Self Employed Injury For Insurance

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

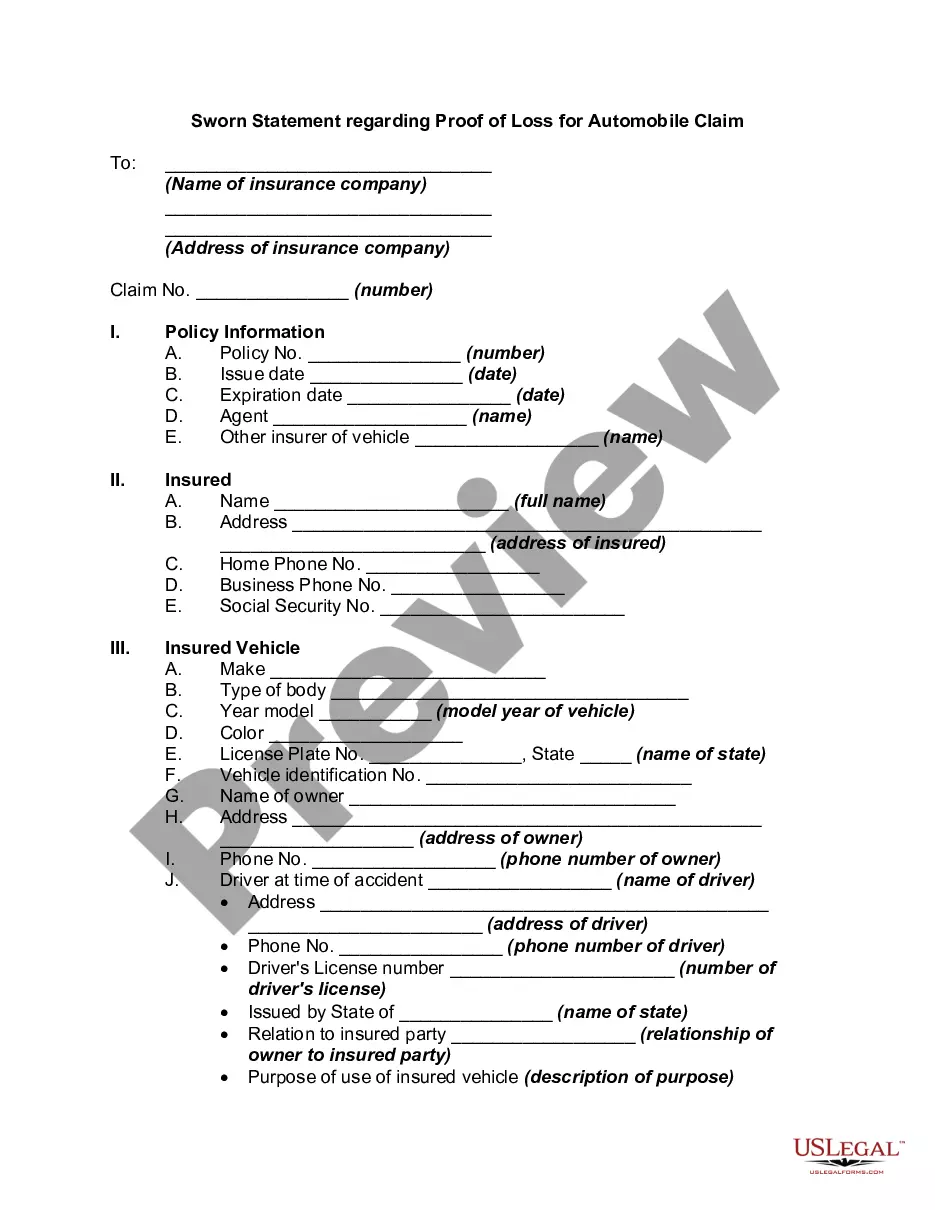

How to fill out Affidavit Of Self-Employed Independent Contractor Regarding Loss Of Wages As Proof Of Damages In Personal Injury Suit?

Regardless of whether for commercial intentions or personal affairs, everyone must confront legal matters at some stage in their life. Filling out legal paperwork demands meticulous care, starting with choosing the correct form template. For example, if you choose an incorrect version of the Self Employed Injury For Insurance, it will be denied upon submission. Thus, it is crucial to obtain a trustworthy source of legal documents such as US Legal Forms.

If you need to obtain a Self Employed Injury For Insurance template, follow these simple steps: Get the form you require by using the search box or catalog browsing. Review the form's description to ensure it aligns with your circumstances, state, and locality. Click on the form's preview to view it. If it is not the right document, return to the search feature to find the Self Employed Injury For Insurance template you need. Acquire the template if it satisfies your requirements.

- If you already possess a US Legal Forms account, simply click Log in to access previously saved documents in My documents.

- If you do not have an account yet, you can download the document by clicking Buy now.

- Choose the suitable pricing option.

- Complete the account registration form.

- Select your payment method: you can utilize a credit card or PayPal account.

- Choose the file format you prefer and download the Self Employed Injury For Insurance.

- Once it is saved, you can fill out the form using editing software or print it and fill it out manually.

- With an extensive US Legal Forms catalog available, you never have to waste time searching for the correct template online.

- Utilize the library's user-friendly navigation to find the suitable template for any situation.

Form popularity

FAQ

If you are self-employed or a business owner, you can buy Elective Coverage through SDI. Some of the rules are different. For example, Elective Coverage is only for 39 weeks, and premiums are based on a percentage of your profit from the previous year.

Many self-employed people consider income protection insurance and critical illness cover in case they get too sick or injured to work, or get a serious illness. People who have dependents, such as a partner or children, often choose to get life insurance.

Individual disability insurance can be particularly helpful if you are a small business owner because the monthly disability benefits you receive can be used any way you want. Since there are no restrictions, you can use your benefits to pay personal expenses or to help sustain your business.

This can hold true not just for regular staff but also subcontractors and even volunteers. If you don't need employers' liability insurance, then you might still want to consider public liability, professional indemnity and business building insurance as a self employed individual.

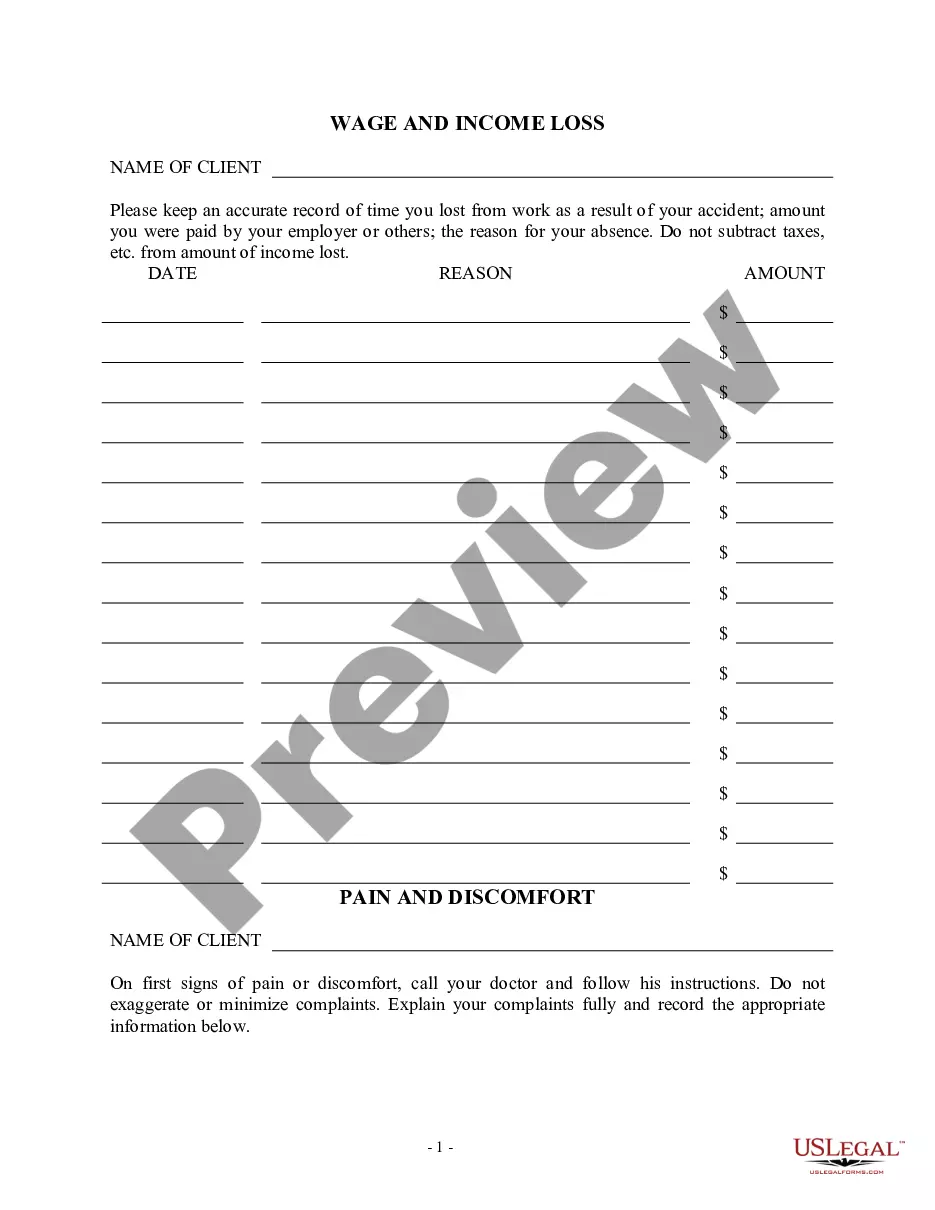

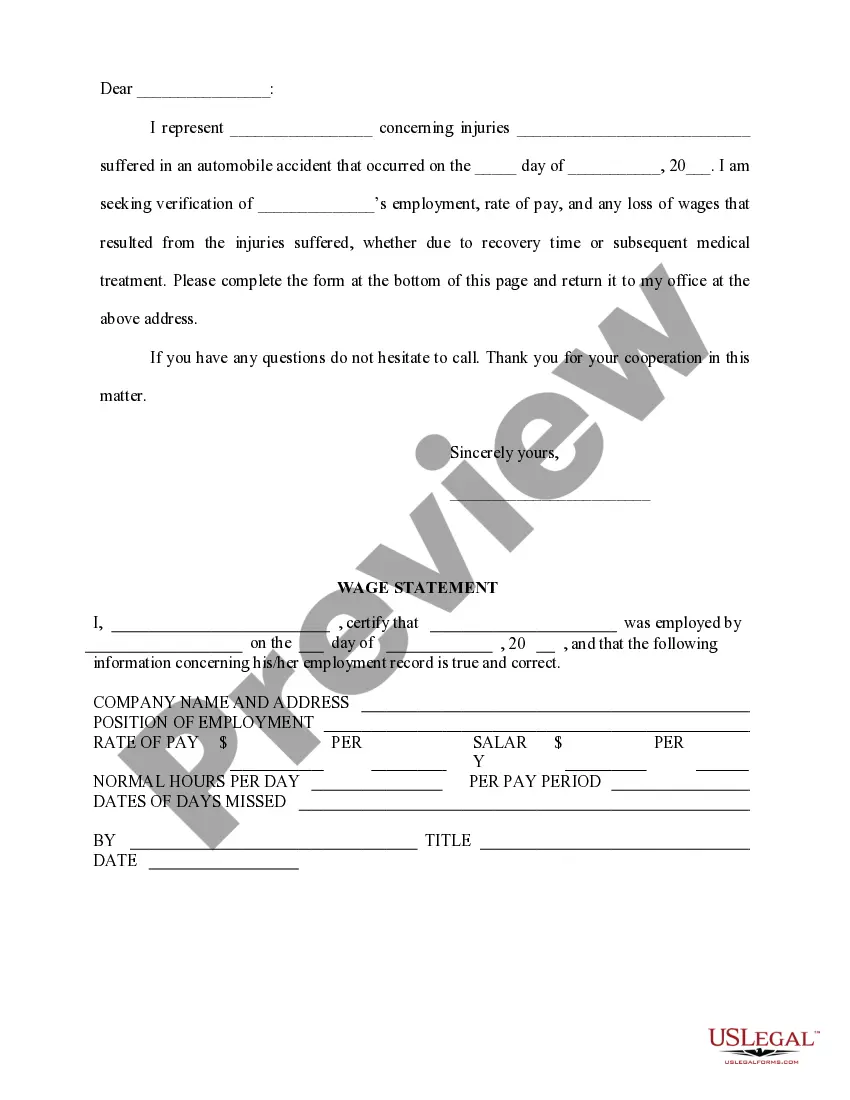

Other ways to prove loss of income in a personal injury claim is with your past W-2 statement or with a Loss of Wages letter from your employer. This letter should include your job title, pay rate, the accident date, time missed and how many hours you work each week.