Home Loan In Form 16

Description

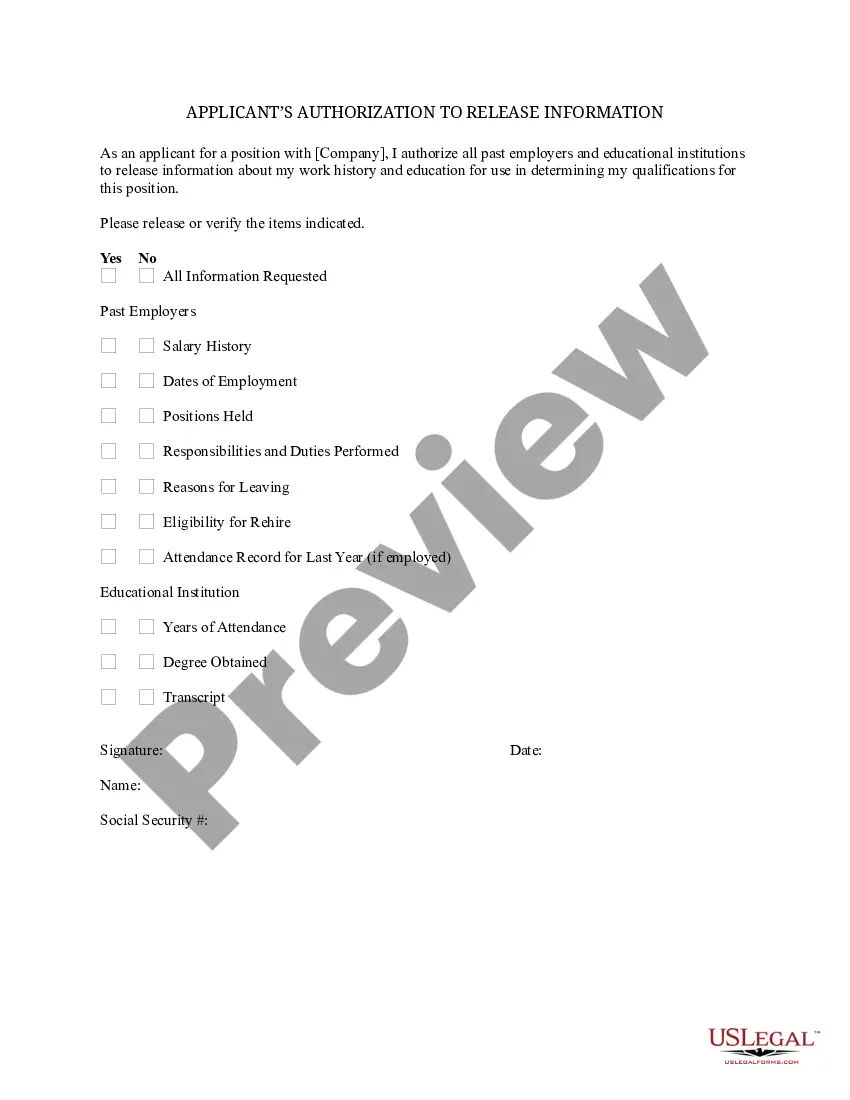

How to fill out Home Equity Conversion Mortgage - Reverse Mortgage?

The Home Loan In Form 16 you see on this page is a reusable formal template drafted by professional lawyers in accordance with federal and state laws and regulations.

For over 25 years, US Legal Forms has supplied individuals, companies, and legal practitioners with more than 85,000 authenticated, state-specific forms for any commercial and personal scenario.

Choose the format you desire for your Home Loan In Form 16 (PDF, DOCX, RTF) and download the sample onto your device.

- Search for the document you require and examine it.

- Browse through the example you searched and preview it or review the form description to ensure it meets your needs. If it doesn’t, use the search feature to find the suitable one. Click Buy Now once you have found the template you require.

- Register and Log In.

- Select the pricing plan that fits you and set up an account. Use PayPal or a credit card for a swift transaction. If you already possess an account, Log In and verify your subscription to proceed.

- Obtain the editable template.

Form popularity

FAQ

Current IRS rules allow many homeowners to deduct up to the first $750,000 of their home mortgage interest costs from their taxes. Homeowners who are married but filing separately may be allowed to deduct up to the first $350,000 of their mortgage interest costs.

Is all mortgage interest deductible? Not all mortgage interest can be subtracted from your taxable income. Only the interest you pay on your primary residence or second home can be deducted if the loans were used to purchase, build or improve your property, or used for a business-related investment.

If the loan is not a secured debt on your home, it is considered a personal loan, and the interest you pay usually isn't deductible. Your home mortgage must be secured by your main home or a second home.

In general, you can deduct the mortgage interest you paid during the tax year on the first $750,000 of your mortgage debt for your primary home or a second home. If you are married filing separately the limit drops to $375,000.

The interest you pay on a qualified mortgage or home equity loan is deductible on your federal tax return, but only if you itemize your deductions and follow IRS guidelines.