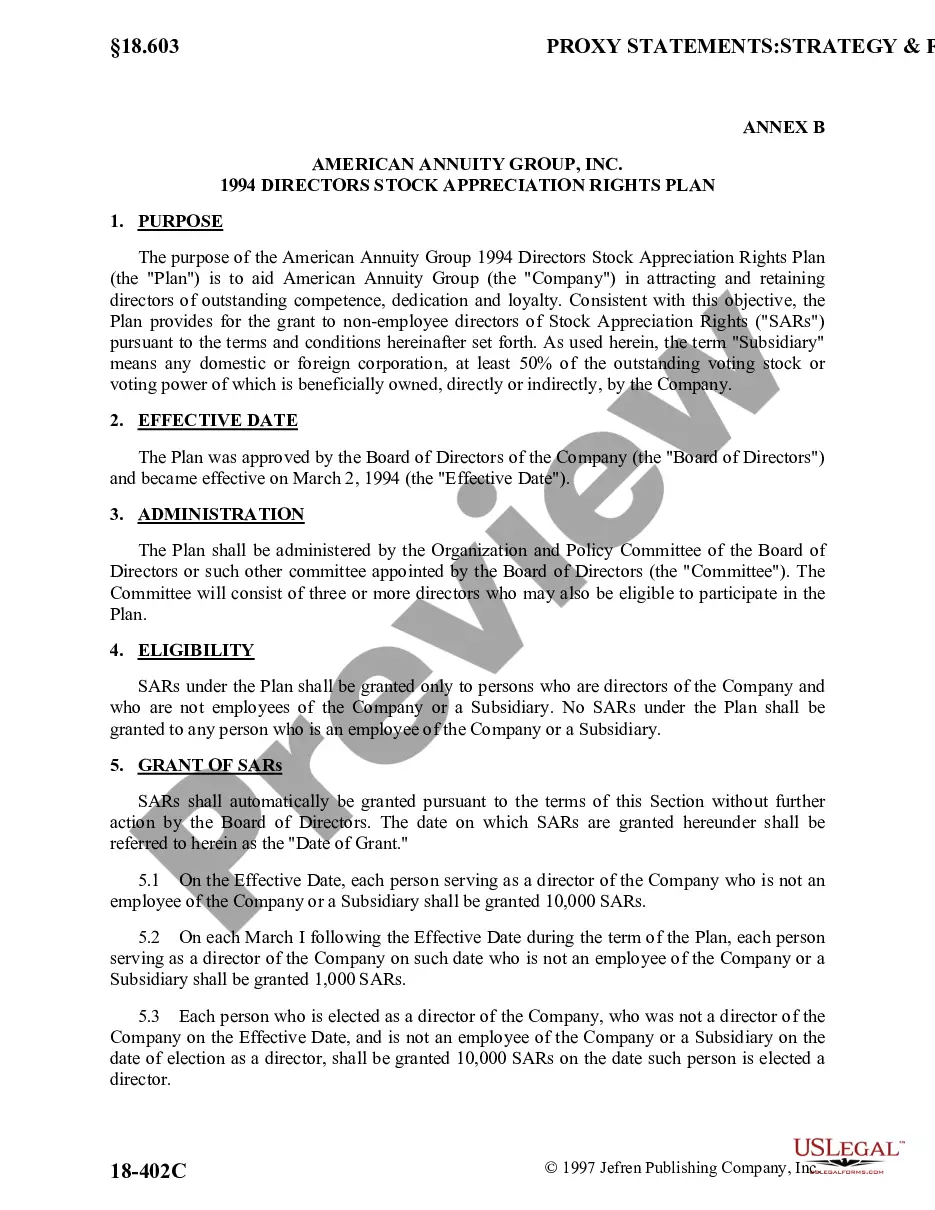

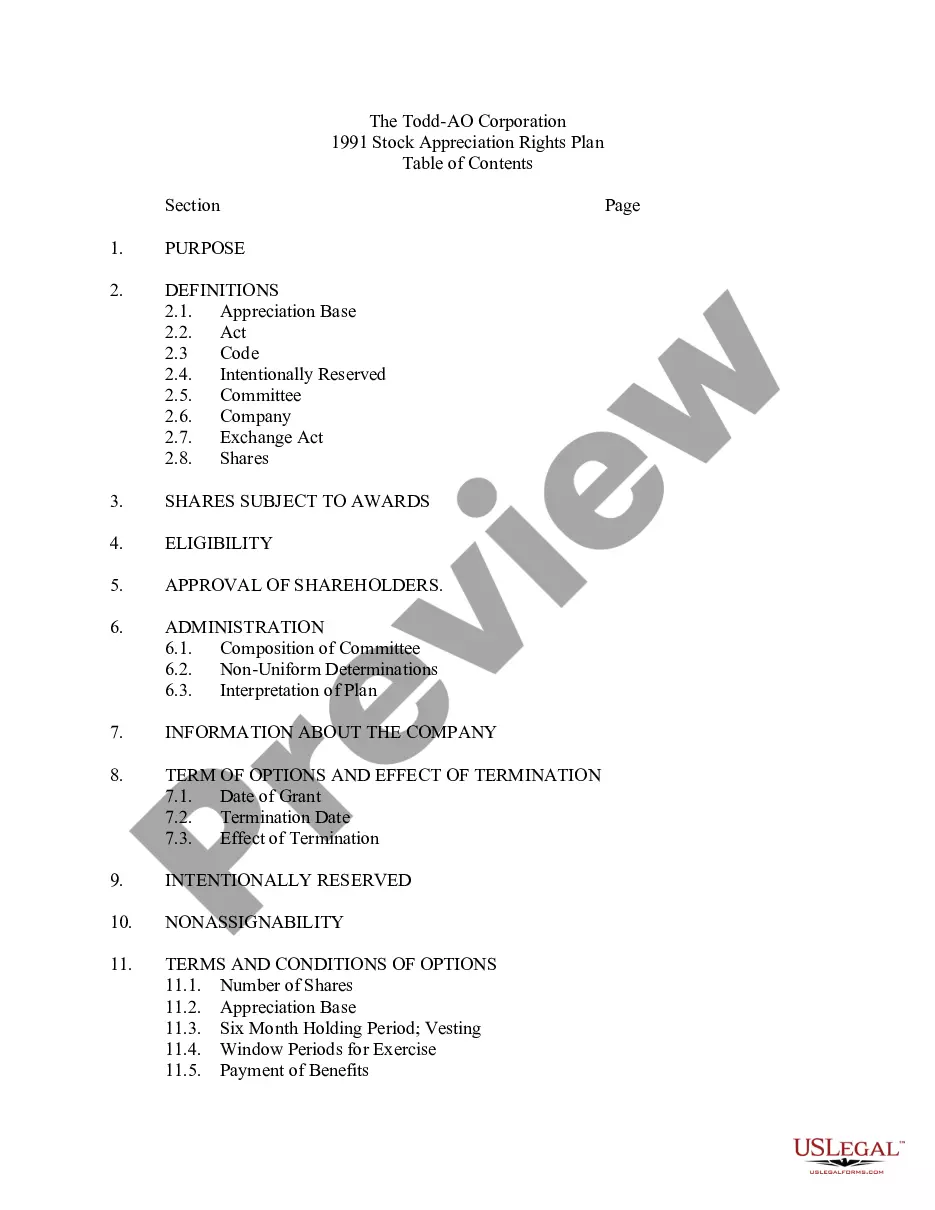

Stock Appreciation Right For The Future

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Stock Appreciation Right Plan Of Helene Curtis Industries, Inc.?

- For returning users, access your account and download the necessary template by clicking the Download button. Ensure your subscription is current, and renew if it has expired.

- If you’re new to US Legal Forms, begin by previewing the templates. Check the descriptions and confirm compatibility with your local legal requirements.

- Use the search function if your desired template isn't immediately visible. Look for alternatives until you find the perfect match for your needs.

- Once you locate the correct document, opt to purchase it by clicking the Buy Now button. Choose your preferred subscription plan and create an account for access.

- Complete the purchase by entering your payment details via credit card or PayPal to finalize the subscription.

- Finally, download your form and save it to your device. You can revisit your documents anytime through the My Forms section of your profile.

By following these steps, you can efficiently acquire legal documents while ensuring compliance with all necessary regulations.

Start your journey with US Legal Forms today and empower yourself with the legal tools you need. Visit their website to explore the vast array of available forms!

Form popularity

FAQ

The $100,000 rule pertains to Incentive Stock Options (ISOs), which states that a maximum of $100,000 in stock options can qualify for favorable tax treatment each year based on their grant date. If your options exceed this limit, the excess will convert to Non-Qualified Stock Options (NSOs) and lose some tax benefits. Understanding this rule can enhance your approach to managing your stock appreciation right for the future. Overall, using platforms like uslegalforms can clarify the intricacies involved.

The ideal time to exercise your Employee Stock Ownership Plan (ESOP) typically depends on the stock's performance and your financial goals. If the company shows signs of continued growth, waiting could increase your potential gains. However, if you anticipate a decline or need liquidity, exercising your ESOP sooner may be best. Consider how your ESOP fits within your overall stock appreciation right for the future strategy.

Yes, stock appreciation rights for the future can be granted to non-employees, such as consultants or independent contractors, depending on the company’s discretion. However, this practice varies by organization and may require specific agreements to outline the terms of the SAR. If you are a non-employee seeking these rights, it’s best to discuss potential options directly with the business.

Yes, stock appreciation rights generally have an expiration date, often ranging from a few years to ten years after the grant date. It’s crucial to be aware of this timeframe, as any unexercised rights will lapse once the expiration date passes. Understanding these details will help you make informed decisions about when to exercise your rights.

Typically, stock appreciation rights for the future are granted to employees, executives, and sometimes board members of a company. While primarily aimed at rewarding workers for their contribution, companies sometimes consider granting SARs to advisors or key stakeholders. Each organization sets its own policies and eligibility criteria, so it’s important to verify with your employer.

To obtain a stock appreciation right for the future, you typically need to be part of an organization that offers this incentive. Companies often grant SARs as part of employee compensation packages. You can request these rights during your employment negotiations or review corporate policies outlining their distribution. It’s wise to consult with HR or company leadership for specific details on eligibility.

Typically, stock appreciation rights are granted by your employer as part of an incentive program or compensation package. To receive these rights, you must meet specific criteria set by your employer, which may include your role and performance. Companies often implement SARs to motivate and retain high-performing employees, as they promise a share in future stock growth. If you seek to enhance your earnings potential, understanding how to navigate these opportunities is essential.

Yes, stock appreciation rights typically vest over time, much like stock options. This vesting process means that employees must meet specific conditions, such as employment duration, before they can fully exercise their rights. Understanding the vesting schedule is crucial when planning for the future, as it aligns employee incentives with long-term company performance. Knowing this helps set realistic expectations around stock appreciation rights.

While stock appreciation rights can provide significant benefits, they do have drawbacks. One main disadvantage is that employees may face substantial tax implications upon exercise, which could affect their financial planning. Additionally, SARs can create a false sense of wealth if the stock's performance does not meet expectations. It's essential to weigh these factors when considering stock appreciation rights for the future.