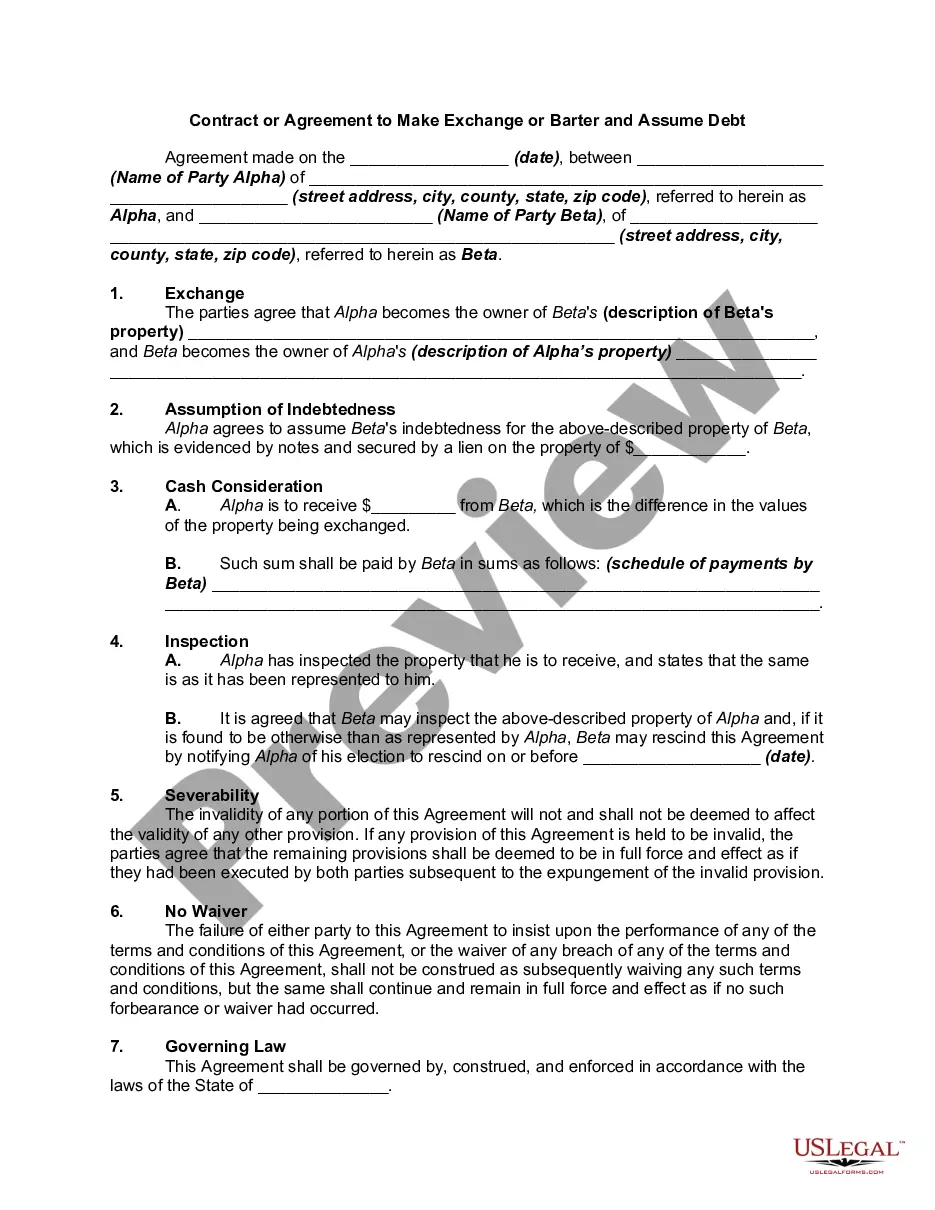

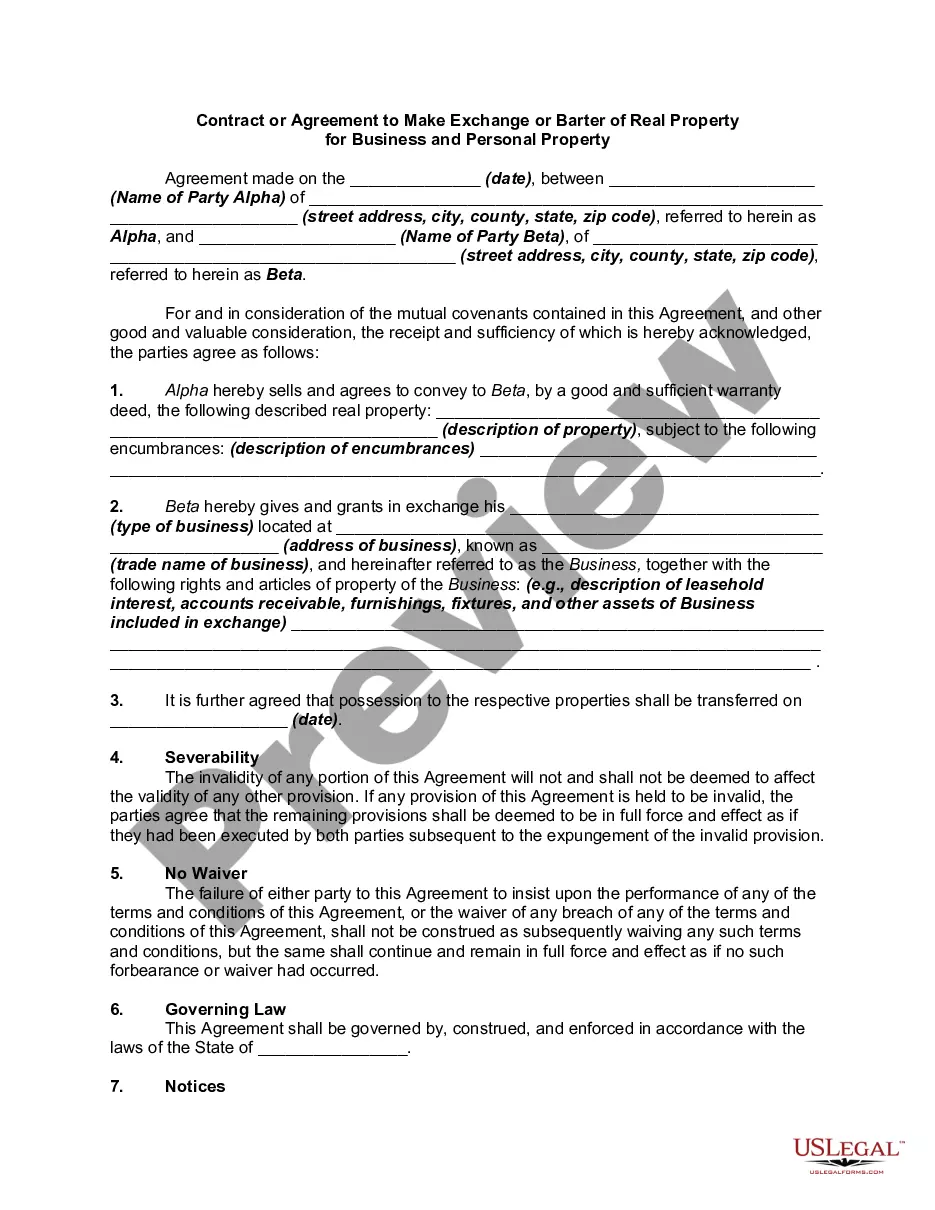

Personal Property Exchange Agreement For 1031

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Contract Or Agreement To Make Exchange Or Barter Of Real Property For Personal Property?

The Personal Property Exchange Agreement For 1031 you see on this page is a multi-usable legal template drafted by professional lawyers in compliance with federal and state laws and regulations. For more than 25 years, US Legal Forms has provided individuals, organizations, and legal professionals with more than 85,000 verified, state-specific forms for any business and personal scenario. It’s the quickest, most straightforward and most reliable way to obtain the paperwork you need, as the service guarantees bank-level data security and anti-malware protection.

Getting this Personal Property Exchange Agreement For 1031 will take you just a few simple steps:

- Look for the document you need and review it. Look through the sample you searched and preview it or review the form description to confirm it fits your needs. If it does not, utilize the search bar to get the correct one. Click Buy Now once you have located the template you need.

- Subscribe and log in. Opt for the pricing plan that suits you and create an account. Use PayPal or a credit card to make a quick payment. If you already have an account, log in and check your subscription to continue.

- Obtain the fillable template. Pick the format you want for your Personal Property Exchange Agreement For 1031 (PDF, DOCX, RTF) and download the sample on your device.

- Fill out and sign the paperwork. Print out the template to complete it by hand. Alternatively, use an online multi-functional PDF editor to rapidly and accurately fill out and sign your form with a legally-binding] {electronic signature.

- Download your papers again. Use the same document again whenever needed. Open the My Forms tab in your profile to redownload any earlier purchased forms.

Sign up for US Legal Forms to have verified legal templates for all of life’s situations at your disposal.

Form popularity

FAQ

Appropriately entitled ?Like-Kind Exchanges,? the IRS Form 8824 is filed by the annual income tax deadline. The form requires a description of the relinquished and replacement property, acquisition and transfer dates, and other information. Replacement Property Identification Form.

Typically, a 1031 exchange involves exchanging relinquished properties with like-kind replacement properties. However, as an investor considering using 1031 funds to build on property you already own, you must equip yourself with the proper knowledge or work with a knowledgeable QI who can guide you through the steps.

Steps to a 1031 Exchange Step 1: Contract and Exchange Documents. ... Step 2: Settlement of Relinquished Property. ... Step 3: 45-Day ID Period. ... Step 5: Settlement on Replacement Property. ... Step 6: Reporting the exchange to the IRS. ... 1031 HELPFUL LINKS.

What is a 1031 Exchange? Step 1: Find a Qualified Intermediary. ... Step 2: Identify The Property to Sell. ... Step 3: Identify Property To Purchase. ... Step 4: Purchase The Replacement Property. ... Step 5: Inform the IRS About The Transaction.

Depreciation After a 1031 Exchange Two schedule depreciation, which is the adjusted cost basis for the property sold divided by 24.5 years (first schedule) and the remaining cost basis of the replacement property divided by 27.5 years (second schedule).