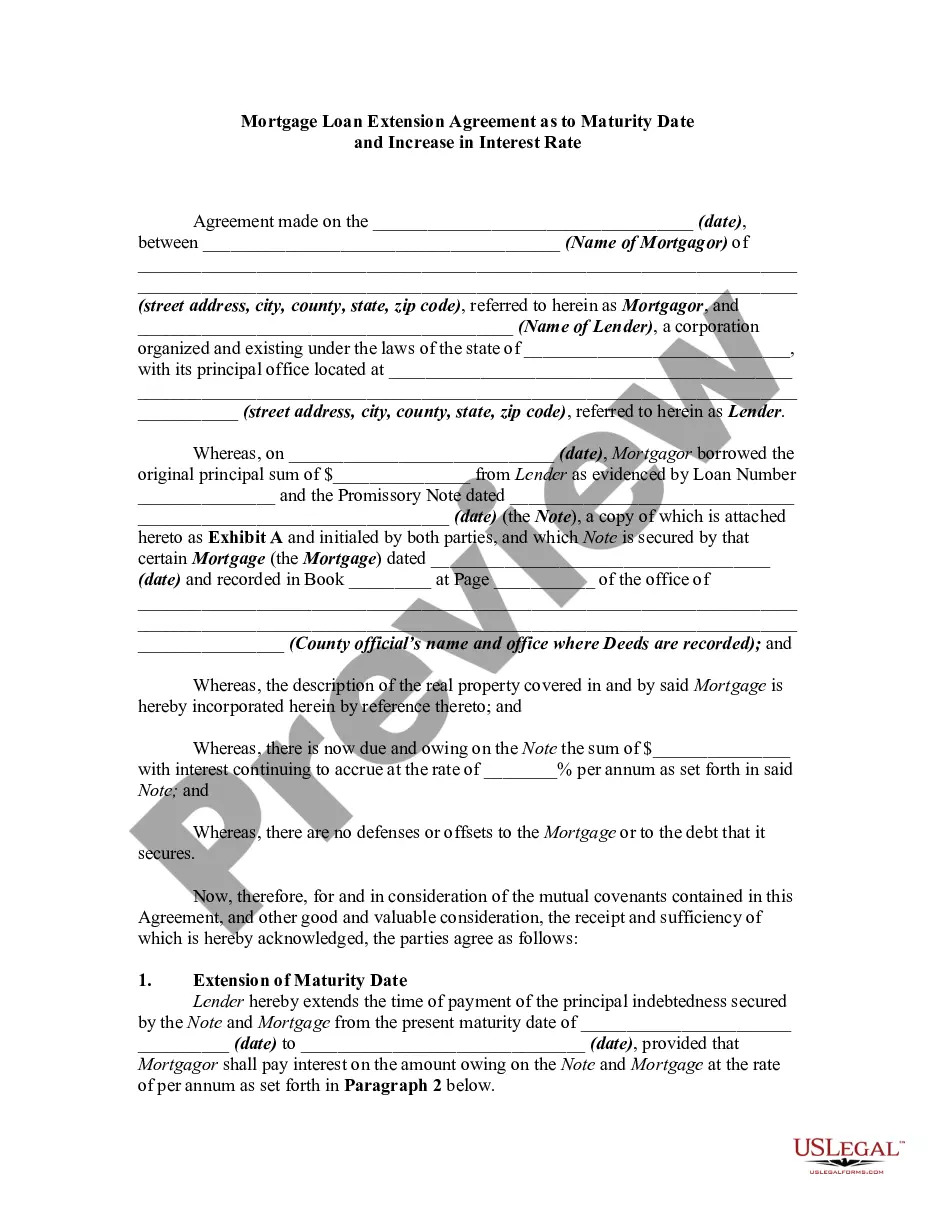

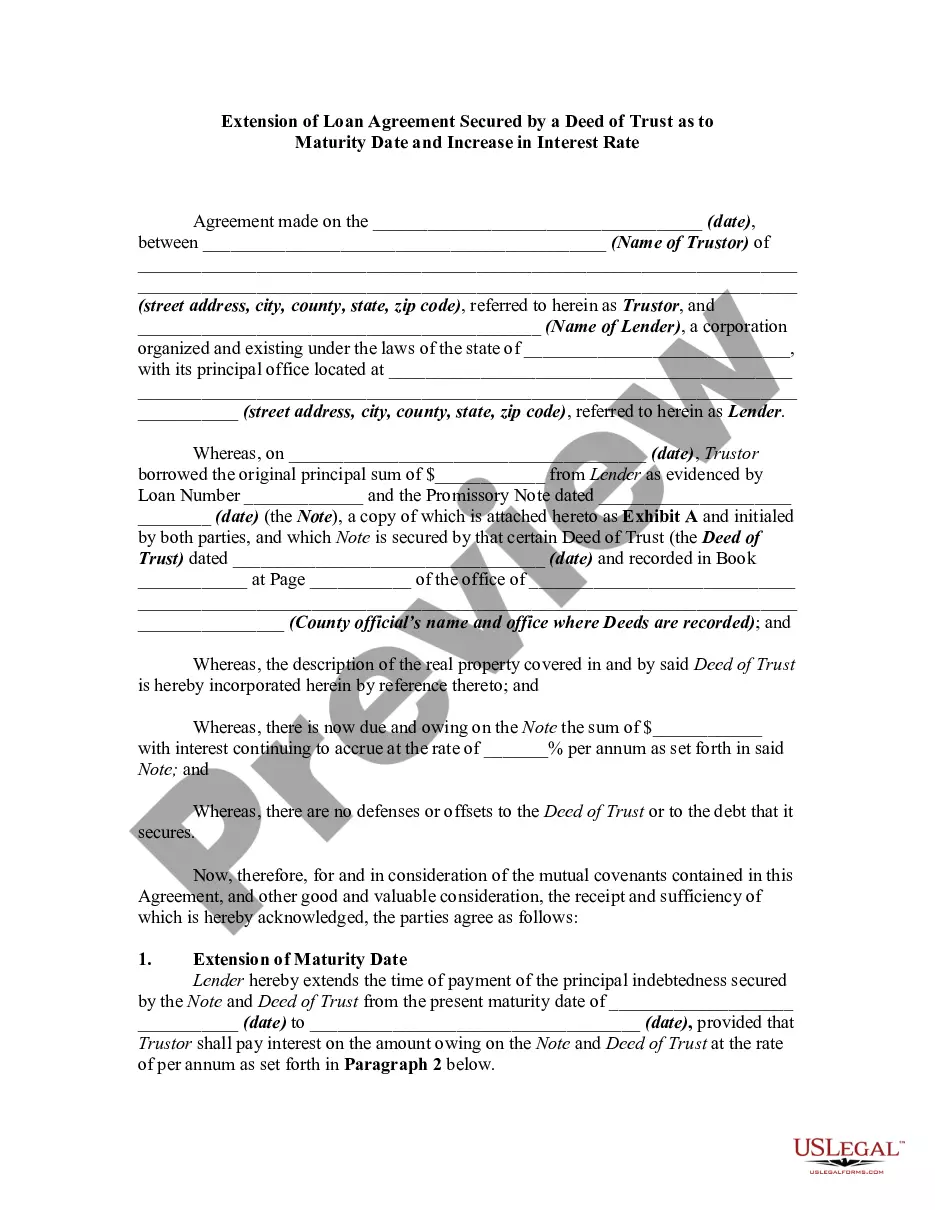

Mortgage Forbearance Extension 18 Months

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

The forbearance rule outlines the terms and conditions under which borrowers can enter into a forbearance agreement with their mortgage lender. It typically includes specific timeframes, such as the mortgage forbearance extension 18 months, which grants borrowers additional months to manage repayments. Understanding this rule ensures that you can effectively negotiate terms that suit your financial needs.

The forbearance policy allows homeowners to temporarily pause or reduce their mortgage payments during financial hardship. This arrangement can help you manage difficult situations while keeping your home secure. With the mortgage forbearance extension 18 months, homeowners have the opportunity to extend their period of relief, providing more time to regain financial stability.

You can usually apply for mortgage forbearance at any point during financial difficulties, but it’s essential to do so quickly. Many lenders allow you to request forbearance for a limited time after missing a payment. If you are considering a mortgage forbearance extension of 18 months, it’s best to apply as early as possible to maximize your options with your lender.

The duration of a forbearance plan can vary, typically lasting up to 12 months. However, with a mortgage forbearance extension of 18 months, you may extend this period if you demonstrate financial need. This extended timeframe allows you more flexibility, making it easier to manage your financial obligations during tough times.

To secure an extension on your mortgage, contact your lender to discuss your situation. They may offer options such as a mortgage forbearance extension of 18 months if you face temporary hardships. Providing documentation about your financial circumstances can aid your request and improve your chances of obtaining the desired extension.

Typically, mortgage forbearance allows you to pause your payments for a specific period, usually ranging from three to twelve months. However, if you qualify for a mortgage forbearance extension of 18 months, you can benefit from a longer break, helping you regain your financial footing before resuming payments.

Typically, forbearance extensions can last up to 18 months but not several years. However, some situations may differ based on individual lender offerings. Regular communication with your lender is crucial to determine the duration and terms specific to your needs.

New forbearance rules have emerged to provide borrowers with more flexible options during economic difficulties. These rules allow for longer periods of forbearance and clearer paths for repayment. Stay informed on changes in legislation and consult platforms like US Legal Forms for guideline updates and assistance.

Yes, you may qualify for another forbearance if you continue to experience financial challenges. However, this depends on the lender's policies and your repayment history. Be proactive by discussing your options with your lender and exploring a mortgage forbearance extension of 18 months if needed.

The maximum mortgage forbearance time available is typically 18 months, but this can vary based on lender policies and individual circumstances. Factors such as the nature of your financial difficulties may influence how long you can receive assistance. It’s vital to consult with your lender to get accurate information regarding your situation.