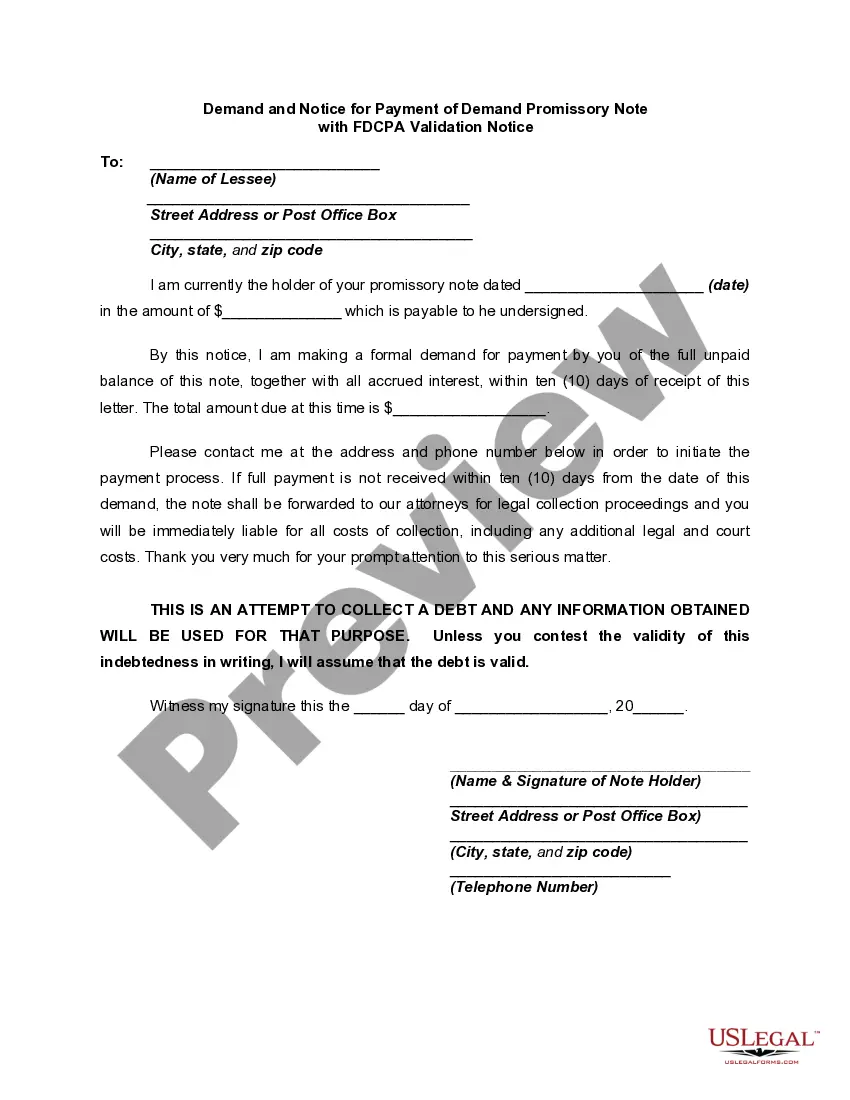

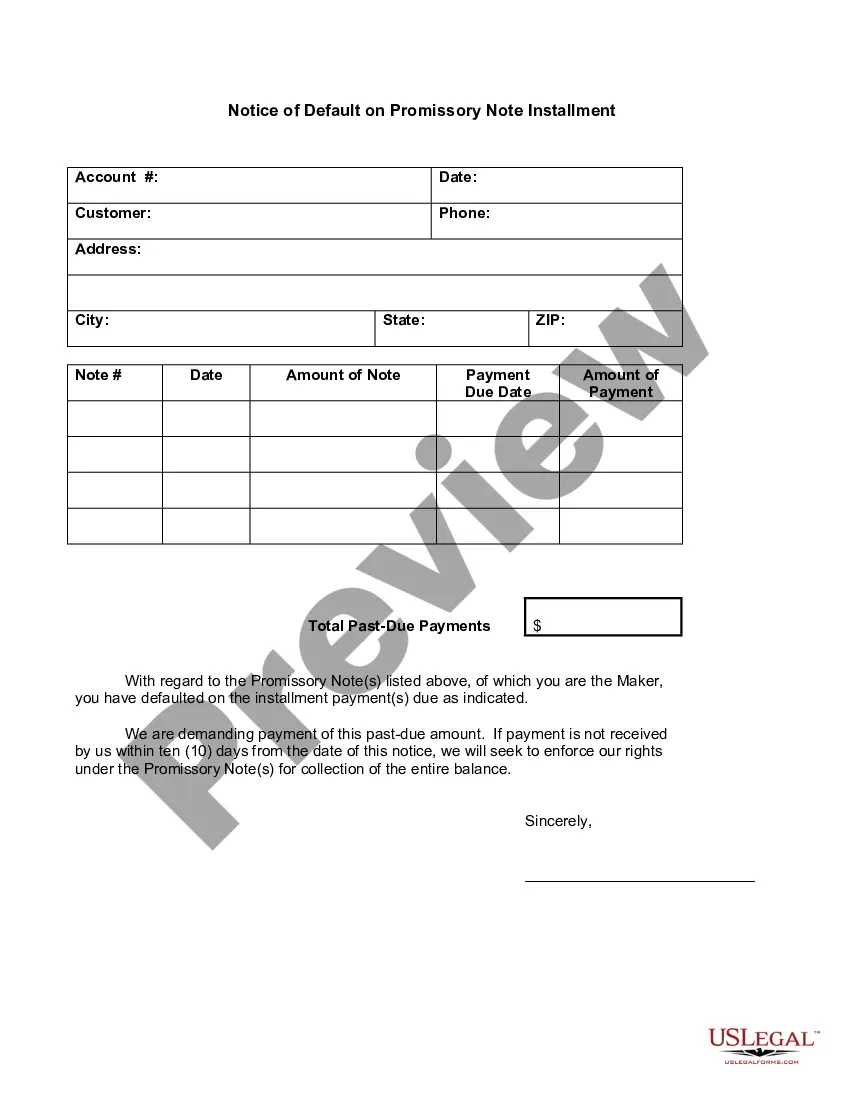

Default Promissory Note For Payment

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Notice Of Default In Payment Due On Promissory Note?

Individuals frequently link legal documentation with something complex that only a specialist can handle.

In some respects, that's accurate, as creating a Default Promissory Note For Payment requires significant expertise in subject aspects, including state and local statutes.

Nevertheless, with US Legal Forms, the process has become more straightforward: ready-to-use legal documents for any personal and business event tailored to state regulations are gathered in one online repository and are now accessible to all.

All templates in our library are reusable: once acquired, they remain stored in your profile. You can access them whenever necessary through the My documents tab. Explore all the advantages of using the US Legal Forms platform. Subscribe today!

- US Legal Forms provides over 85k current documents categorized by state and area of use, making it easy to find a Default Promissory Note For Payment or any specific template in just minutes.

- Previously registered users with an active subscription must Log In to their account and click Download to retrieve the form.

- New users will first have to create an account and subscribe before they are able to save any documents.

- Here’s a step-by-step guide on how to obtain the Default Promissory Note For Payment.

- Examine the page contents thoroughly to confirm it meets your requirements.

- Review the form description or check it through the Preview feature.

- If the previous example doesn’t meet your needs, search for another sample using the Search bar above.

- When you discover the appropriate Default Promissory Note For Payment, click Buy Now.

- Choose a subscription plan that aligns with your requirements and financial plan.

- Create an account or Log In to proceed to the payment page.

- Pay for your subscription using PayPal or your credit card.

- Select the desired format for your file and click Download

Form popularity

FAQ

At its most basic, a promissory note should include the following things:Date.Name of the lender and borrower.Loan amount.Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral?Payment amount and frequency.Payment due date.Whether the loan has a cosigner, and if so, who.

A Promissory Note will only be enforceable if it includes all the elements which are necessary to make it a legal document.

Default could happen with one missed payment or might not occur until after several payments have been missed, depending on the terms of the note. The promissory note itself should set out what constitutes default, so that both the lender and the borrower are clear on the terms.

A default occurs when a borrower is unable to make timely payments, misses payments, or avoids or stops making payments on interest or principal owed. Defaults can occur on secured debt, such as a mortgage loan secured by a house, or unsecured debt such as credit cards or a student loan.

What Happens When a Promissory Note Is Not Paid? Promissory notes are legally binding documents. Someone who fails to repay a loan detailed in a promissory note can lose an asset that secures the loan, such as a home, or face other actions.