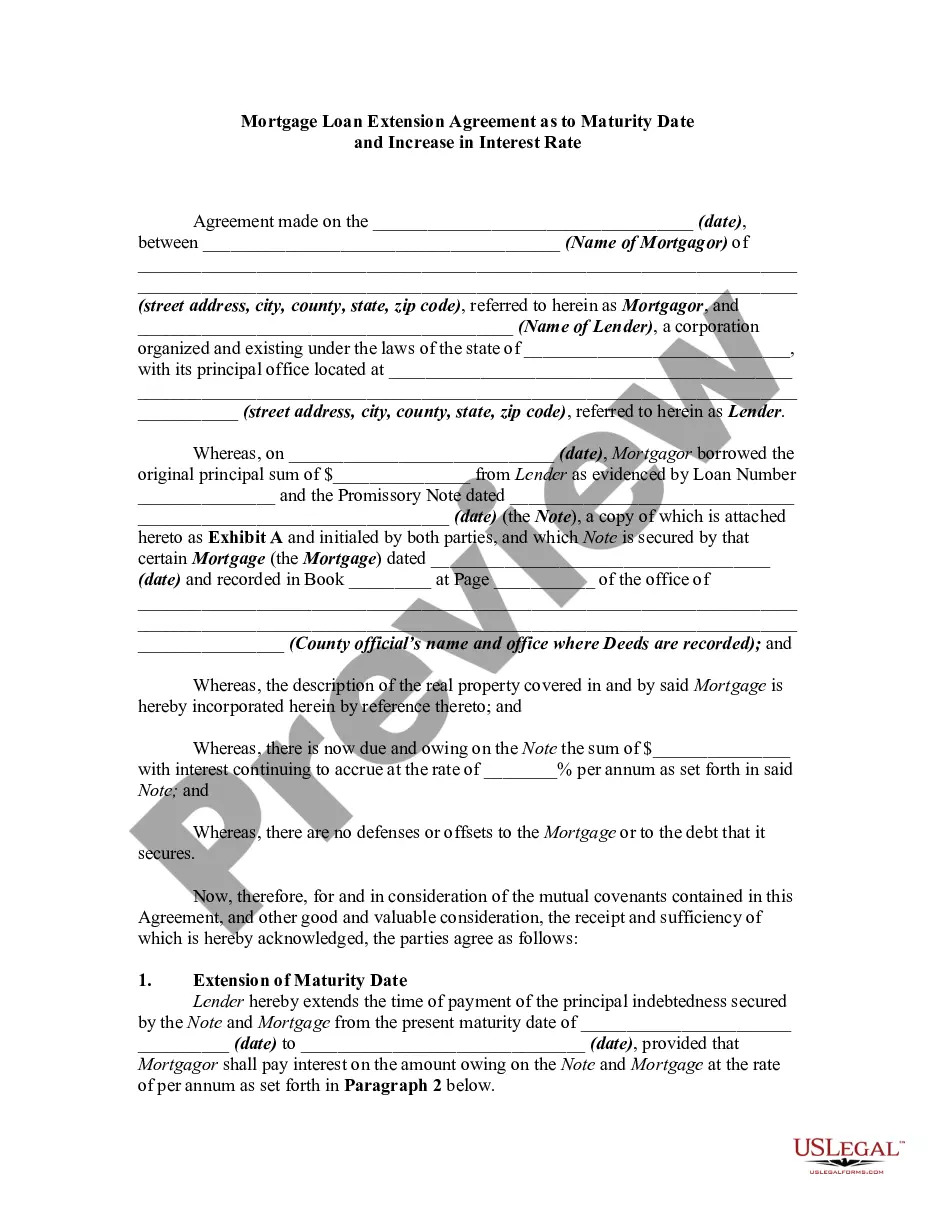

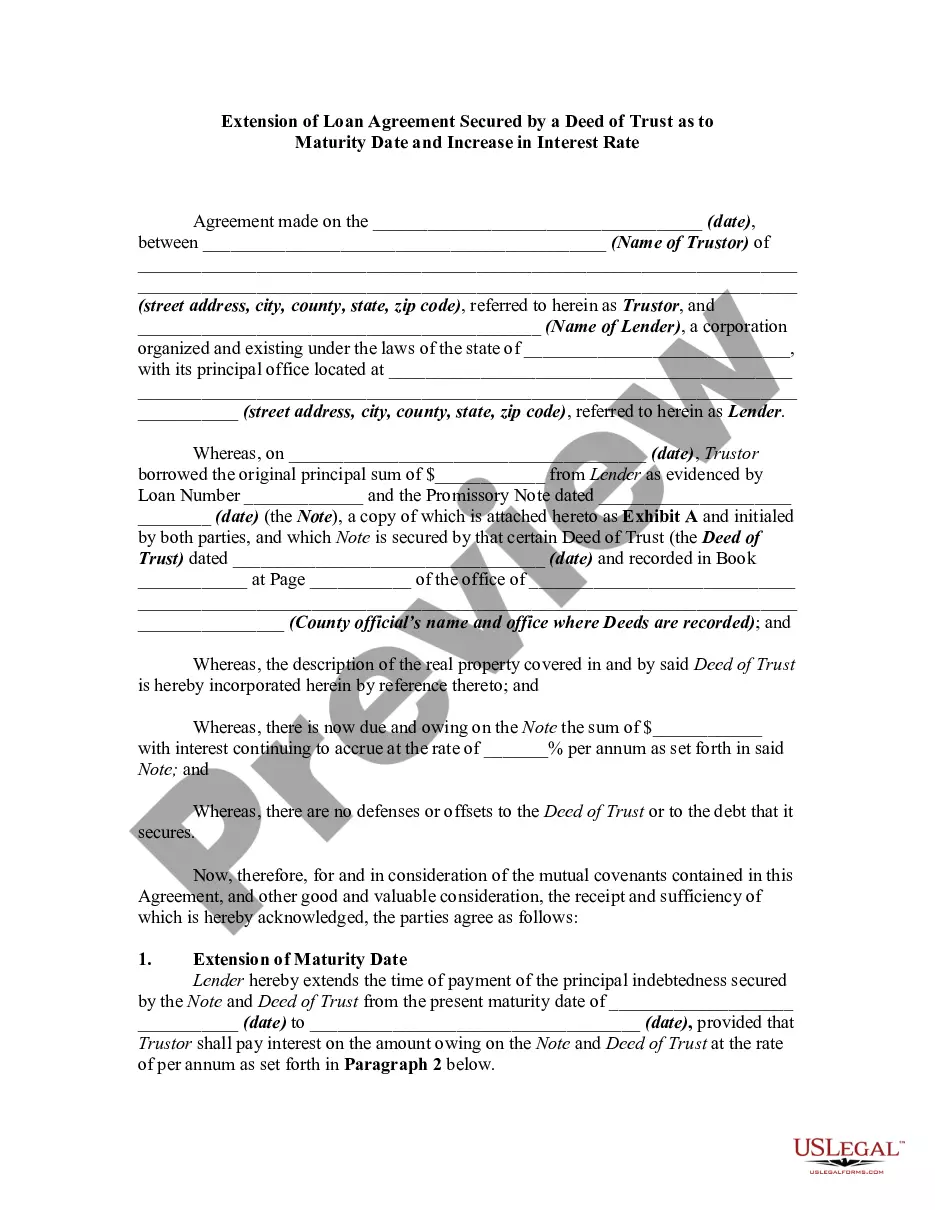

Extension Real Property For Section 179

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Mortgage Extension Agreement With Assumption Of Debt By New Owner Of Real Property Covered By The Mortgage And Increase Of Interest?

Legal documents management can be daunting, even for experienced professionals.

When you are looking for an Extension Real Property For Section 179 and lack the time to dedicate to finding the right and updated version, the process can be stressful.

US Legal Forms accommodates any requirements you may have, from individual to corporate documentation, all in one place.

Leverage sophisticated tools to complete and manage your Extension Real Property For Section 179.

Here are the steps to follow after acquiring the form you need: Verify that it is the correct template by previewing it and reviewing its details, ensure that the sample is accepted in your state or county, click Buy Now when you are ready, select a subscription plan, choose the format you require, and Download, fill out, sign, print, and send your documents. Enjoy the US Legal Forms online repository, supported by 25 years of expertise and trustworthiness. Transform your daily document management into a seamless and user-friendly experience today.

- Tap into a resource library of articles, guidance, handbooks, and tools pertinent to your situation and needs.

- Save time and effort searching for the forms you require, utilizing US Legal Forms’ advanced search and Preview feature to find and obtain Extension Real Property For Section 179.

- If you have a membership, Log In to your US Legal Forms account, search for the form, and download it.

- Check the My documents tab to view the documents you have previously downloaded and manage your folders as desired.

- If this is your first experience with US Legal Forms, create a free account for unlimited access to all the resources of the library.

- A comprehensive online form repository could be transformative for anyone wanting to navigate these challenges effectively.

- US Legal Forms stands as a market leader in online legal documents, featuring over 85,000 state-specific legal templates accessible whenever needed.

- With US Legal Forms, you can access tailored legal and business documents specific to your state or county.

Form popularity

FAQ

Section 179 eligible property includes: Qualified computer equipment and software. Property listed under MACRS (the modified accelerated cost recovery system) with a recovery period of no more than 20 years.

Most types of real property (?section 1250 property?), such as land or land improvements, do not qualify for the section 179 deduction. However, taxpayers may elect to treat ?qualified real property? as qualifying section 179 property. Qualified real property consists primarily of qualified improvement property.

How to report a section 179 expense recapture Under Input Return, select Income. Select Disposition (Sch D, etc.), then Schedule D/4797/etc. Select Carryovers/Misc Info. Select the 4797 Carryovers & Recap tab. Under the Form 4797 section, scroll to the Recapture 50% or Less Business Use subsection.

If placed in service after 2017, qualified improvement property, in addition to no longer qualifying for bonus depreciation and being newly eligible as section 179 property, has a 15-year depreciation period (rather than the usual 39 year period for non-residential buildings).

The 1120-S Schedule K-1, Box 17, Code K instructions for Dispositions of property with section 179 deductions state the corporation reports the shareholder's pro rata share of gain or loss on the sale, exchange, or other disposition of property for which a section 179 expense deduction was passed through to ...