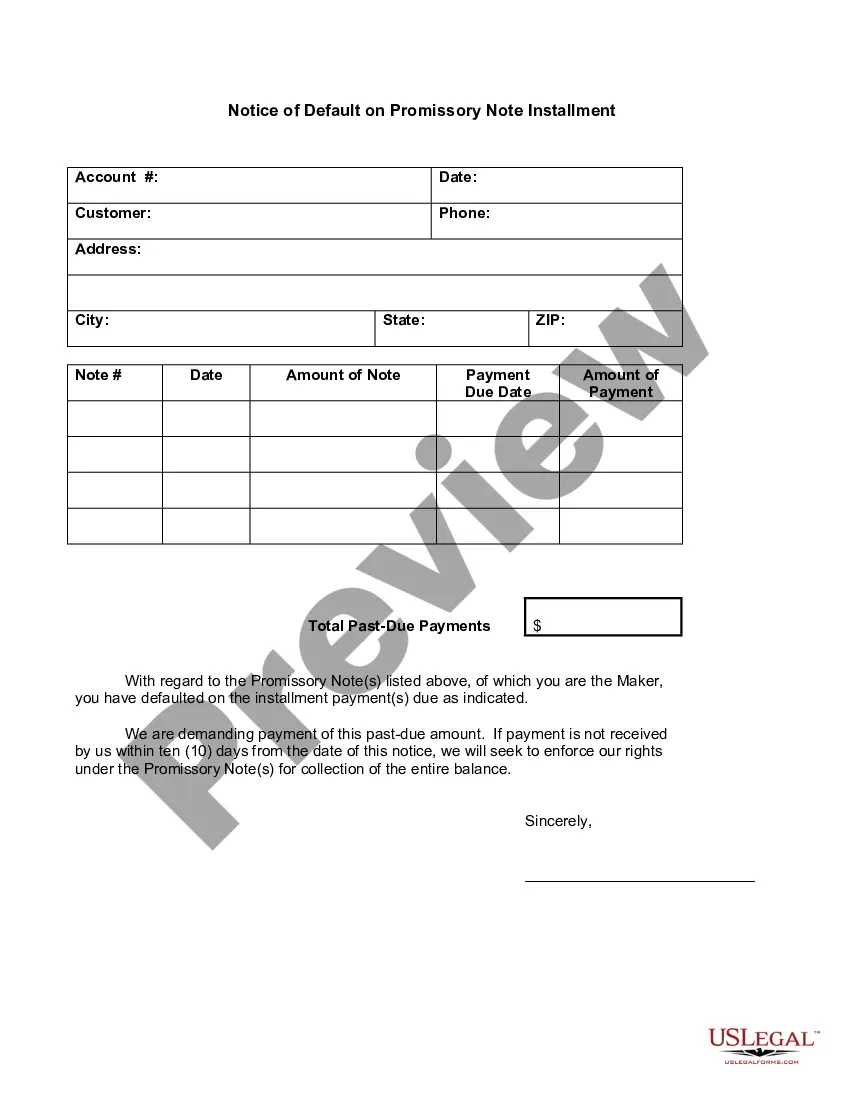

Default Promissory Note Without Interest Tax Implications

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Notice Of Default In Payment Due On Promissory Note?

Bureaucracy necessitates exactness and correctness.

If you do not engage with completing documentation like the Default Promissory Note Without Interest Tax Implications regularly, it may lead to some confusions.

Choosing the right template from the outset will guarantee that your document submission proceeds smoothly and avoids any hassles of resubmitting a document or repeating the same task from the beginning.

If you are not a registered user, finding the required template will take a few more steps: Locate the template using the search bar.

- Acquire the appropriate template for your documentation at US Legal Forms.

- US Legal Forms is the largest online forms repository that provides over 85 thousand templates for many domains.

- You can access the latest and most pertinent version of the Default Promissory Note Without Interest Tax Implications by simply searching it on the site.

- Find, store, and save templates in your account or confirm with the description to ensure you possess the correct one available.

- With an account at US Legal Forms, it is simple to gather, store in one place, and navigate the templates you save for quick access.

- When on the site, click the Log In button to authenticate.

- Then, visit the My documents page, where your forms history is kept.

- Review the descriptions of the forms and save those you need at any given moment.

Form popularity

FAQ

A promissory note must specify the percentage interest charged on the loan. All loans should carry some interest, even if it is between family members.

If interest on your loan is calculated as simple interest, the formula for calculating interest begins with the total principal balance multiplied by the interest rate. For example, if the principal is $5,000 and the interest rate is 15 percent, multiply 5,000 by 0.15 to equal 750.

The buyer doesn't want to have to pay interest, and the seller feels funny asking for it, so they agree, no interest. Unfortunately, the IRS may impute interest received to the seller, even if the parties agreed to zero interest or a rate below the IRS' published rates.

The borrower records the note by debiting the cash account and crediting the notes payable account. The rest of the notes payable formula includes that interest due to date is accrued at the end of each financial period by debiting the interest expense account and crediting the interest payable liability account.

Based on discussions with professionals who buy and sell notes, the market rate of return for a privately held note typically ranges from 12% for a well collateralized note with a strong payment history to 25% for an uncollateralized note.