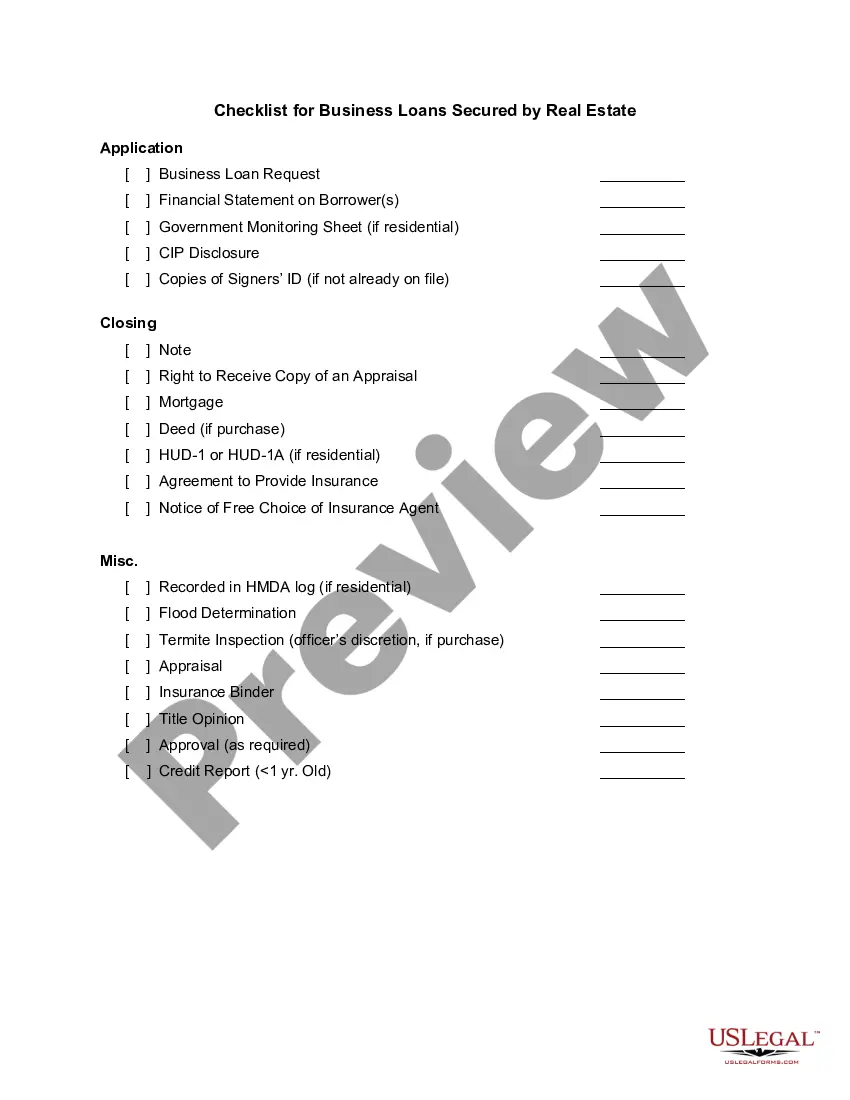

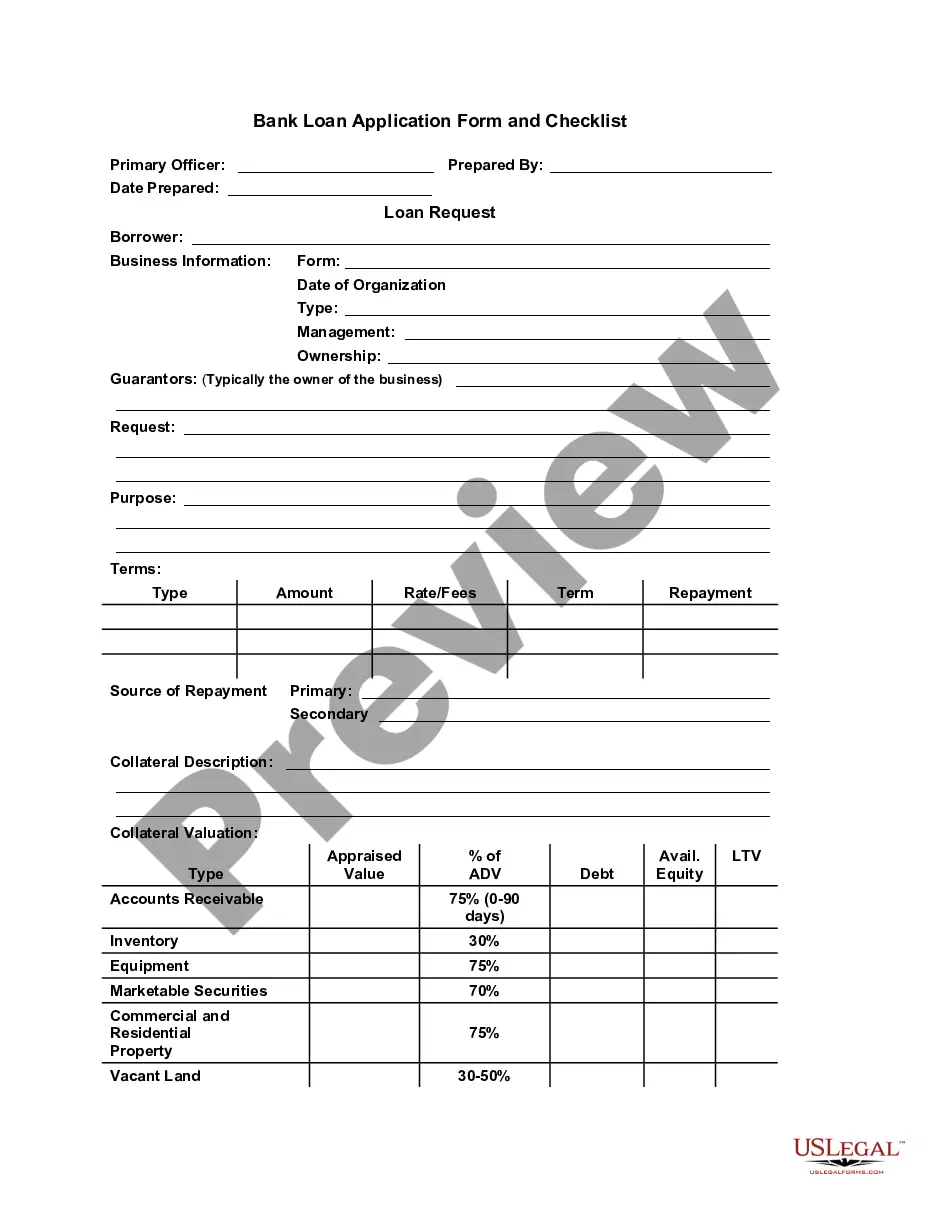

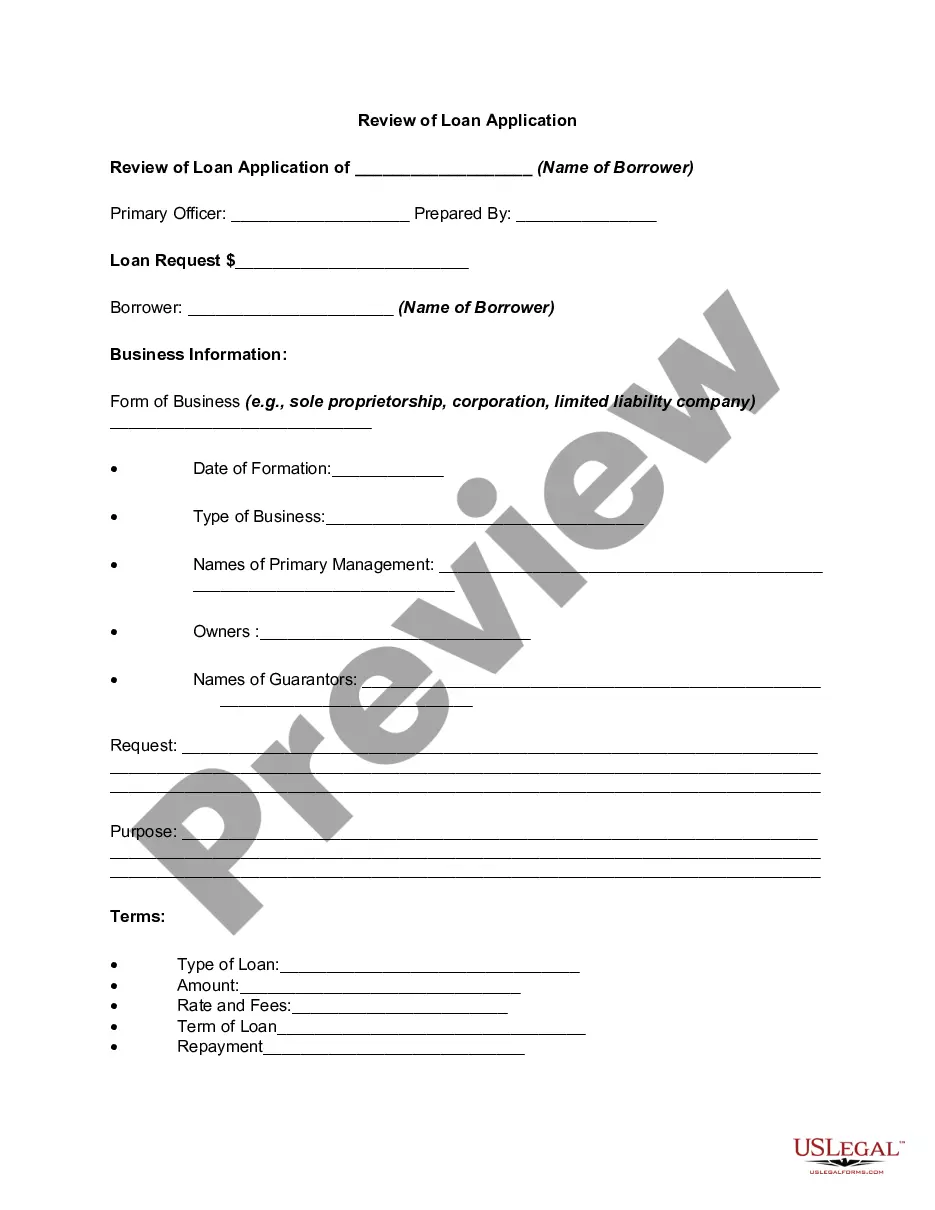

Loan Checklist Property Formula

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Loan Application - Review Or Checklist Form For Loan Secured By Real Property?

Legal administration can be perplexing, even for seasoned professionals.

When you are looking for a Loan Checklist Property Formula and don’t have the opportunity to spend time finding the correct and updated version, the processes can be anxiety-inducing.

US Legal Forms accommodates any needs you might have, from personal to business paperwork, all in one location.

Utilize cutting-edge tools to fill out and manage your Loan Checklist Property Formula.

Here are the steps to follow after accessing the form you need: Verify it is the correct form by previewing it and reviewing its description. Ensure that the template is validated in your state or county. Click Buy Now when you are ready. Select a monthly subscription plan. Choose the format you need, and Download, complete, eSign, print, and send your documents. Take advantage of the US Legal Forms web library, supported by 25 years of experience and trustworthiness. Streamline your everyday document management into a seamless and user-friendly process today.

- Access a repository of articles, guides, and materials pertinent to your situation and requirements.

- Save time and energy looking for the forms you need, and take advantage of US Legal Forms’ advanced search and Review feature to find Loan Checklist Property Formula and download it.

- If you have a subscription, Log In to your US Legal Forms account, search for the form, and download it.

- Check the My documents tab to view the documents you previously downloaded and to manage your folders as you see fit.

- If it is your first time using US Legal Forms, create an account and gain unlimited access to all the advantages of the library.

- A comprehensive web form library can be transformative for anyone seeking to navigate these circumstances efficiently.

- US Legal Forms is a frontrunner in online legal documents, with over 85,000 state-specific legal forms accessible to you at any time.

- With US Legal Forms, you can access state- or county-specific legal and business documents.

Form popularity

FAQ

Hear this out loud PauseMortgage lenders look at a variety of things in order to determine whether the borrower would be a good candidate for a mortgage loan. This includes income, debt-to-income ratio, credit score, assets, employment history and property type.

Lenders look at two ratios when determining how much mortgage you qualify for: Gross Debt Service ratio (GDS) ? total monthly housing costs shouldn't be more than 39% of your gross household income. Total Debt Service ratio (TDS) ? total debt load shouldn't be more than 44% of your gross household income.

Personal loan documents checklist KYC documents - Any government-issued KYC document such as an Aadhaar card, PAN card, passport or driving licence. Your employee ID card. Salary slips for the last three months. Bank account statements of your salary account for the previous three months.

The 28%/36% rule is a heuristic used to calculate the amount of housing debt one should assume. ing to this rule, a maximum of 28% of one's gross monthly income should be spent on housing expenses and no more than 36% on total debt service (including housing and other debt such as car loans and credit cards).

When you apply for a mortgage, lenders calculate how much they'll lend based on both your income and your outgoings - so the more you're committed to spend each month, the less you can borrow.