Personal Exemption For Trust

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

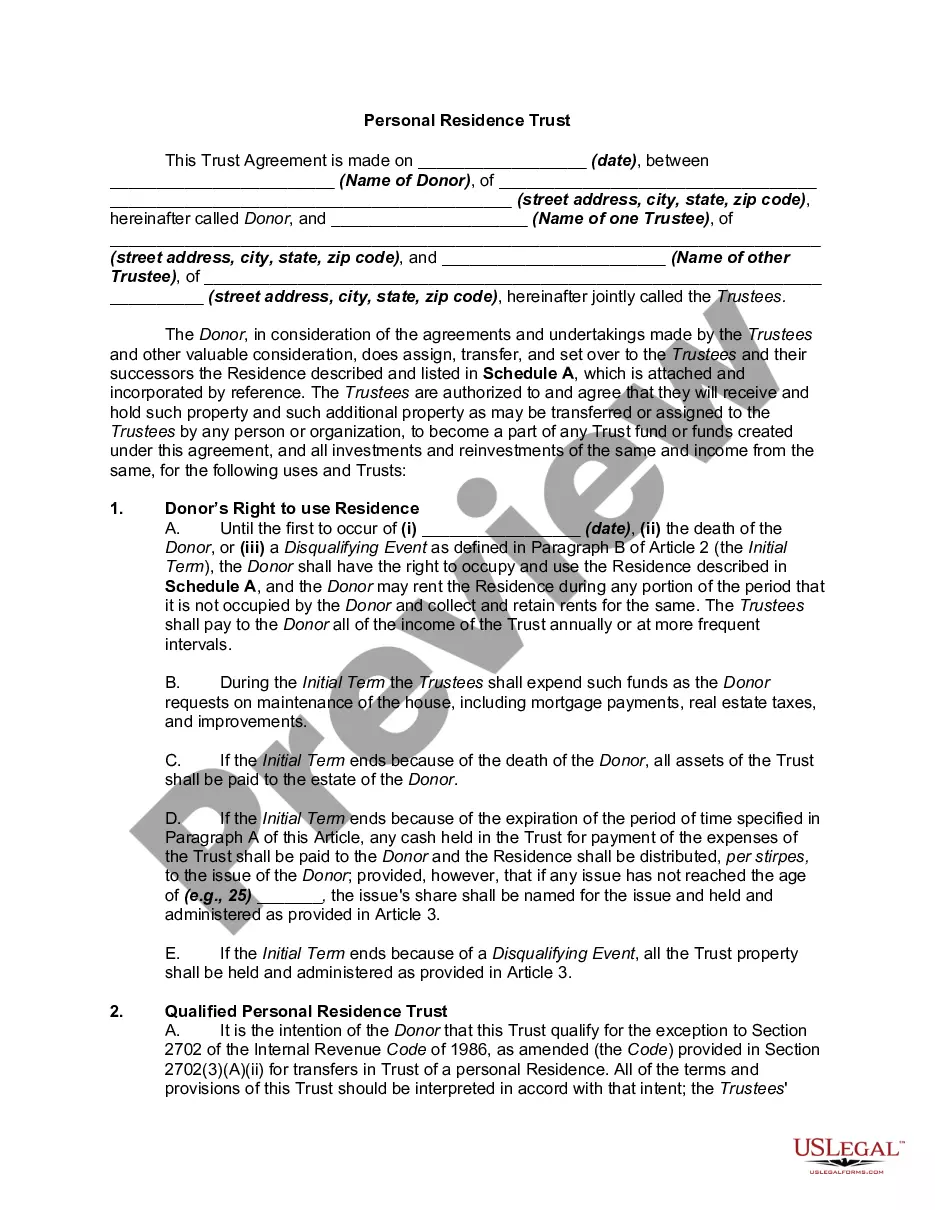

How to fill out Qualified Personal Residence Trust?

- If you're a returning user, log into your [US Legal Forms account](https://www.us and ensure your subscription is active. Click the Download button to retrieve the necessary template.

- For new users, start by previewing the form and reading the description to choose one that fits your needs and complies with local regulations.

- If the chosen template doesn't work, utilize the Search tab to find a more suitable option that fulfills your requirements.

- After selecting the right document, click the Buy Now button and choose a subscription plan. You'll need to register to access an extensive library of legal forms.

- Finalize your purchase by entering your payment details via credit card or PayPal.

- Once purchased, download the form and save it on your device. You can also find it in the [My Forms](https://www.us section of your profile at any time.

Using US Legal Forms not only empowers you to quickly execute legal documents, but also provides peace of mind with access to over 85,000 forms and direct assistance from premium experts.

Don't hesitate! Start your legal journey today with US Legal Forms and secure your personal exemption for trust effortlessly.

Form popularity

FAQ

While placing a home in a trust offers benefits, there are disadvantages to consider. One key issue is that transferring a personal residence into a trust can complicate your tax situation. For instance, the personal exemption for trust may not be applicable if the switching of properties leads to gains. Additionally, some trusts require ongoing maintenance and management, which can add to your overall responsibilities. Therefore, weigh these factors carefully before making a decision.

Yes, a trust can own a personal residence, allowing for seamless transfer of ownership and potential tax benefits. By holding a home in a trust, you can protect the property from probate and ensure that it passes directly to your beneficiaries. However, consider how the personal exemption for trust applies to this arrangement, as it may affect how gains from the sale of the home are taxed. It is wise to consult a legal expert to understand all implications.

The personal residence exclusion allows homeowners to exclude a certain amount of capital gains from taxes when selling their primary home. Under current tax laws, individuals can benefit from this exclusion, which may apply to trusts as well. Thus, understanding how the personal exemption for trust interacts with this exclusion can lead to significant tax savings. If you plan to sell a property held in a trust, knowing this information is vital.

Filling out a 1041 estate tax return involves collecting information on all income, deductions, and distributions for the estate or trust. You will need to provide details about the tax year and any relevant personal exemptions for trust deductions. Using solutions like uslegalforms can simplify this process and ensure you have the right forms and guidance.

To report trust income, you must file Form 1041, the U.S. Income Tax Return for Estates and Trusts. This form details all income, deductions, and distributions to beneficiaries. It's important to accurately calculate the personal exemption for trust to ensure compliance and proper tax treatment.

The exemption for a trust refers to the amount of income that can be excluded from taxation. These exemptions can help manage tax obligations for both trusts and beneficiaries. Understanding the personal exemption for trust rules can be crucial when establishing a trust, so consulting with a professional is essential.

The personal residence exclusion allows certain trusts to exclude gains from the sale of a primary residence. For individuals, this exclusion can significantly reduce taxable income. However, trusts must meet specific criteria to qualify, meaning the personal exemption for trust provisions must be applied carefully.

A simple trust does not allow for much flexibility in distribution of assets. Beneficiaries must receive all income generated by the trust, which can lead to higher personal tax rates for them. Additionally, a simple trust does not provide personal exemptions for trust assets, which can complicate tax planning.

The minimum income required to file a trust return usually depends on the type of trust and applicable tax laws. For many trusts, if income exceeds a particular threshold, filing a return becomes necessary. It's wise to consider the implications of the personal exemption for trust when determining your filing obligations.

Generally, if an irrevocable trust has no income, filing a tax return may not be necessary. However, it’s crucial to review the trust's provisions and consult with a tax expert. Understanding the application of the personal exemption for trust can help in determining your filing requirements.