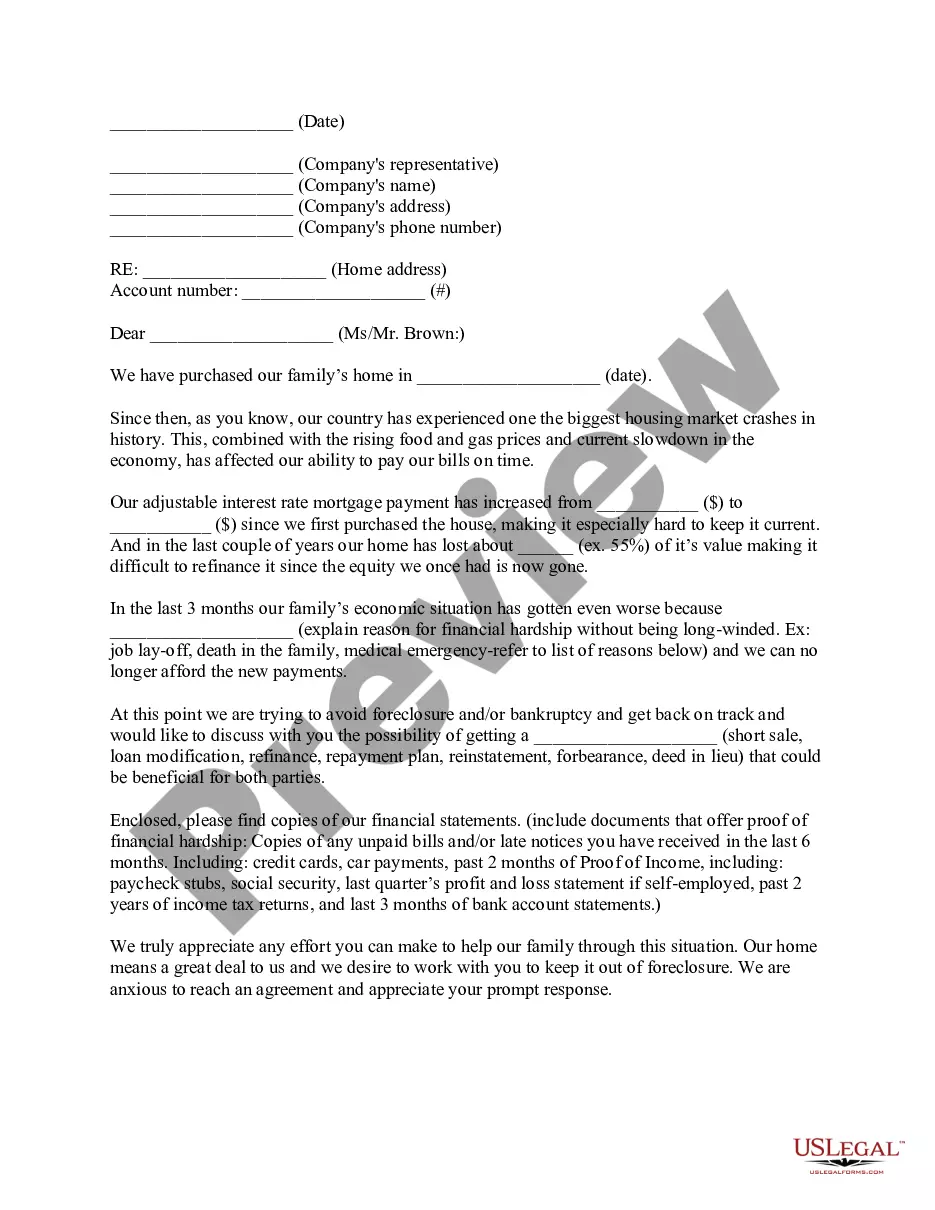

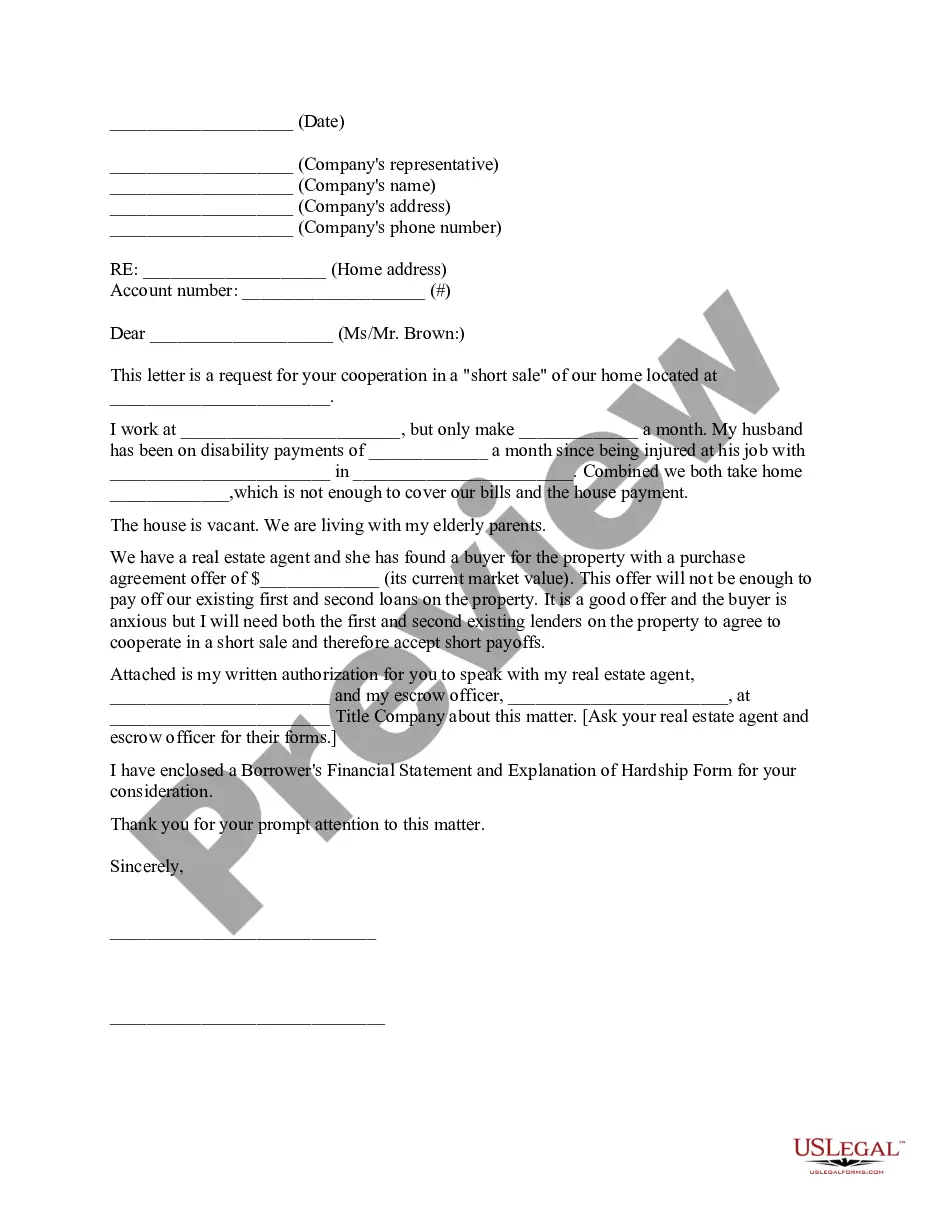

Requesting Loan From 401k

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Request To Lender Or Loan Servicer For Loan Modification Due To Financial Hardship - Requesting Change To Fixed Rate Of Interest Of Adjustable Rate?

The Loan Application From 401k you observe on this site is a reusable formal document crafted by expert attorneys in accordance with federal and local laws.

For over 25 years, US Legal Forms has supplied individuals, businesses, and legal professionals with more than 85,000 confirmed, state-specific documents for any business and personal situation. It’s the fastest, most straightforward, and most reliable method to obtain the papers you require, as the service ensures the highest degree of data security and anti-malware safeguards.

Register with US Legal Forms to have validated legal documents for all of life's circumstances at your fingertips.

- Examine the document you seek and verify it.

- Choose the pricing plan that fits you and create an account. Employ PayPal or a credit card for a quick payment. If you already possess an account, Log In and examine your subscription to continue.

- Select the format you desire for your Loan Application From 401k (PDF, DOCX, RTF) and download the sample to your device.

- Print the document to fill it out manually. Alternatively, use an online versatile PDF editor to swiftly and accurately complete and sign your form electronically.

- Utilize the same document again whenever needed. Access the My documents section in your profile to redownload any forms previously obtained.

Form popularity

FAQ

When requesting a loan from a 401(k), you can usually borrow up to $50,000 or 50% of your vested balance, whichever is less. This limit provides access to necessary funds while still protecting your overall retirement savings. Keep in mind that the rules may vary based on your plan, so it's essential to check with your plan administrator. Always consider your repayment ability to avoid unnecessary penalties.

By age 59.5 (and in some cases, age 55), you will be eligible to begin withdrawing money from your 401(k) without having to pay a penalty tax. You'll simply need to contact your plan administrator or log into your account online and request a withdrawal.

If you decide to borrow from your retirement savings, you can submit your request via the ADP Mobile App, or on your plan's Participant Website. If you decide a hardship withdrawal is right for you, you can submit and certify your request via the ADP Mobile App, or on your plan's Participant Website.

The short answer: It depends. If debt causes daily stress, you may consider drastic debt payoff plans. Knowing that early withdrawal from your 401(k) could cost you in extra taxes and fees, it's important to assess your financial situation and run some calculations first. Here's how to do that.

?This is generally not a preferred option, as the money in the retirement plan is, after all, designated for life in retirement years,? says Sean Fox, president of Achieve Resolution in San Mateo, California. There could also be other ways to pay off debt that don't include tapping 401(k) funds.

Some of the reasons why you can't borrow from your 401(k) include lack of spousal consent, you are nearing retirement, you have exhausted your 401(k) loan limit, you are no longer working for the employer, or if your job position is at risk due to ongoing restructuring.