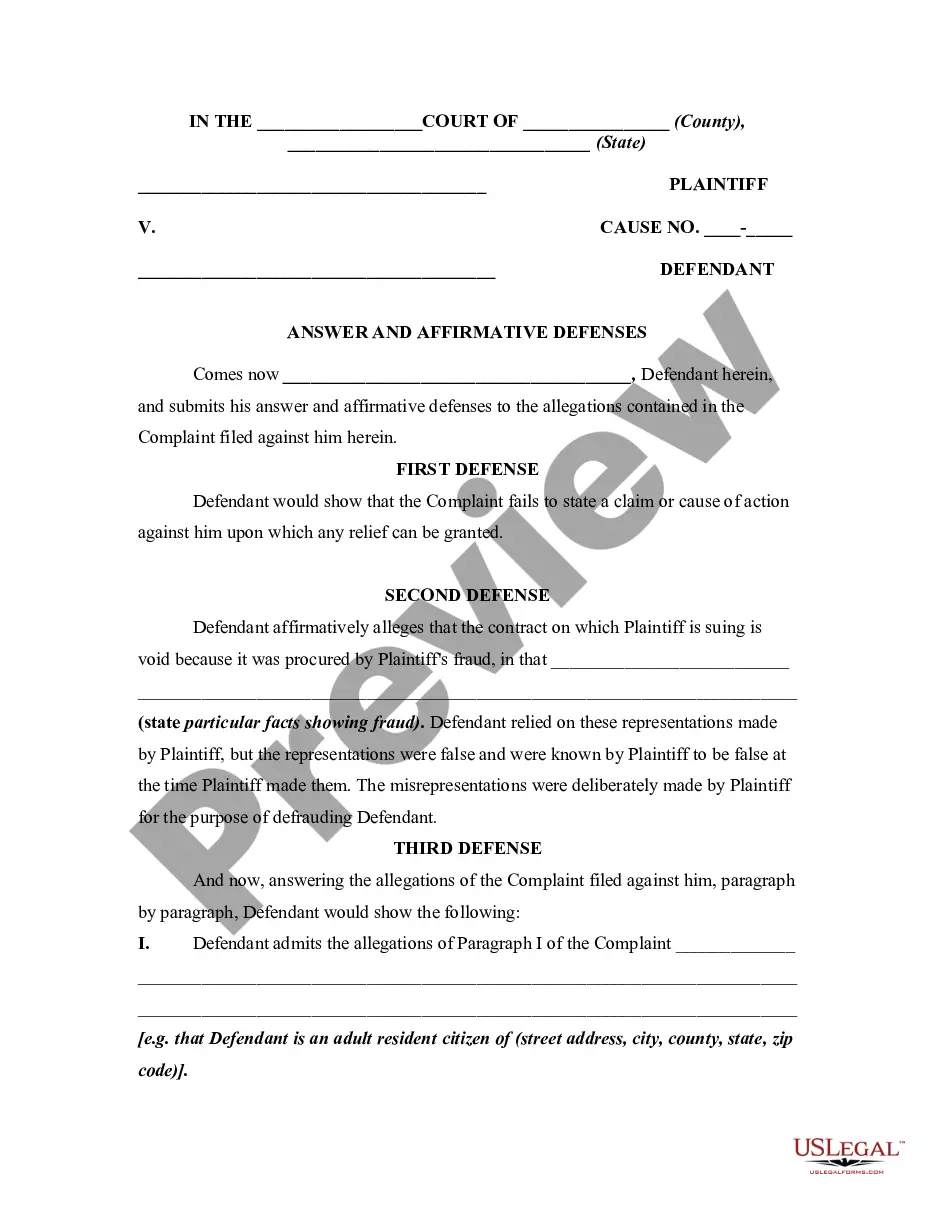

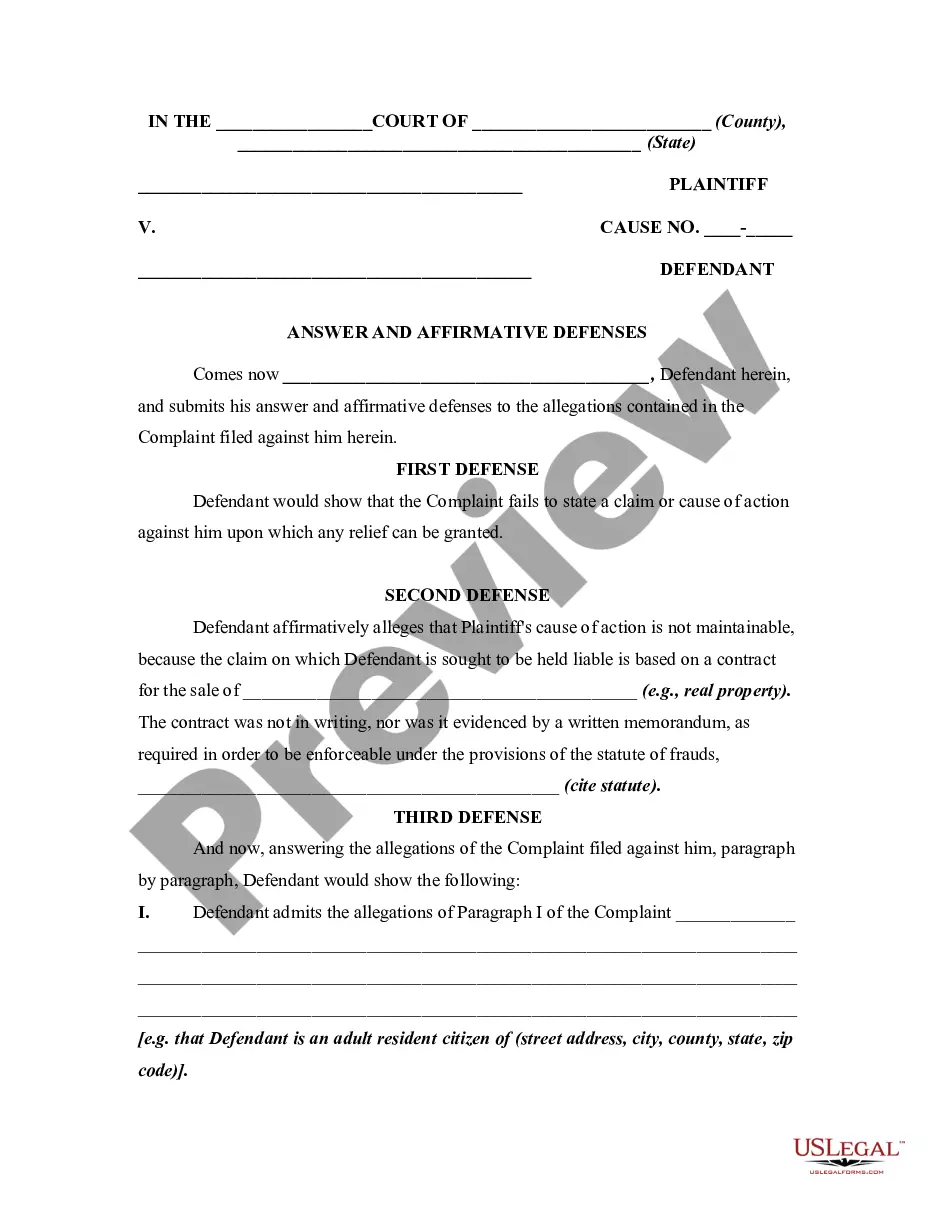

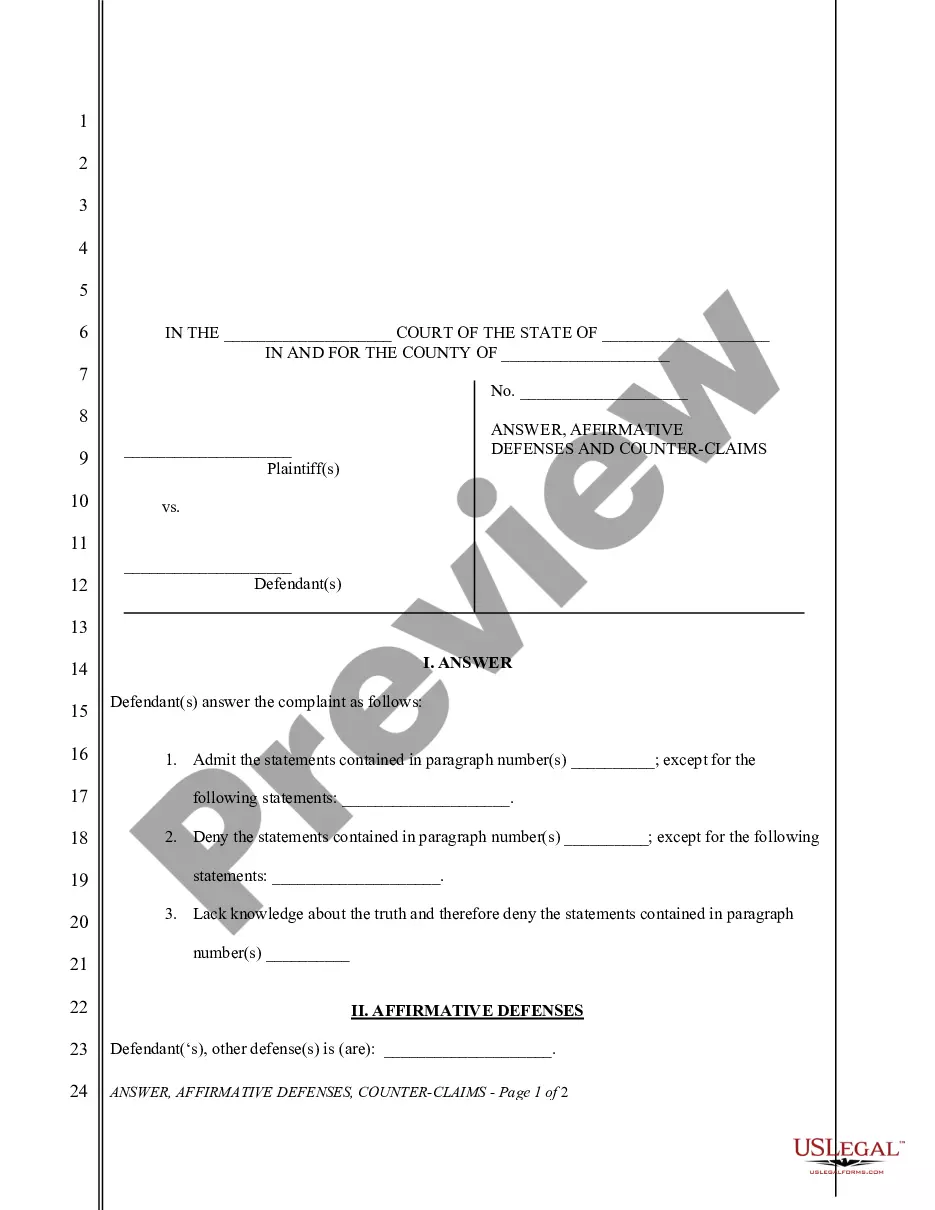

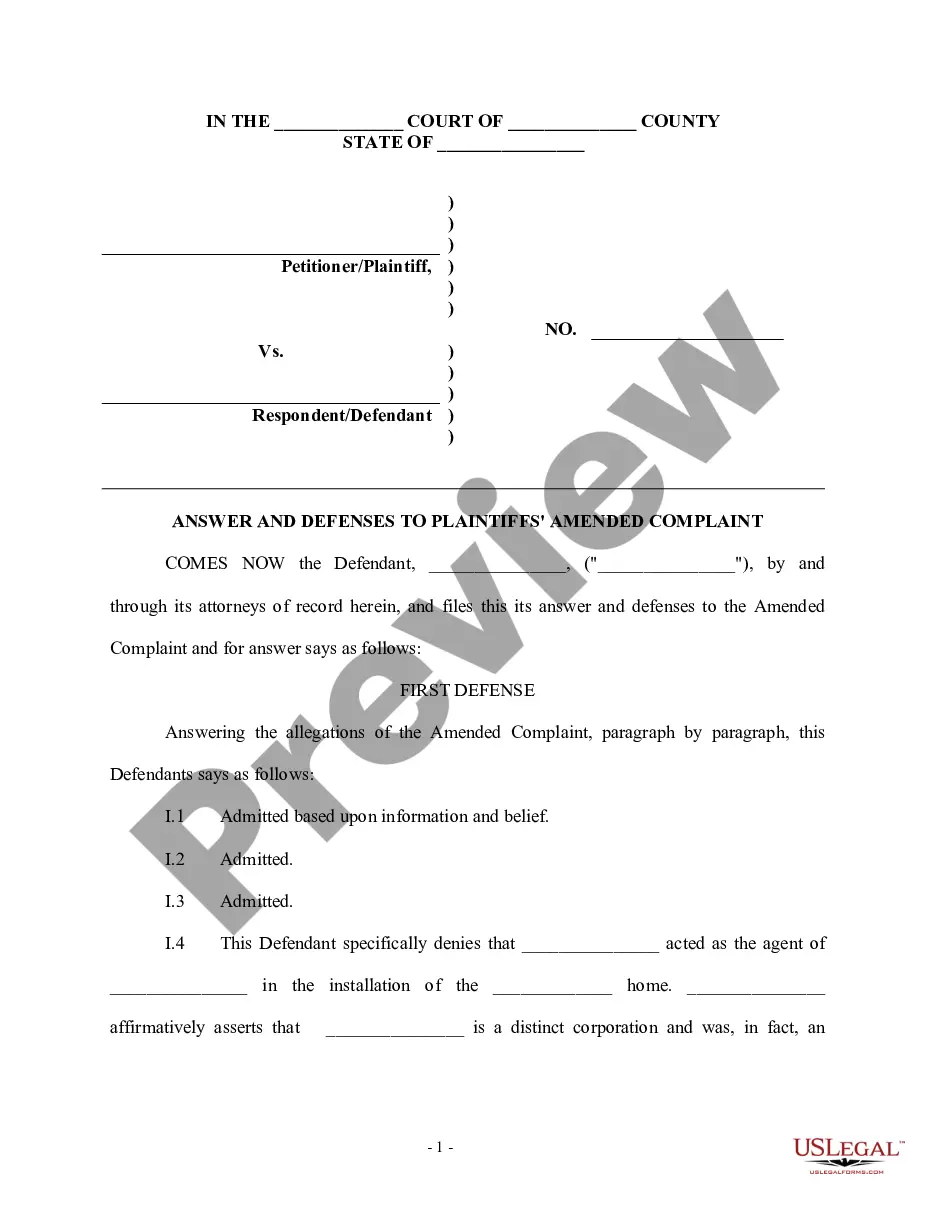

Answer To Debt Collection Lawsuit Example With Explanation

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out General Form Of An Answer By Defendant In A Civil Lawsuit?

The Response To Debt Recovery Lawsuit Sample With Elucidation you observe on this page is a reusable formal template crafted by expert attorneys in compliance with federal and local statutes.

For over 25 years, US Legal Forms has supplied individuals, businesses, and legal professionals with more than 85,000 confirmed, state-specific documents for any commercial and personal event. It’s the fastest, easiest, and most trustworthy method to acquire the paperwork you require, as the service ensures bank-level data protection and anti-malware security.

Subscribe to US Legal Forms to have authenticated legal templates for all of life's situations readily available.

- Search for the document you require and examine it. Browse through the template you looked for and preview it or check the form description to confirm it meets your needs. If it doesn’t, utilize the search bar to find the suitable one. Click Purchase Now once you have located the template you need.

- Sign up and Log In. Choose the pricing option that fits you and set up an account. Use PayPal or a credit card to make a quick payment. If you already possess an account, Log In and verify your subscription to continue.

- Obtain the editable template. Choose the format you desire for your Response To Debt Recovery Lawsuit Sample With Elucidation (PDF, Word, RTF) and store the template on your device.

- Fill out and sign the document. Print the template to complete it by hand. Alternatively, use an online versatile PDF editor to swiftly and accurately fill out and sign your form with a legally-binding electronic signature.

- Re-download your documents. Use the same document again whenever needed. Access the My documents section in your profile to re-download any previously acquired forms.

Form popularity

FAQ

You should dispute a debt if you believe you don't owe it or the information and amount is incorrect. While you can submit your dispute at any time, sending it in writing within 30 days of receiving a validation notice, which can be your initial communication with the debt collector.

If you doubt that you owe a debt, or that the amount owed is not accurate, your best recourse is to send a debt dispute letter to the collection agency asking that the debt be validated. ?An effective debt-dispute letter must be clear and concise,? says Daniel Chan, Chief Technology Officer for Marketplace Fairness.

Dear debt collector, I am responding to your contact about collecting a debt. You contacted me by [phone/mail], on [date] and identified the debt as [any information they gave you about the debt]. I do not have any responsibility for the debt you're trying to collect.

Your answer can be a handwritten letter to the court that says you do not agree with the lawsuit. Include your case (cause) number and mailing address and any defenses you may have to the lawsuit; for example, the amount they claim you owe is incorrect, the account isn't yours, or the debt is older than 4 years.

If a debt collector contacts you, it's your responsibility to: Be honest about your financial situation, including other debts. Reply in good time to calls or letters. Agree to a payment plan if you can afford it. Tell the debt collector if your contact details change.